In short

- The generative AI market surpassed $25.6 billion in 2024, driven by rapid adoption and the increasing integration of AI capabilities across industries, according to the 263-page Generative AI Market Report 2025–2030 (published January 2025).

- The data center GPU market saw remarkable growth to $125 billion, with NVIDIA maintaining a dominant position, holding 92% of the market share.

- Microsoft and AWS lead the rapidly expanding foundation models and model management platforms market, while Accenture and Deloitte lead the highly fragmented generative AI services market.

Why it matters?

- For generative AI companies: The new generative AI market landscape is rapidly evolving and presenting many opportunities across the hardware, software/platform, and services industries.

- For generative AI end users: Understanding who is ahead, who is upcoming, and the strengths and weaknesses of individual players and their models is important when building generative AI solutions and making important vendor and architecture decisions.

The rise of generative AI: Rapid market growth and widespread adoption

Generative AI market surpassed $25 billion in 2024. Over two years, the combined generative AI software and services market (including foundation models and model management platforms) skyrocketed from a mere $191 million market in 2022 to $25.6 billion in 2024,* according to IoT Analytics’ 263-page Generative AI Market Report 2025–2030 (published January 2025). According to the analysis in the report, the acceleration of generative AI adoption across industries is driving this growth, with businesses increasingly incorporating AI-driven capabilities into their operations. Since the introduction of breakthrough Generative AI models, CEOs have increasingly discussed AI and its workplace applications in their earnings calls, and companies have raced to leverage this technology.

*Note : The combined market size for generative AI foundation models, model management platforms, and services does not include the market for individual generative AI applications (such as ChatGPT).

Key adopter quote

“We’re finding tangible ways to leverage GenAI to improve the customer, member, and associate experience. We’re leveraging data and LLMs from others and building our own.”

Doug McMillon, CEO of Walmart (during Walmart’s Q2 2025 earnings call on August 15, 2024)

The AI hardware market—specifically, data center GPUs—also experienced vast growth, climbing from $17 billion in 2022 to $125 billion in 2024 as major hyperscalers and large IT software companies (most notably, Salesforce and Meta) raced to expand their cloud and AI capabilities using the powerful processors.

About IoT Analytics’ generative AI market coverage

Insights in this article are from IoT Analytics’ 263-page Generative AI Market Report 2025–2030, its 3rd report about generative AI in general and its 2nd major market report on the topic.

While traditionally focused on the intersection of industry and technology, IoT Analytics has covered the AI markets since 2017, starting with industrial AI and predictive maintenance applications. Over the years, it expanded its scope to broader technology and enterprise trends, including (generative) AI, given its far-reaching impact across industries.

Already a subscriber? View your reports here →

As part of its research for the latest generative AI market report, the team spoke with 50+ experts in the field and gathered information on 530+ generative AI projects, analyzing which industries and departments are quick to adopt generative AI and which vendors are most selected today. The research is holistic across industries and use cases, with industrial case deep-dives.

IoT Analytics plans to continue publishing follow-up market reports annually, as the market is growing and maturing, and the competitive landscape is likely to remain very dynamic for the foreseeable future.

