In short

- The global smart manufacturing market reached $175 billion in 2025, according to IoT Analytics’ Industry 4.0 & Smart Manufacturing Market Report 2026–2030 (published March 2026).

- IoT Analytics projects the market to grow at a CAGR of 9.3% until 2030, reaching $274 billion.

- In 2026, the top 10 smart manufacturing technology vendors are prioritizing software-defined, AI-infused architectures, but their approaches differ.

In this article

- Smart manufacturing market snapshot and outlook

- Comparing the top 10 smart manufacturing vendors

- Deep dive: The top 10 vendors

- Further analysis

- Global smart manufacturing market by segment and technology (Insights+)

- Growth vs maturity of smart manufacturing technologies (Insights+)

- Top 20 smart manufacturing vendors (Insights+)

- Key segments for the top 20 smart manufacturing vendors (Insights+)

- 3 key action items from this report for strategists, product managers, marketers, and salespeople (Insights+)

Smart manufacturing market snapshot and outlook

Industrial AI is reviving the smart manufacturing technology market. Early evidence suggests that industrial AI is beginning to re-energize the smart manufacturing market, with data management/platform, AI platform, and AI-related investments such as mobile robotics increasingly driving market growth, according to IoT Analytics’ 406-page Industry 4.0 & Smart Manufacturing Market Report 2026–2030 (published March 2026). The global smart manufacturing market (hardware, software, and services) stood at $175 billion in 2025 and is projected to reach $274 billion by 2030, growing at 9.3%.

Smart manufacturing interest has seen steady increase. Over the past decade, interest in smart manufacturing has increased strongly (with Google searches for “smart manufacturing” up 1,900% since 2016). Since mid-2025, we have been witnessing a renewed wave of interest in the topic, driven by US-based semiconductor company NVIDIA‘s push into physical AI, a term that describes AI systems designed to operate in and interact with the physical world. Physical AI reflects a broader shift in how manufacturers and technology vendors are thinking about AI’s role on the factory floor, moving it from data analytics toward systems that can take action in real-world environments.

Over 25 submarkets make up the smart manufacturing market. IoT Analytics categorizes the smart manufacturing market into 3 segments with a total of 26 individual submarket models:

- The core tech stack – includes underlying hardware/edge technology such as PLCs, IPCs, DCS systems), key platforms/middleware (such as industrial DataOps and AI platforms), industrial cybersecurity, and key applications such as MOM or APM. Together, this category holds a 55% share and is projected to grow at 8.7% CAGR until 2030;

- Professional services market – represents 28% of the market and is expected to grow at a 9.2% CAGR;

- Supporting technologies – tech that is not part of the core tech stack but often supports smart manufacturing technologies, including stationary robotics, machine vision, and autonomous mobile robots, making up 17% of the total market and expected to grow at 9.4% CAGR.

5 forces are driving smart manufacturing market growth:

- Cost pressure. Manufacturers face sustained margin pressure from rising labor, energy, and material costs, pushing them to improve overall equipment effectiveness, reduce scrap, and cut energy consumption.

- World events. Geopolitical tensions and supply chain disruptions are accelerating reshoring and regional production strategies. As a result, new factories are built, some of which require great automation technology as they are in higher-cost manufacturing locations.

- Skill issues. Chronic labor shortages and demographic shifts in skilled trades are pushing companies to deploy technology as a substitute for or complement to human workers.

- Maturation of technologies. The maturation of industrial connectivity, edge computing, cloud platforms, and standardized protocols is enabling tighter integration between production systems and enterprise IT, a shift referred to as IT/OT convergence.

- AI. AI is increasingly driving growth, and the C-suite is demanding that teams implement it and show results.

Insights in this article are derived from

Industry 4.0 & Smart Manufacturing Market Report 2026–2030

A 406-page report analyzing the global smart manufacturing market, with a deep dive into 25 key technologies, 52 individual trends, and the competitive landscape of 240+ vendors.

Already a subscriber? View your reports and trackers here →

Market leaders setting pace in a broad and specialized market. IoT Analytics monitors more than 750 companies that actively sell smart manufacturing technology or services. The top 20 vendors account for less than half of the total market revenue. Not all market leaders compete head-to-head in each market. In fact, some of the leading vendors sell only one service in the market (e.g., Accenture, the market leader in smart manufacturing professional services), while others have a broad portfolio (e.g., Siemens, with a presence in nearly half of the 26 markets). The following analysis examines the top 10 vendors setting the tone for this market in 2026.

