Download the chart as a .gif file | Download the chart without animation as a .png file

In short

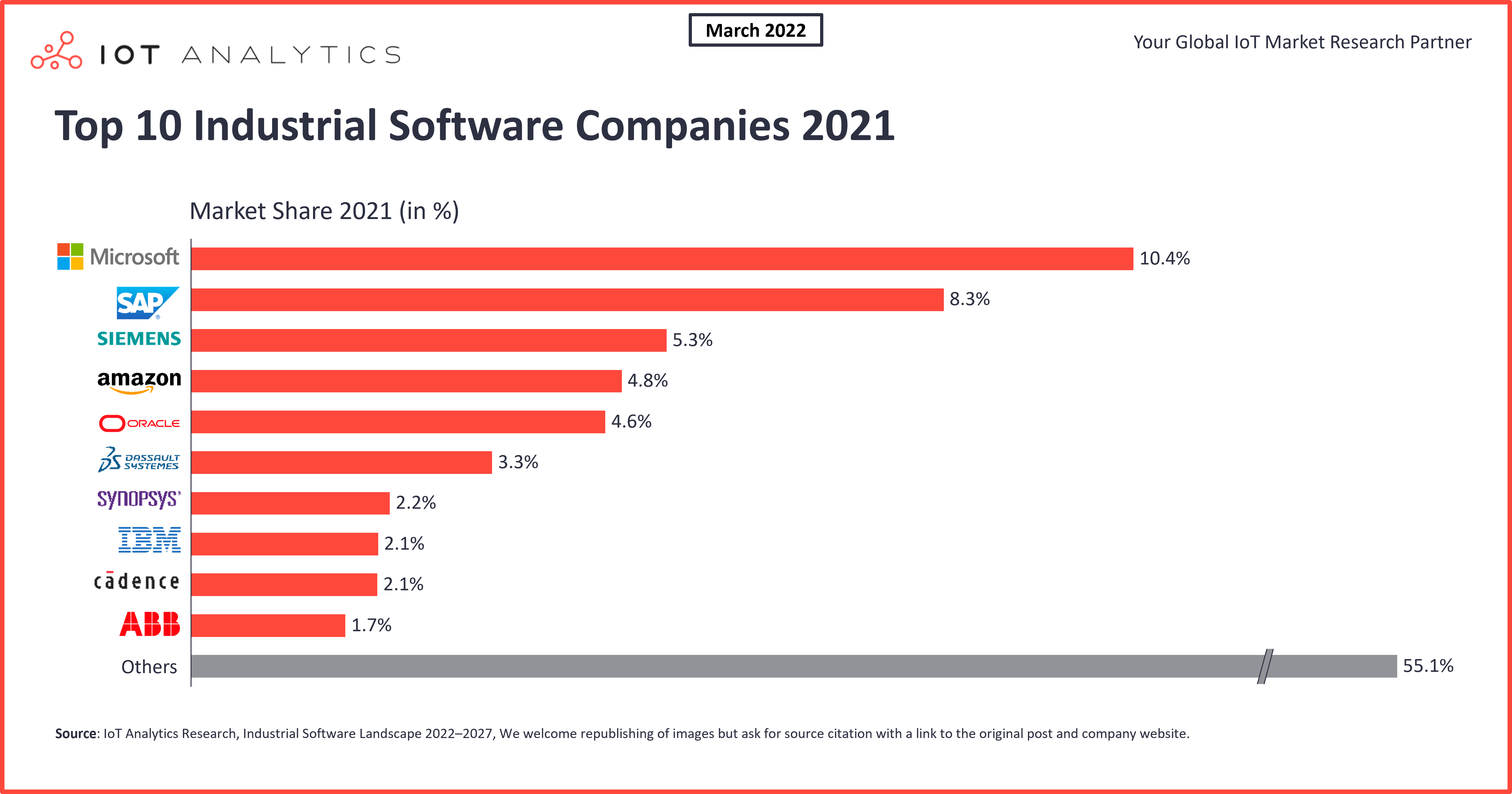

- Microsoft surpassed SAP in 2021 to become the largest industrial software vendor according to IoT Analytics latest research on the topic.

- The overall market for industrial software is estimated to grow at a CAGR of +18% in the next five years across the 14 major software categories analyzed.

Why it matters

- Software will play a significantly bigger role for manufacturers in the future. Understanding and reflecting on the positioning of industrial software companies is a useful exercise for any manufacturer or vendor in the space.

Introduction

2022 is going to be a turning point for manufacturers. For the first time, the average manufacturer will spend more on industrial software than on industrial automation hardware (OT hardware), according to IoT Analytics’ latest report on the industry titled Industrial Software Landscape 2022–2027. Just five years ago, in 2017, the industrial software market was approximately 40% smaller than the hardware-centric OT market, but things are changing quickly. 10 years after Marc Andreessen, in 2011, proclaimed that “software is eating the world,” manufacturing is becoming software-based. It is estimated that five years from now, the industrial software market will be twice as big as the OT hardware market. (The total market size for 2021 is $109 billion; the estimate for 2027 is $288 billion).