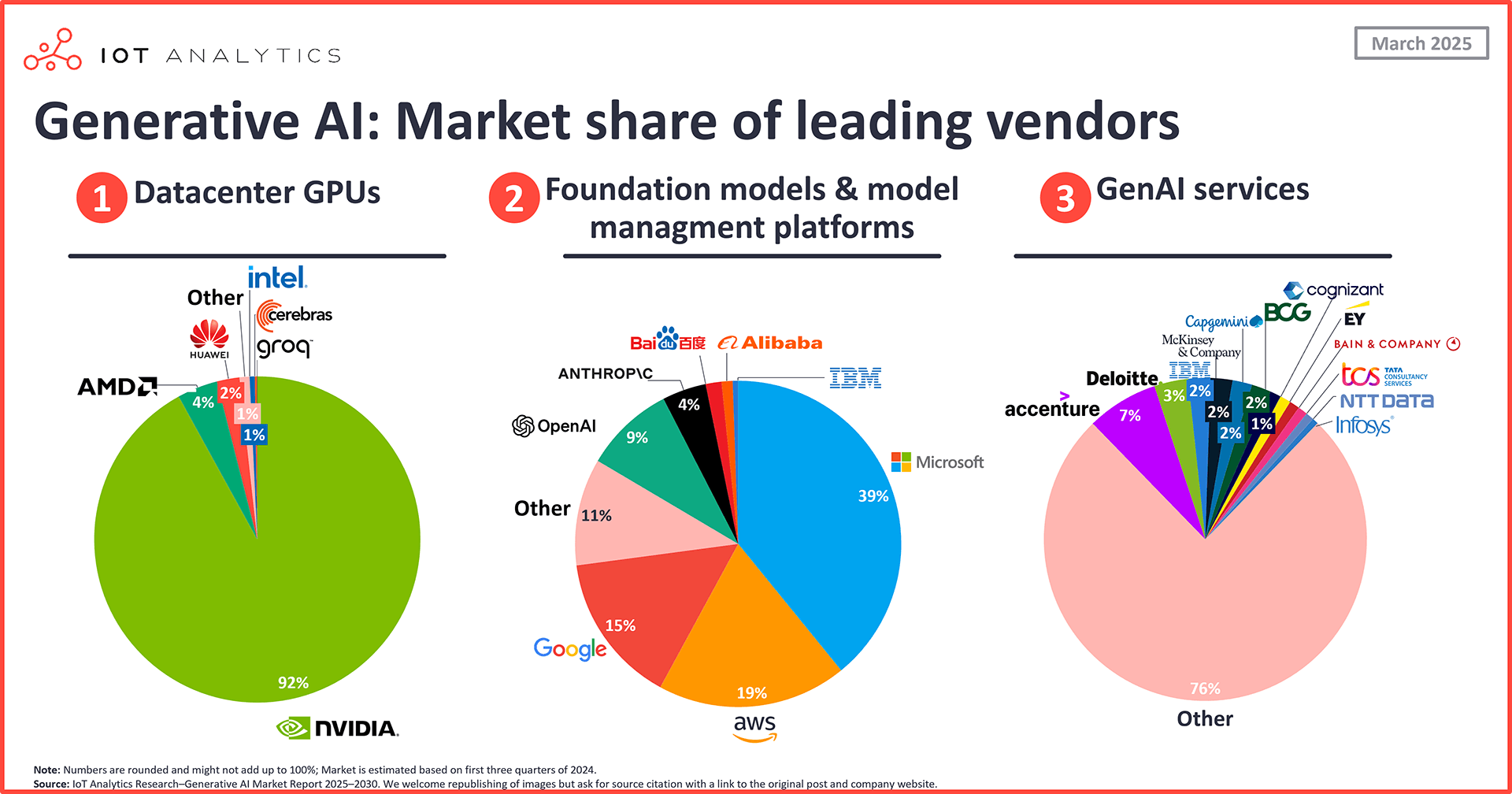

The leading generative AI companies

With all three generative AI market segments—1) data center GPUs, 2) foundation models and model management platforms, and 3) generative AI services—set to experience continued rapid growth through 2030, the IoT Analytics team presents the leading companies for each market below. Both the data center GPU market and foundation models and model management platforms market show clear dominant market leaders, while the generative AI services market shows a bit more fragmentation.

Market 1: Data center GPUs

a) Market overview

Data center GPU market surges amid strong demand. According to IoT Analytics research, the data center GPU market more than doubled year-over-year (YoY) in 2024, mostly driven by one company alone: NVIDIA. Data center GPUs refers to specialized GPUs designed to handle the extensive computation demands of modern data centers, which are the backbone of generative AI. Supply constraints, high prices, and stiff competition for top-tier GPUs make this market both dynamic and challenging.

Hyperscalers are the biggest buyers of GPUs

Hyperscalers like AWS, Google, and Microsoft remain the biggest buyers, and other technology companies like Meta are also ramping up GPU investments. Despite smaller, more efficient models, like DeepSeek’s R1, being introduced to and affecting the market across the value chain, there is currently no reason to believe demand will decline in the near future.

Note: The data center GPU market does not include CPUs, consumer GPUs, TPUs , ASICs, or other chips; only GPU systems intended for data center use.

Key quote

“There is a new demand in town, which is the change of data center […] when they change and become more related to AI. That has, of course, increased demand in the U.S. It is also a pretty much a selective or exclusive discussion with the fewer players. […] And of course, we participate as part of the supply chain and the supply of either projects or turbines for doing it.”

Henrik Andersen, CEO of Vestas Wind Systems AS (during Vestas’ Q3 2024 earnings call on November 5, 2024)

b) Leading data center GPU companies

One company dominates. At this point, the data center GPU market has one very clear leader. However, the market report shows that there are promising startups and other established companies trying to make inroads.