Smart manufacturing defined

Smart manufacturing is the use of digital and automation technologies to improve manufacturing operations across the value chain. It comprises (A) core smart manufacturing technology stack elements, (B) supporting technologies, and typically results in solutions/use cases that make production environments more responsive, interoperable, and better suited to improving key operational KPIs such as OEE.

Smart manufacturing market scope

In IoT Analytics’ view, the smart manufacturing market comprises 26 segments spread across 3 categories: tech stack elements, supporting technologies, and services.

The 26 submarkets:

Smart manufacturing tech stack elements

A. Edge

1. Field instruments

2. Remote I/Os

3. HMIs

4. PLCs

5. DCSs

6. Gateways

7. IPCs

B. Platforms/middleware

8. Message brokers

9. Device management

10. Application management

11. Data management

12. Industrial DataOps

13. AI platforms

14. Protocol converters

C. Applications

15. Industrial automation software

16. MOM

17. Asset performance & management

18. Factory logistics

19. Security

Supporting technologies

20. Additive manufacturing

21. Stationary robots

22. Autonomous mobile robots

23. Machine vision

24. Augmented reality

25. Humanoid robots

Services

26. Professional services

Comparing the top 10 smart manufacturing technology vendors

Industrial AI has become the priority for the top smart manufacturing technology vendors. The latest analysis shows that the top vendors are broadly united by a transition away from pure hardware toward software-defined, AI-infused architectures. Software-defined automation and industrial AI are key priorities for nearly all top-10 vendors in 2026 as some start to paint a vision of industrial sites moving to perception-driven, autonomous operations.

| Rank | Vendor | HQ country | Market share range (2024) | Key offerings | Largest manufacturing segments | Q4 2025 YoY revenue growth (segment) | Strategy and key priorities going forward | |

|---|---|---|---|---|---|---|---|---|

| 1 | ABB | SUI | 5%–10% | – PLCs – DCS – Field instruments – Remote I/Os – HMI – Gateways | – IPCs – AI platforms – IAS – MOM – APM – Robotics | – Energy/Power – Chemicals | +25% (Process Automation/ Automation) | – Shifting to a software-centric model and perception-driven autonomous operations – Advancing perception-driven autonomy (OmniCore) and standardizing on the Ability Genix platform |

| 2 | Siemens | GER | 5%–10% | – PLCs – DCS – Field instruments – Remote I/Os – HMI – Gateways | – IPCs – AI platforms – Industrial DataOps – IAS – MOM – Security software | – Machinery and equipment – Automotive – Electronics | +15% (Digital Industries) | – “ONE Tech Company” approach integrating software, edge computing, and AI to “automate automation” – Investing >€1 billion in industrial AI over 3 years; advancing the Industrial Copilot |

| 3 | Emerson | USA | 5%–10% | – PLCs – DCS – Field instruments – Remote I/Os – HMI | – Gateways – Industrial DataOps – IAS – APM – Security software | – O&G – Chemicals – Power and water (utilities) | +2% (Control Systems & Software) | – “Boundless Automation” through a software-defined platform (Project Beyond) •Focusing on deterministic, mission-critical workflows |

| 4 | Schneider Electric/ AVEVA | FRA | 2%–5% | – PLCs – DCS – Field instruments – Remote I/Os – HMI | – IPCs – IAS – MOM – APM – Gateways | – F&B – Machinery and equipment – Energy and utilities | +6% (Industrial Automation) | – Open, software-defined automation (SDA) and Industry 5.0 (human-AI augmentation) |

| 5 | Honeywell | USA | 2%–5% | – PLCs – DCS – Field instruments – Remote I/O | – Factory logistics – HMI – IAS | – O&G – Chemicals – Pulp and paper | -8% (Industrial Automation) | – “Automation to Autonomy” roadmap anchored on Honeywell Forge and Honeywell Digital Prime – Transitioning into a pure-play automation company (aerospace spin-off Q3 2026) via focus on a “trifecta” of AI, connectivity (5G), and cloud-edge convergence |