Factors driving the industrial software market

There are a number of drivers for industrial software adoption, including:

- The digitization of information flows and data—there are still a lot of previously unconnected assets coming online, worker instructions being digitized, or processes (such as KPI measurement) being automated.

- Softwarization/Virtualization of hardware—hardware budgets are becoming software budgets (e.g., companies spend on public cloud software instead of owning on-premises servers).

- Integration of systems and processes—whether as the layers of the traditional ISA-95 pyramid or any software, more APIs, interfaces, and connectors are being built, tying in suppliers or customers.

- Software delivered with more capabilities and efficiency—many software applications are becoming more efficient and capable. Just think of the limits of CAD tools 20 years ago and the capabilities for real-time 3D simulation and other tools today. Some software is starting to be able to replace humans in specific tasks (or at least provide significant support).

- Systems and data requiring more efficient protection—as system complexity grows, cyber threats are driving the need for more protection (and detection) capability.

- Manufacturers reacting to short-term changes and new requirements—market needs are changing, and it is becoming more and more critical to have transparency, be flexible, and react quickly. Software can often do that (e.g., supply chain transparency and optimization software in case of supply disruptions). Software also enables manufacturers to monitor new KPIs, e.g., tracking CO2 emissions.

The top 10 industrial software companies

These are the top 10 industrial software companies (by market share 2021):

1. Microsoft

In 2021, Microsoft surpassed SAP to become the #1 industrial software company worldwide (in terms of total revenue). Over the last years, Microsoft has gained significant market share in the industrial space thanks to a dedicated focus on and value proposition for manufacturers, most notably through its Microsoft Dynamics and Azure products. Microsoft is a market leader (top five) in the following six of the 14 industrial software categories analyzed:

- Cloud infrastructure and services

- Cybersecurity

- Data and analytics

- Field service

- IIoT platforms

- Virtualization

With cyclical tailwinds in each of these categories, Microsoft is on track to continue to gain market share in the coming years.

2. SAP

SAP has been the undisputed market leader for ERP systems for years, and most manufacturers today rely on ERP components (such as EAM) from SAP for some of their operations. SAP is capitalizing on this leadership position by integrating SAP’s ERP, SCM, HR, and CRM capabilities into a single intelligent enterprise offer aimed at cross-selling SAP’s software between the functional teams of its customers and removing portfolio overlaps.

SAP is a market leader (top five) in the following five of the 14 industrial software categories analyzed:

- Supply chain management

- Enterprise asset management

- Product lifecycle management

- Manufacturing operations management

- Field service

3. Siemens

To many people, Siemens is the market leader for industrial automation hardware. The company, however, is transitioning to becoming more of an industrial software company. The acquisition of UGS in 2007 marked the beginning of Siemens’ execution towards the vision of the “digital enterprise”, a strategy and concept focusing on increased software and digital product and services sales. Siemens has stuck to this strategy successfully since. Siemens’ industrial software revenue growth, however, has recently slowed, as the company is transitioning its offers towards software as a service (SaaS), which typically results in lower revenue in the short term with the prospect of higher revenue in the long run.

Siemens is a market leader (top five) in the following six of the 14 industrial software categories analyzed:

- Electronic design automation

- Computer-aided design

- Machine control

- Product lifecycle management

- Manufacturing operations management

- IIoT platforms

4. Amazon (AWS)

AWS, just like Microsoft, is gaining market share in the industrial software market due to its leading position in the public cloud market and the attached revenue through various services and its AWS B2B Marketplace. Amazon also targets industrial manufacturers with its newly launched AWS for industrial software portfolio.

5. Oracle

Oracle, alongside its main competitor SAP, is a market leader in the ERP and SCM market through its Oracle NetSuite and Oracle Fusion offers. The company also offers cloud infrastructure and related services, although it is not a top-five vendor in this space. Oracle’s success has been associated with its early shift to an SaaS business model. Back in 2014, the company considered itself the world’s second-largest cloud SaaS company. This shift has allowed Oracle customers to source Oracle software more flexibly than with traditional perpetual licenses. Today, customers still appreciate the ability to customize Oracle’s software and features according their needs.

6. Dassault Systèmes

France-based Dassault Systèmes is the market leader for CAD and PLM software through a suite of offerings, most notably Dassault Catia and Dassault SolidWorks. In recent years, the industrial software company has announced a number of key partnerships with other leading industrial software companies to provide an end-to-end solution for key industry verticals. In 2019, Dassault announced a partnership with ABB providing an end-to-end CAD, SCM, and MOM solution dedicated to robotics. In February 2022, the company also announced a partnership with Cadence Design Systems. This partnership will enable both companies to provide a cross-functional understanding of the manufacturing processes of chipmakers, with interconnected software capabilities on supply chain and manufacturing operations management software and electronic design automation (EDA) and CAD software.

7. Synopsys

US-based Synopsys is the global market leader in the EDA space, a category that is riding the momentum (and thus high growth) in the global chip industry. The company has a dedicated focus on chipset design and semiconductor intellectual property licensing in AI, automotive, cloud, and IoT. Synopsys also has a dedicated offer for application security testing and is set to continue benefitting from high growth in the cybersecurity space due to its DevSecOps offerings.