1. NVIDIA

Record revenue keeps NVIDIA at top of data center GPU market. In 2024, US-based semiconductor company NVIDIA vastly led the data center GPU market, holding 92% of the market share (similar market share as in 2023). Throughout 2024, the company’s quarterly revenue for its data center GPUs kept climbing, resulting in a record annual revenue of just over $115 billion in 2024, up 142% YoY.

NVIDIA’s key strengths: Advanced GPUs and the CUDA ecosystem. NVIDIA’s AI strategy focuses on becoming the all-in-one supplier of the AI data centers of the future. The company’s continuous GPU architectures and software innovations have helped it maintain its leadership. Its AI-focused accelerators—like the NVIDIA H100 Tensor Core GPU or the most recent Blackwell-architecture GPUs—remain the standard for data center GPUs. Additionally, as discussed in the report, NVIDIA’s CUDA parallel computing platform and programming model remains a critical differentiator. The company has spent most of the last two decades working to improve CUDA, turning it into a leading software architecture and developer ecosystem. This is often considered NVIDIA’s biggest moat, making it one of the key reasons NVIDIA is not set to lose its dominant position anytime soon.

NVIDIA aims at positioning itself as the go-to source for what it calls the “AI factory” of tomorrow, a new type of AI-focused data center, by investing in cutting-edge AI hardware for the entire data center, including networking solutions such as Infiniband, Ethernet switches, AI-optimized routers, CPUs, and continuously more powerful AI accelerators, alongside its powerful software platforms like CUDA.

“I think it’s important to understand that we wouldn’t have a massive AI networking opportunity if NVIDIA didn’t build some fantastic GPUs.”

Jayshree Ullal, CEO of Arista Networks (during Arista Network’s Q1 2024 earnings call on May 07, 2024)

2. AMD

AMD sees small market share increase. US-based semiconductor AMD’s data center GPU segment, NVIDIA’s first real GPU challenger, grew by 179% between CY 2023 and CY 2024, thereby increasing its market share by 1 percentage point (4% in 2024 vs. 3% in 2023). Its AI strategy revolves around providing an open, end-to-end, and cost-effective AI infrastructure. As of December 2024, it is estimated that AMD shipped 307,000 of its flagship MI300X GPUs to Meta, Microsoft, and Oracle.

AMD offers cheaper AI GPUs and ROCm. AMD continues to invest in the hardware and software front for advancing AI. In Q4 2024, the company announced the release of its Instinct MI325 Series accelerators, which are cheaper than NVIDIA’s comparable accelerators, alongside continuous investments in the AMD ROCm 6.2 platform, AMD’s response to NVIDIA CUDA.

Key quote

“We have made outstanding progress building the foundational product, technology, and customer relationships needed to capture a meaningful portion of this market. And we believe this places AMD on a steep long-term growth trajectory, led by the rapid scaling of our data center AI franchise for more than $5 billion of revenue in 2024 to tens of billions of dollars of annual revenue over the coming years.”

Lisa Su, CEO of AMD (during AMD’s Q4 2024 earnings call on February 4, 2025)

3. Emerging AI hardware players

Huawei claims market share with AI chip efforts and proprietary architecture. Emerging AI hardware players are focusing on novel AI acceleration strategies to challenge the dominance of established players. Huawei, a China-based information and communications technology company, has ramped up investment in AI hardware—specifically, in its Ascend AI chips, which are supported by Huawei’s proprietary Da Vinci architecture. Huawei designed the Da Vinci architecture to be universal across Huawei chipsets, energy efficient, and scalable for cloud and enterprise applications. In 2024, Huawei secured 2% market share.

Cerebras and Groq push AI chip innovation. Huawei is not alone in gaining traction. AI-focused semiconductor startups like Cerebras and Groq, both US-based, have emerged as new players. While still relatively small players, these startups are pioneering specialized AI chip architectures. Cerebras offers its wafer-scale processors designed for massive AI model training, and Groq deterministic, ultra-low-latency inference chips optimized for real-time AI workloads.