| 6 | Rockwell Automation | USA | 2%–5% | – PLC – DCS – HMI – IAS | – Remote I/O – IPCs – Security software | – Automotive – F&B – Life sciences | +19 (Software & Control) | – Transitioning to modular SaaS delivery via cloud marketplaces (e.g., FactoryTalk Hub on AWS) •Integrating GenAI copilots into tools like FactoryTalk DesignStudio to autonomously generate and fix code |

| 7 | Accenture | IRL/USA | 2%–5% | – Professional services | – Automotive – Consumer goods – Energy and utilities | +10% | – Industry X practice as the I4.0 delivery vehicle. •Co-developing AI-native industrial solutions through strategic partnerships, such as the 7,000-person Accenture Siemens Business Group | |

| 8 | Yokogawa | JPN | 2%–5% | – PLCs – DCS – Field Instruments – Remote I/O | – HMI – IAS – APM – Security software | – O&G – Chemicals – Power and energy | +6% (Control) | – IA2IA (Industrial Automation to Industrial Autonomy), a 6-level maturity model used as both a consulting framework and I4.0 delivery methodology across process industries – Scaling commercial deployment of autonomous control AI across process industries while pivoting toward a recurring revenue model via Yokogawa Cloud and OpreX services |

| 9 | Mitsubishi Electric | JPN | 2%–5% | – PLCs – DCS – Remote I/O – HMI | – Gateways – IPCs – IAS – Fixed Robots | – Automotive – Semiconductor and electronics – F&B | +10% (Factory Automation) | – e-F@ctory as Mitsubishi’s IT/OT convergence architecture, connecting controllers and edge devices through CC-Link IE TSN to enterprise systems. – Maisart (compact, edge-deployable AI) is embedded throughout •Complement e-F@ctory with composable, AI-native frontline operations software (Tulip) |

| 10 | Endress+ Hauser | SUI | 2%–5% | •Field Instruments | – Chemicals – F&B – O&G | N/A | – Leveraging Netilion IIoT ecosystem for lifecycle and asset management services across the multi-vendor installed base | |

Smart manufacturing spans a vast multivendor landscape. While the table above highlights the top 10 market leaders, it is important to note that the smart manufacturing market remains a highly diverse ecosystem, with over 750 identified vendors providing solutions, products, and services across the stack (and many other smaller companies selling into the market). According to the Industry 4.0 & Smart Manufacturing Market Report 2026–2030, many of the larger industrial manufacturers (from automotive to oil & gas) employ dozens of different vendors across their hardware/edge stack, and sometimes more than 100 different software vendors, as individual plants/sites standardize on different ecosystems.

Deep dive: The top 10 smart manufacturing technology vendors

ABB

Switzerland-based ABB’s strong position in industrial robotics, industrial automation, and software makes the company the leading smart manufacturing vendor. With the sale of the robotics division to SoftBank (October 2025), ABB will almost certainly not occupy the top spot once the acquisition closes.

ABB’s current strategy centers on a software-driven model and the advancement of perception-driven autonomous operations. The company is standardizing on its Ability Genix platform and prioritizing partnerships for the AI era. Based on an IoT Analytics interview with ABB Automation’s Chief Digital Officer, Rajesh Ramachandran, the software-centric pivot has already been highly successful, with ABB’s Digital and AI business growing nearly 5x over the past 5 years (while overall company revenue saw a +1.5% CAGR from 2023–2025).

“Genix is at the core of our digital strategy—it’s an AI-driven industrial platform that connects systems, drives operational excellence, and scales across industries. With over 50 AI applications built on Genix, we’re now transforming how customers run their operations.”