8. IBM/Kyndryl

IBM, once the world’s second-most valuable brand, recently split its business into two companies. The new company, Kyndryl, focuses on IBM’s infrastructure business, while the remaining part of IBM will focus on cloud services and AI. Although IBM has been struggling to grow its business meaningfully in recent years, it continues to deliver a strong industrial software portfolio with offerings such as IBM Maximo enterprise asset management, IBM hybrid cloud, IBM WebSphere, or IBM security.

9. Cadence Design Systems

Just like Synopsys, Cadence is a leader in the EDA software market. Cadence began as a pure-play EDA software vendor but has expanded into other products, such as IC package design and analysis and intellectual property used to design chips.

10. ABB

Switzerland-based ABB has a market leading position in industrial process automation, robotics, drives & motors, and electrification infrastructure. Among ABB’s key software value propositions are its robotics simulation and programming software as well as its MOM, SCADA, and PLC programming software. In recent years ABB has released software in the IIoT and Industrial AI / Analytics space building on ABB Ability, the latest being the ABB Ability Genix Industrial Analytics and AI Suite, a modular Industrial AI and IoT platform.

In contrast to most of ABB’s competitors, the company, in 2019, decided to embark on a decentralized organizational strategy with each of the 4 ABB business areas managing their own software portfolio with some solutions cutting across the organization.

Conclusion and outlook

Software plays an increasing role for manufacturers globally. The market for the top industrial software companies is relatively fragmented, with some high-growth categories, such as cloud infrastructure and services, cybersecurity, and data analytics.

As more companies digitize and modernize their software setup, those with heavy exposure in these above-mentioned segments will continue to gain a larger portion of the overall industrial software spend.

The growth rates of the top 10 industrial software companies vary tremendously. The top 10 industrial software companies in five years will almost certainly not be the same as the top 10 today. Market positioning plays a massive role in determining tomorrow’s winners. But there are also other factors that determine future success for these vendors including:

- The ability to differentiate in the new edge-to-cloud setup

- The ability to transition to SaaS successfully

- The ability to differentiate with new capabilities, such as AI or low-code

To maximize opportunity, any vendor in this market should check their strategy against these and other trends mentioned in the market report.

DISCLAIMER: This data set was developed based on publicly available investor relations revenue data as well as a number of proxys and survey data. Vendors did not influence the calculation. Please note that IoT Analytics has commercial relationships with some of the companies analyzed as part of this research.

| The Industrial software market

| Definition

IoT Analytics defines the industrial software market as follows: Industrial software is a tool used for creating or managing information related to the industrial manufacturing value stream. This definition includes key software categories that support the manufacturing value stream from product design to product maintenance. Excluded are supporting software tools, such as sales and marketing, HR, finance, and legal software.

The report includes software used for core value chain activities for industrial manufacturing end users as defined per discrete, process, and hybrid manufacturing and logistic service providers. Examples of these industries are ISIC C 27—manufacture of electrical equipment, ISIC C 20—manufacture of chemicals, ISIC C 24—manufacture of basic metals, and ISIC H 52—warehousing and supporting activities for transportation.

| 14 major software categories make up the market

- Computer-aided design (CAD)

- Electronic design automation (EDA)

- Product lifecycle management (PLM)

- Machine control

- Manufacturing operations management (MOM)

- IIoT platforms

- Supply chain management (SCM)

- Field service

- Enterprise asset management (EAM)

- Cloud infrastructure and services

- Cybersecurity

- Virtualization

- Remote access

- Data and analytics

More information and further reading

Are you interested in learning more about the industrial software landscape?

The Industrial Software Landscape 2022-2027 is a 65-page report and database detailing the industrial software landscape. It is part of IoT Analytics’ ongoing coverage industrial IoT.

The report includes a global industrial software vendor database, with a classification of 150+ companies in 14 different software categories, market size and forecast, competitive landscape, trends, deep dives, and more.

This report provides answers to the following questions:

- How large is the industrial software market, and how fast is it growing?

- How large are individual sub-markets, and how far are they growing?

- Which companies are active in specific software categories, and what is their market share?

- What are some of the key market trends?

- What are specific trends in each of the individual software categories?

- And more

Sample

The sample of the report gives you a holistic overview of the available analysis (outline, key slides). The sample also provides additional context on the topic and describes the methodology of the analysis. You can download the sample here:

Related articles

You may also be interested in the following articles:

- Soft PLCs: Revisiting the industrial innovator’s dilemma

- The rise of industrial AI and AIoT: 4 trends driving technology adoption

- Cloud MES: How manufacturing software is migrating to the cloud

- The IoT cloud: Microsoft Azure vs. AWS vs. Google Cloud

- The case for a $2 trillion addressable public cloud market

Subscribe to our newsletter and follow us on LinkedIn and Twitter to stay up-to-date on the latest trends shaping the IoT markets. For complete enterprise IoT coverage with access to all of IoT Analytics’ paid content & reports including dedicated analyst time check out Enterprise subscription.