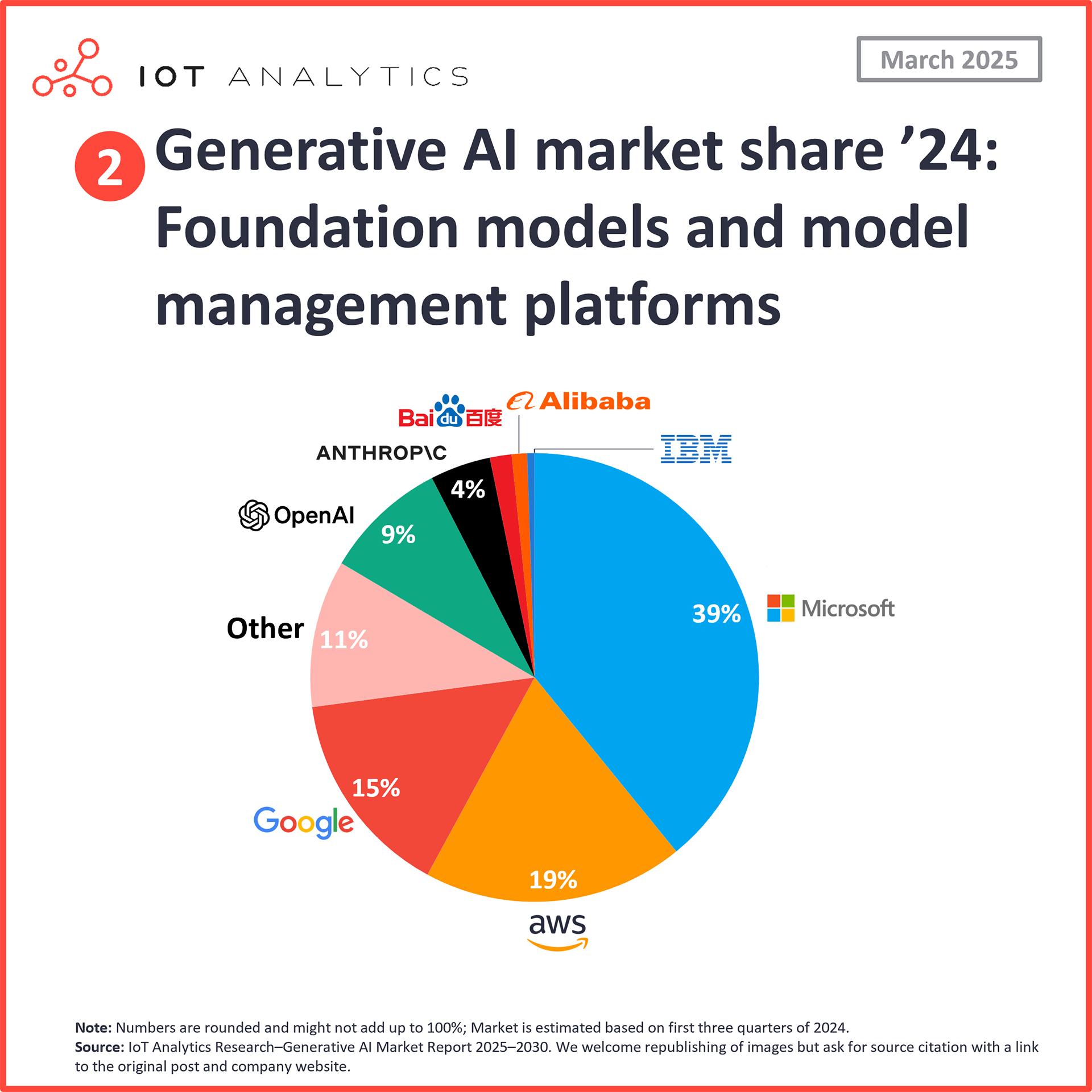

Market 2: Generative AI foundational models and platforms

a) Market overview

Enterprise AI adoption to drive market expansion. In 2024, the foundation models and model management platforms market reached $11 billion.* IoT Analytics projects strong market growth in the coming years as enterprises continue to invest billions in—and report real value from—generative AI implementations and continuous improvements.

*Note: The foundation model and model management platforms market does not include chatbots and applications such as ChatGPT.

The foundation models and platforms market comprises two related areas. Foundation models are large-scale, pre-trained models that can be adapted to various tasks without the need for training from scratch, such as language processing, image recognition, and decision-making algorithms. In turn, model management platforms are software platforms that enable users to deploy, fine-tune, and call generative AI models. These platforms allow the use of different models and are not limited to one single model vendor.

b) Leading generative AI foundational model and platform companies

The foundation model and platform market has become increasingly competitive, with hyperscalers and AI startups alike refining their strategies to capture enterprise demand.

1. Microsoft

Microsoft holds lion’s share for AI platforms. US-based software company and hyperscaler Microsoft has solidified its leadership in the foundation models and platforms sector, with an estimated 39% market share in 2024. Its dominance is driven by its deep integration with leading foundation models (such as OpenAI’s models) and enterprise-focused AI services. Azure AI provides businesses with multimodal AI support and customization, making it the dominant cloud AI platform with the most new generative AI customers of the hyperscalers.