Rajesh Ramachandran, Chief Digital Officer, ABB Automation (from interview)

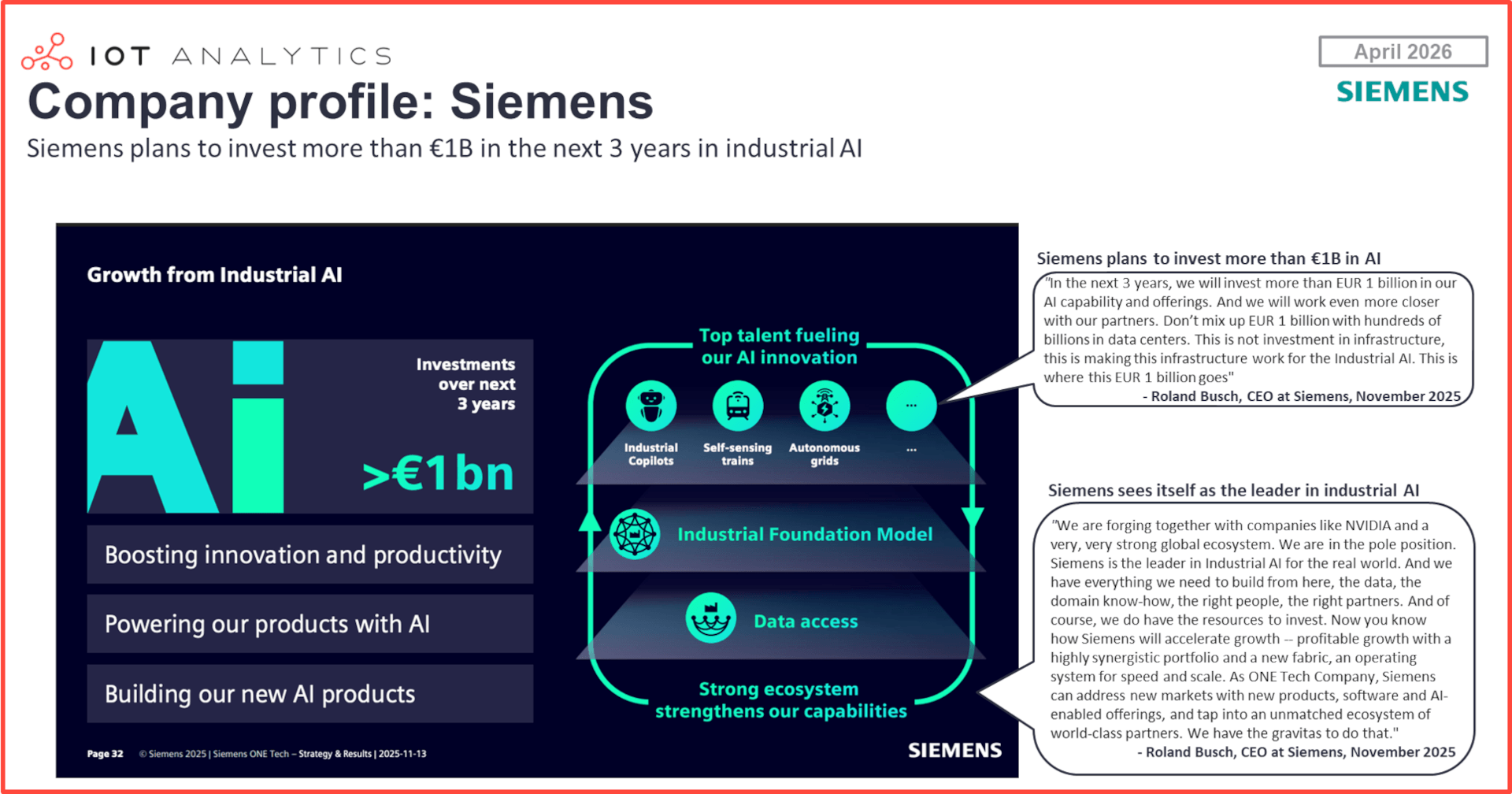

Siemens

Germany-based Siemens is the market leader in discrete automation and industrial software. The company is executing its “ONE Tech Company” program, an overarching strategy to create a unified data, technology, and sales fabric across its entire organization, which some speculate may lead to a Siemens reorganization in the coming months. A massive priority for Siemens is industrial AI, with the company committing over €1 billion to AI capabilities over the next 3 years. Siemens is also moving to “automate automation,” having already released or announced over 20 industrial copilots as part of its portfolio (e.g., Siemens Engineering Copilot) that help engineers generate and debug PLC code.

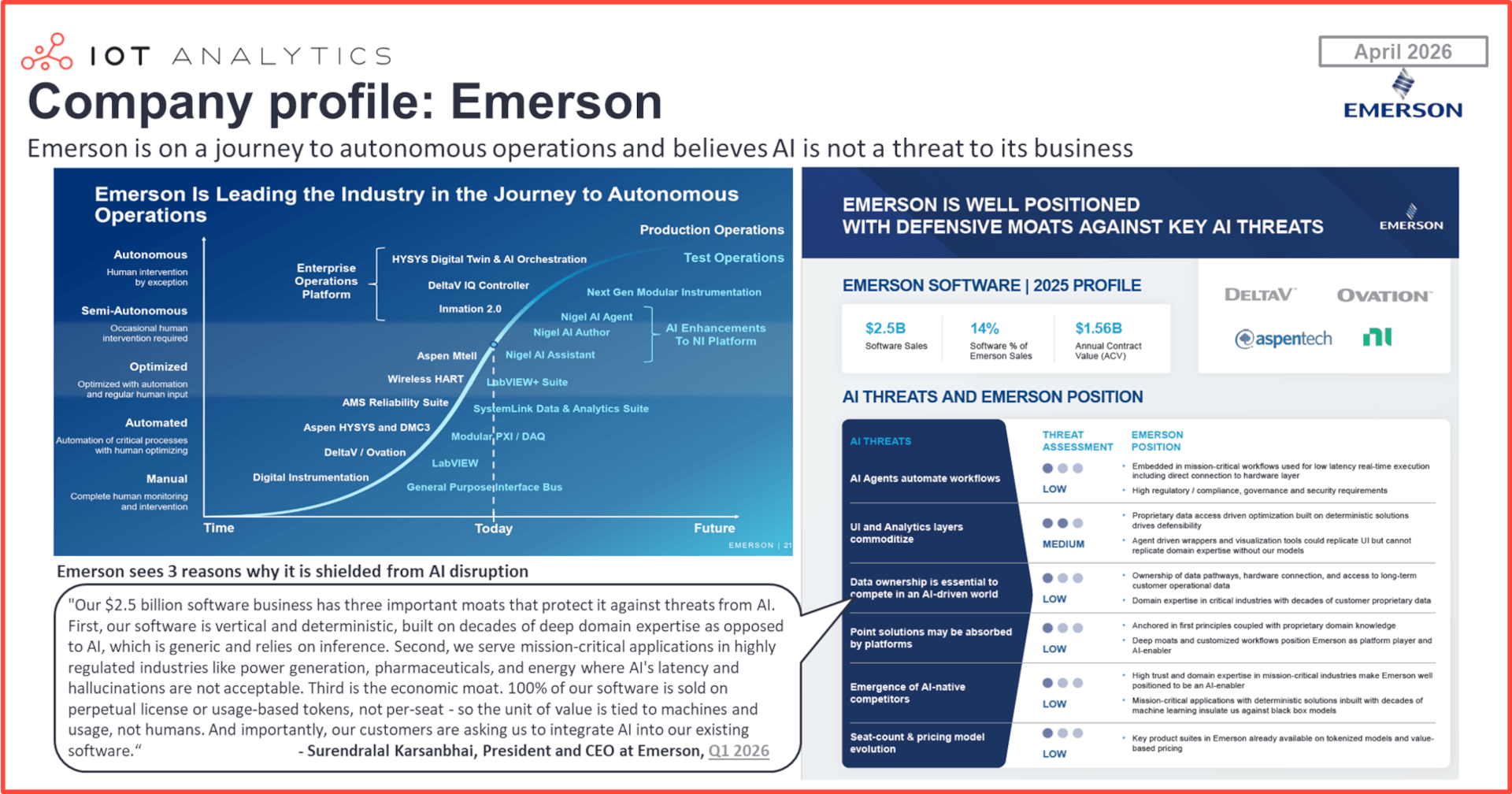

Emerson Electric

US-based Emerson is expanding its footprint beyond traditional control hardware to become a robust industrial software provider, leveraging its $2.5 billion software business (which now accounts for 14% of its total sales). This expanding software and industrial AI portfolio is supported by key company assets, including AspenTech (acquired by Emerson in March 2025) and NI (acquired in October 2023), as well as its DeltaV and Ovation control platforms.