Microsoft advancing enterprise AI and agentic ecosystems. Microsoft is focused on integrating AI across enterprise workflows by combining proprietary and third-party models, leveraging Azure AI infrastructure and services to offer enterprises flexibility in deploying AI solutions. Another key priority is building an agentic world, partnering with companies and organizations to drive an agentic ecosystem where agents work across enterprise boundaries.

Microsoft has announced plans to invest $80 billion in 2025 to build a full-stack AI infrastructure to achieve its vision, on top of an already existing investment of $10 billion that the company has in OpenAI.

2. AWS

AWS takes nearly 1/5 of the market. US-based hyperscaler AWS strengthened its position in the foundation model and model management platform market, securing an estimated 19% market share in 2024. The company has focused its efforts on delivering a scalable infrastructure along with a wide range of hardware and software solutions. It quickly scaled its model management platform services (i.e., Bedrock and Sagemaker) by leveraging its public cloud services leadership, positioning itself as an environment with an ecosystem of third-party and proprietary models. This gives its customers access to a variety of models—both its proprietary NOVA models and models from developers Anthropic, AI21 Labs, Cohere, and others—while also pairing them with AWS’s own GPU-as-a-service offerings (including access to its own AI chips, like Amazon Trainium2).

AWS ramps up AI investment with Anthropic and infrastructure. AWS has increased its AI investments in recent years and is deepening its collaboration with Anthropic. In November 2024, AWS announced a $4 billion investment in Anthropic, while Anthropic named AWS its primary training partner. Further, Anthropic committed to using AWS Trainium and Inferentia chips to train and deploy its future foundation models. More recently, Amazon CEO Andy Jassy shared that Amazon will spend over $100 billion on capital expenses toward AI infrastructure in 2025.

Key quote

“When AWS is expanding its CapEx, particularly on what we think is one of these once-in-a-lifetime type of business opportunities like AI represents, I think it’s actually quite a good sign medium to long term for the AWS business.”

Andy Jassy, CEO of Amazon (during Amazon’s Q4 2024 earnings call on February 6, 2025)

3. Google

Google focuses on developer innovation. US-based hyperscaler Google secured 15% market share in 2024. Once seen as a top leader in AI in terms of technology advancements, the company has tried to recapture momentum in recent years. It aims to become the leading AI platform, focusing on developer innovation via Vertex AI and new data services. Vertex AI remains one of Google’s key AI solutions, allowing customers to fine-tune foundation models—both its proprietary Gemini models and models from other developers, including Anthropic and Meta, amongst others—while benefiting from Google’s extensive AI research and infrastructure.

Google earmarks billions of dollars for AI. On February 6, 2025, it announced a $75 billion AI investment in 2025 earmarked for capital expenditures, and in January 2025, it agreed to a $1 billion investment in generative AI startup Anthropic, building on its past investments of $2 billion in the startup.

4. OpenAI

OpenAI nears $300 billion valuation with new funding. US-based OpenAI continues to be a leading player in the generative AI market, with 9% share in the foundation models and model management platforms market.* Its early success in the generative AI sector, combined with their API services—which provide access to powerful models—has positioned OpenAI as a key provider of foundation models and model management platforms. The launch of ChatGPT significantly boosted the company’s visibility and market presence, contributing to substantial funding opportunities. As of February 2025, OpenAI and its strategic partners were nearing the completion of a $40 billion primary investment, bringing the company’s total post-money valuation close to $300 billion.

*Note: The revenue for OpenAI’s foundation models and model management platforms does not include revenue for its popular chatbot, ChatGPT, which IoT Analytics counts as a generative AI application.

OpenAI pursues AGI with enterprise focus and partnerships. OpenAI has prioritized high-performance AI with premium enterprise offerings, forming strong partnerships, notably with Microsoft. OpenAI’s strategy is centered around one single objective: developing artificial general intelligence (AGI), progressing from conversational AI to fully operational systems.

c) Emerging players

New challengers are reshaping the market

DeepSeek disrupts AI market with efficient R1 model. New challengers are reshaping the market, with China-based AI company DeepSeek emerging as a notable disruptor. Its latest model, R1, has garnered global attention for its exceptional efficiency and significantly lower inference costs. This breakthrough has sparked concerns along the generative AI value chain, such as semiconductor giants like NVIDIA, leading to a decline in their stock prices as investors reassess the long-term demand for high-end AI accelerators.

Hugging Face and Mistral AI push open-source AI. Open-source and open-weight models are gaining traction in the market. US-based open-source model platform provider Hugging Face and France-based open-source model developer Mistral AI are emerging as key players in this area. Hugging Face has built a robust ecosystem for accessible AI development, while Mistral AI focuses on high-performance, transparent AI models that challenge proprietary solutions. The strategies of these and most open-source model developers are centered on democratizing AI through open collaboration, reducing reliance on closed ecosystems.

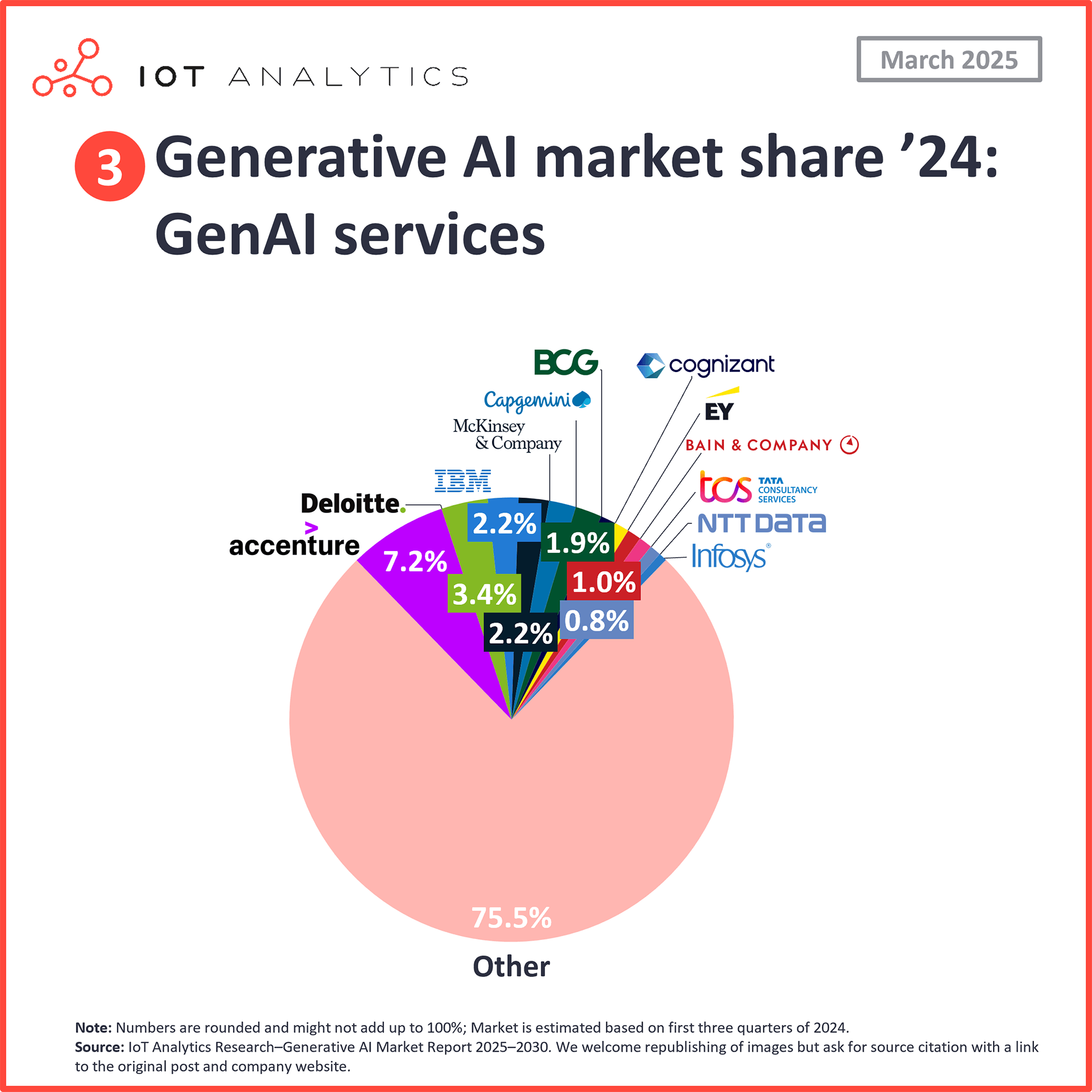

Market 3: Generative AI services

a) Market overview

Professional services target growing generative AI integration market. The generative AI services market represents a specialized segment dedicated to consulting, integration, and implementation support for organizations aiming to integrate generative AI capabilities. As companies increasingly look to integrate generative AI into their operations, professional services companies are sensing a large opportunity in helping companies formulate their generative AI strategies (e.g., what use cases to implement), advising them on technical architecture choices (e.g., which models to use) and helping them implement and build individual solutions.