The company recently signaled that it is building “defensive moats” against generic AI tools by prioritizing deterministic, mission-critical workflows where AI hallucinations are unacceptable. Emerson today sells 100% of its software on perpetual licenses or usage-based tokens rather than per-seat pricing.

During its 2025 Investor Conference, Emerson highlighted its complete transformation from a diversified industrial conglomerate into a “Global Automation Leader” with a core vision of “Engineering the Autonomous Future.” Leadership introduced a three-pillar “Value Creation Framework” that prioritizes organic growth, operational excellence, and a major capital-allocation pivot, aiming to return $10 billion to shareholders by 2028. Technologically, this strategy is underpinned by investments in an Enterprise Operations Platform and a new “Multi-Agent AI Architecture” designed to break down data silos across safety, reliability, control, and optimization workflows.

Schneider Electric/AVEVA

France-based Schneider Electric is driving its smart manufacturing strategy, among other things, through the EcoStruxure Automation Expert platform and its AVEVA software portfolio (including AVEVA Connect and AVEVA MES), championing an open, software-defined automation (SDA) approach. By leveraging the IEC 61499 standard, EcoStruxure Automation Expert creates an open, interoperable architecture, enabling customers to achieve new levels of performance that, according to Schneider Electric, traditional closed systems cannot match.

A primary priority is the deep integration of sustainability and AI; To further its AI and data orchestration priorities, AVEVA is embedding a GenAI operator’s copilot into Operations Control and recently partnered with Databricks to create a shared, cross-cloud AI workspace for high-quality industrial data.

Honeywell

US-based Honeywell is undergoing a significant structural transformation. In October 2024, CEO Vimal Kapur announced plans to split the company into three independent entities. Solstice Advanced Materials has already been spun off, and Honeywell Aerospace is expected to become a standalone pure-play aerospace company in Q3 2026. The remaining entity will form a pure-play automation company organized across building automation, industrial automation, and process automation & technology.

Honeywell’s I4.0 strategy is anchored on an “Automation to Autonomy” transition, built around two flagship platforms: Honeywell Forge (IoT/AI analytics) and Honeywell Digital Prime (lifecycle management). The underlying technology architecture rests on what Kapur termed a “technology trifecta”: the convergence of AI, 5G connectivity, and cloud-edge computing, supported by strategic partnerships with Microsoft, Google, and Qualcomm. The company plans to focus exclusively on mission-critical automation segments, and “build and mine” the installed base by expanding AI-enabled aftermarket services and software delivered via Forge, targeting a roughly 50/50 hardware-to-software-and-services revenue mix over time.

Rockwell Automation

US-based Rockwell Automation is integrating generative AI into its foundational software ecosystem. A key priority is its GenAI copilot, which is embedded directly into FactoryTalk DesignStudio to help users autonomously generate and fix automation code.

This integration of AI directly supports the strategic vision outlined by Rockwell Automation executives at the 2025 Automation Fair:

- Driving the shift to autonomy: Chairman and CEO Blake Moret emphasized that AI, software-defined automation, and robotics are the foundation for a revolution in industrial operations. Tools that autonomously generate code are a prime example of how the company is guiding the industry’s shift from traditional automation to true industrial autonomy.

- Rethinking industrial design: Chief Technology Officer Cyril Perducat noted that unlocking the value of tomorrow’s operations requires rethinking how we design and build equipment and factories today. Embedding generative AI directly into foundational design software perfectly illustrates this new approach to building the “Future of Industrial Operations”.

- Meeting manufacturing challenges: Matheus Bulho, Sr. Vice President of Software & Control, highlighted that the industry is increasingly relying on AI and digital transformation strategies to achieve results. Integrating a GenAI copilot directly addresses the driving forces behind today’s biggest manufacturing challenges by streamlining software and control development.

Accenture

US-based Accenture stands out in the top 10 as a pure-play professional services vendor, with 100% of its smart manufacturing portfolio dedicated strictly to consulting, system integration, and managed/operational services

The company focuses on helping industrial firms navigate highly complex digital transformations, such as IT/OT convergence, cloud migration, cybersecurity compliance, and the deployment of AI.