Professional services companies are sensing a large opportunity

Generative AI services demand grows as firms seek expertise. IoT Analytics assesses that the generative AI services sector’s opportunity is now. Due to the novelty of generative AI, organizations often lack skills and experience, and the only option is to look for professional services firms that have built or are building up the required expertise.

Key quote

“GenAI is still driving many client discussions, and we engage in larger programs to deploy use cases at scale.”

Aiman Ezzat, CEO of Capgemini (during Capgemini’s Board of Directors meeting on July 26, 2024)

b) Leading generative AI services companies

The generative AI services market is more dispersed than the other two markets highlighted above.

1. Accenture

Accenture leads generative AI services with $3 billion investment. IoT Analytics estimates that Accenture, an Ireland-based professional services company, holds 7% market share, making it a relatively dominant force in the generative AI services market. The company has solidified its lead through a $3 billion AI investment aimed at accelerating enterprise AI adoption, developing AI-powered solutions, and enhancing internal AI integration. Accenture’s GenAI strategy revolves around being the first-mover go-to partner for AI-driven business transformation, emphasizing early adoption, proprietary AI frameworks, and specialized AI consulting services.

Accenture’s GenAI services surge with key partnerships. By the end of 2024, IoT Analytics estimates that Accenture’s GenAI services revenue increased 390% from the previous year—demonstrating the strong demand for its AI offerings. The company has also expanded its AI workforce, deploying 14 million AI training hours and executing strategic acquisitions to bolster its AI capabilities. Key partnerships with major AI players, including OpenAI, Microsoft, NVIDIA, and Google, further reinforce its market position.

2. Deloitte

Deloitte to invest $4 billion to expand AI services. IoT Analytics estimates that Deloitte, a UK-based multinational professional services firm, holds a relatively sizeable market share of 3% in 2024. The company is rapidly expanding its AI consulting division, with a strong focus on helping enterprises transition from proof-of-concept stages to full-scale AI implementation. The firm’s AI strategy revolves around embedding generative AI tools into core business functions, including R&D, product development, customer service, and financial reporting. To support this transformation, Deloitte has pledged $3 billion in generative AI investments through FY2030 and a $1 billion multi-year investment in AI-enabled delivery platforms and capabilities.

Deloitte’s 700 generative AI projects. By June 2024, Deloitte delivered over 700 generative AI projects, showcasing its ability to drive large-scale AI transformations. Deloitte has also developed a suite of AI-powered solutions and strong partnerships with industry leaders like NVIDIA, Google, AWS, and Oracle, further reinforcing Deloitte’s AI expertise.

3. IBM

IBM in third place. IoT Analytics estimates that IBM, a US-based IT and professional services giant, currently holds a 2% share in this market. The company has a strong focus on scalable, enterprise-grade AI deployments. IBM has centered its AI strategy around its watsonx platform, providing a suite of proprietary and open-source models that enable organizations to train, fine-tune, and deploy AI solutions tailored to their business needs.

IBM focuses on automation and responsible AI for enterprise solutions. IBM’s AI strategy prioritizes automation, hybrid cloud integration, and responsible AI, helping businesses leverage AI while ensuring compliance with industry regulations. The company focuses on three key generative AI use cases: digital labor transformation, customer experience enhancement, and application development/IT operations, with AI assistants like Watson Orchestrate and Watson Assistant driving efficiencies.

IBM leverages open-source AI and strategic partnerships for growth. IBM also emphasizes open-source collaboration, with its Granite foundation models fostering AI transparency and innovation. Its consulting services, combined with AI-powered solutions, support clients in healthcare, finance, and manufacturing, ensuring continued relevance in an evolving AI market. With strong partnerships with Microsoft, Oracle, and AWS, IBM believes it is in a good position to drive enterprise-scale AI adoption in the coming years.

c) The many others

Consulting firms expand AI services for industry-specific solutions. Beyond the major consulting giants, several other firms are making significant strides in the generative AI services space. Professional services companies such as US-based McKinsey (estimated 2%), US-based BCG (estimated 2%), US-based Cognizant (estimated 1%), and France-based Capgemini (estimated 1%) have expanded their AI-focused service offerings, tailoring solutions for industry-specific AI adoption.

Professional services firms generally follow a strategy of embedding AI-driven insights into digital transformation efforts, optimizing AI governance, and enabling scalable AI deployments for clients. Their approach is to provide strategic consulting, implementation support, and managed AI services, aiming to help businesses leverage AI technology effectively within their operational frameworks.

Strategy firms help shape CEO-driven generative AI initiatives. Strategy consulting specialists stand out in this space, notably McKinsey, BCG, and Bain & Company, as they have an exceptionally high share in this market compared to their overall size. This is because AI initiatives are mostly CEO-driven, so these companies are currently in high demand for shaping corporate AI strategies.

Generative AI company landscape outlook

Generative AI adoption is growing rapidly across industries. As part of its research for the Generative AI Market Report 2025–2030, IoT Analytics spoke with 50+ experts in the field and gathered information on 530+ generative AI projects, analyzing which industries and departments are quick to adopt generative AI and which vendors are most selected today.

The results? The teams found that the generative AI market is very dynamic and evolving rapidly, with new advancements constantly being announced. In the short time since IoT Analytics published its second generative AI report—the Generative AI Market Report 2025-2030—in late January 2025, more powerful foundation models have emerged, e.g., OpenAI’s o3-mini and DeepSeek’s R1.

AI competition intensifies as new models challenge incumbents. The competitive landscape of generative AI is also dynamic and evolving, driven by innovation in both foundation models and underlying hardware. Companies focusing on optimized architectures and novel training methodologies are beginning to challenge the status quo, forcing incumbents to adapt. Case in point, the emergence of more cost-effective and power-efficient AI models like DeepSeek R1 has signaled a shift in industry dynamics, with companies like NVIDIA experiencing increased volatility despite their dominant position (e.g., NVIDIA’s stock was down over 13% since the beginning of the year, as of March 3, 2025). Further, though generative AI applications were not covered above,* it is worth noting that even OpenAI’s ChatGPT—the clear leader in monetized consumer- and enterprise-facing generative AI applications—was rattled by the release of R1, losing its spot as the Apple App Store’s top downloaded app to Deepseek’s AI Assistant app for a short time (as of 27 February 2025, ChatGPT had reclaimed this spot, and Deepseek’s app was ranked 38th).

*Note: IoT Analytics plans to publish a separate blog on generative AI use cases. Those interested in reading the article when released can sign up for IoT Analytics’ IoT Research Newsletter by clicking below.

The current AI hype may be comparable to the Dot-Com bubble

Generative AI’s success depends on real-world value. There is still a lot of movement to be had in the generative AI company landscape. Even Microsoft CEO Satya Nadella has recently warned that the current AI hype may be comparable to the 1999 Dot-Com bubble. The next year will reveal how many of the new generative AI offerings deliver value besides just being a marketing coup or how many of those currently in the proof-of-concept state will move forward. Organizations that strategically adopt AI may gain a significant competitive advantage as AI capabilities continually become embedded across industries. With ongoing technological advancements and expanding enterprise adoption, the future of generative AI looks more promising than ever. IoT Analytics will stay on top of this space, with a follow-up report expected in late 2025 or early 2026.

Disclosure

Companies mentioned in this article are used as examples to showcase the trends discussed. No company paid or received preferential treatment in this article, and it is at the discretion of the analyst to select which examples are used. IoT Analytics makes efforts to vary the companies and products mentioned to help shine attention to the numerous IoT and related technology market players.

It is worth noting that IoT Analytics may have commercial relationships with some companies mentioned in its articles, as some companies license IoT Analytics market research. However, for confidentiality, IoT Analytics cannot disclose individual relationships. Please contact compliance@iot-analytics.com for any questions or concerns on this front.

More information and further reading

Are you interested in learning more about the generative AI market?

Generative AI Market Report 2025-2030

A 263-page report on the enterprise Generative AI market, incl. market sizing & forecast, competitive landscape, end user adoption, trends, challenges, and more.

Already a subscriber? View your reports here →

Related articles

You may also be interested in the following articles:

- DeepSeek R1’s implications: Winners and losers in the generative AI value chain

- Who is winning the cloud AI race? Microsoft vs. AWS vs. Google

- AI 2024 in review: The 10 most notable AI stories of the year

Related publications

You may also be interested in the following reports:

- List of generative AI projects 2025

- State of IoT Spring 2025

- IoT System Integration and Professional Services Market Report 2024–2030

- Quarterly trend report: What CEOs talked about in Q4 2024

- Global Cloud Projects Report and Database 2024

Related market trackers

You may be interested in the folllowing trackers:

Subscribe to our research newsletter and follow us on LinkedIn to stay up-to-date on the latest trends shaping the IoT markets. For complete enterprise IoT coverage with access to all of IoT Analytics’ paid content & reports, including dedicated analyst time, check out the Enterprise subscription.