A massive priority for Accenture is co-developing software-defined factories through strategic ecosystem partnerships. Most notably, in March 2025, Accenture and Siemens launched the Accenture Siemens Business Group, dedicating a 7,000-person team specifically to building software-defined products and factories with deep AI integration.

Yokogawa

Japan-based Yokogawa is a process automation specialist with strength in industries such as chemicals, oil & gas, pharmaceuticals, and power. The company’s I4.0 strategy is organized around a proprietary framework called IA2IA (Industrial Automation to Industrial Autonomy), a six-level operational maturity model that guides customers from manually operated facilities toward fully autonomous operations, functioning as both a strategic roadmap and an active consulting delivery methodology in customer engagements.

A highlight of IA2IA is Yokogawa’s proprietary FKDPP (Factorial Kernel Dynamic Policy Programming), a reinforcement learning AI co-developed with Nara Institute of Science and Technology, which autonomizes process control operations. First commercially deployed at ENEOS Materials in 2023, FKDPP is now scaling to other deployments. The latest generation of the CENTUM VP DCS (marking its 50th anniversary in 2025) was launched with autonomous control AI embedded directly at the DCS layer. Yokogawa has also been broadening the OpreX portfolio with the addition of OpreX Plant Stewardship (April 2025), covering safety, reliability, regulatory compliance, and operational efficiency, indicating a shift from product-centric maintenance toward outcome-based service contracts.

Mitsubishi Electric

Japan-based Mitsubishi Electric approaches Industry 4.0 through two pillars: e-F@ctory and Maisart. e-F@ctory is the company’s IT/OT convergence architecture, connecting controllers and edge devices through CC-Link IE TSN network, supported by an alliance of over 450 partner companies. Maisart is the company’s proprietary AI brand, engineered to run on compact, edge hardware. The Maisart program is supported by Mitsubishi Electric Research Laboratories, the company’s global R&D arm with facilities in the US and Europe.

In January 2026, the company led a $120 million Series D investment in Tulip Interfaces, an AI-native, no-code frontline operations platform, forming a strategic alliance to deploy Tulip’s composable applications alongside Mitsubishi Electric’s automation hardware.

“Tulip Interfaces’ composable platform development technology will enable us to respond to the speed and flexibility demanded by manufacturing sites. By combining the technologies that both companies possess, we aim to accelerate DX and innovation as well as strengthen our competitiveness beyond the boundaries of the manufacturing industry.”

Satoshi Takeda, SVP and CDO, Mitsubishi (source)

Mitsubishi Electric’s largest acquisition to date, Nozomi Networks, completed in January 2026 (approximately $883M), adds the market-leading OT/IoT asset visibility and threat detection platform to its portfolio. The deal supports the company’s goal of building a “One-Stop OT Security Solution.”

Endress+Hauser

Switzerland-based Endress+Hauser is the only pure-play field instrumentation vendor and the only family-owned company in the top 10, headquartered in Reinach, Switzerland. Its I4.0 strategy rests on leveraging 1) Netilion IIoT ecosystem to convert its large global installed base of field instruments into a recurring digital revenue stream and 2) expanding its physical measurement portfolio into decarbonization and gas measurement through strategic partnerships rather than organic product development alone.

Netilion is Endress+Hauser’s cloud-based IIoT platform, providing digital device twins (Netilion Analytics), remote asset health diagnostics (Netilion Health), and process data services across multi-vendor plants. The system creates digital twins of field instruments, drawing on a database of over 40 million device records, and provides plant operators with visibility into installed base status, obsolescence risk, and maintenance scheduling.

Further analysis

Below in our Insights+ section, we dive deeper into the Industry 4.0 & Smart Manufacturing Market Report 2026–2030, including:

- The global smart manufacturing market by segment

- Growth vs maturity of smart manufacturing technologies

- The top 20 smart manufacturing vendors (overall and by segment)

- A comparison of the 2024 and projected 2030 global smart manufacturing market by technology

- 12 key action items for strategists, product managers, marketers, and salespeople based on the findings in the report.

Access key market data for $99/month per user

The Insights+ Subscription unlocks exclusive facts & figures. You will gain access to:

- Additional analyses derived directly from our reports, databases, and trackers

- An extended version of each research article not available to the public

Full report access not included. For enterprise offerings, please contact sales: sales@iot-analytics.com