In short

- A “reshoring boom” due to the US’s widespread tariffs has not happened, based on macro data as part of IoT Analytics’ 34-page Industrial Macro Pulse – May 2026 report.

- In general, US manufacturing construction spending has steadily declined since 2024, driven by a 44% slowdown in spending on electronics factories and semiconductor fabs since their peak in mid-2024.

- Discounting the electronics sector, there was a 5.6% jump in manufacturing construction spending since the start of the tariffs—lower than would be expected for a boom.

- Still, the report offers positive signs for US manufacturing health and shows that data centers and power generation & infrastructure are the real stories of US industrial growth.

Why it matters

- What companies announced in response to tariffs and what the data presents a year later have diverged, and this divergence has implications for capex planning, supplier strategy, and where the next demand wave will land.

In this article

- Anticipation of a manufacturing “reshoring boom”

- US factory construction: On the decline

- Other macroeconomic indicators: No boom visible

- Analyst takeaway: There is no US manufacturing boom, but there is a data center boom and possibly soon a power/grid boom

- The real industrial building construction story: data centers, not factories

- The next construction boom: Power infrastructure

- Further analysis

- US manufacturing orders (Insights+)

- Industrial automation lead times (Insights+)

Anticipation of a manufacturing “reshoring boom”

Tariffs led to US manufacturing onshoring/reshoring commitments. In February 2025, US President Donald Trump began imposing tariffs on China, Canada, and Mexico. Then in April 2025, he announced widespread tariffs on nearly every country, calling the move Liberation Day for the US.

A month later, IoT Analytics published the report The Evolving Tariff Landscape: Impact on the Economy and Businesses. The analysis found that, as a result of these tariffs, a large number of CEOs of public companies began committing to reshoring to the US to avoid the tariffs and benefit from local production. In Q2 2025 alone, 227 public industrial firms announced footprint changes, the majority expanding within the US or towards the US. 87 companies expanding existing US operations, 33 said they would move production from China to the US, and 13 said they would relocate from Mexico or Canada to the US.

Some commitments from these companies include:

RTX

“Over the last five years, we’ve invested nearly $10 billion to enhance our domestic manufacturing footprint and capabilities. And this year, we’re planning another $2 billion of investment to further increase our US capacity.”

Chris Calio, CEO and President, RTX, April 2025 (source)

Apogee Enterprises

“In services, we will be closing our Toronto manufacturing site and aligning resources to support growth in the US. In metals, we will continue to optimize our footprint and make organizational changes to gain more efficiency.”

Ty Silberhorn, CEO, Apogee Enterprises, Inc., April 2025 (source)

Despite ongoing uncertainty about the validity and legal basis of these tariffs, the main question a year later is:

Is there evidence of a manufacturing reshoring boom in the US?

The White House surely believes so. An April 22, 2026, press release titled “Trump Effect: American Manufacturing Is Roaring Back as Factory Activity Hits Four-Year High” states that the US is seeing “the largest reshoring wave in American history as companies invest trillions to build and expand here at home.” A leading indicator for that statement is the ISM Manufacturing PMI, which in March 2026 reached a multi-year high at 52.7.

The latest IoT Analytics report, Industrial Macro Pulse – May 2026, examines recent US manufacturing construction data, among other indicators of industrial activity. Based on the data in the report, IoT Analytics concludes that it is too early to call out a “reshoring boom” in the US. The data show a strong manufacturing sector, but no boom.

Commenting on the findings of the analysis, IoT Analytics CEO Knud Lasse Lueth says:

“It is striking that over the past 12 months, dozens of manufacturing CEOs have publicly committed to expanding US manufacturing capacity, fueling considerable optimism across the industrial sector. Yet one year later, the leading indicators still show little evidence of a reshoring-driven manufacturing boom beyond what could be explained by a normal cyclical industrial upswing.”

US factory construction: On the decline

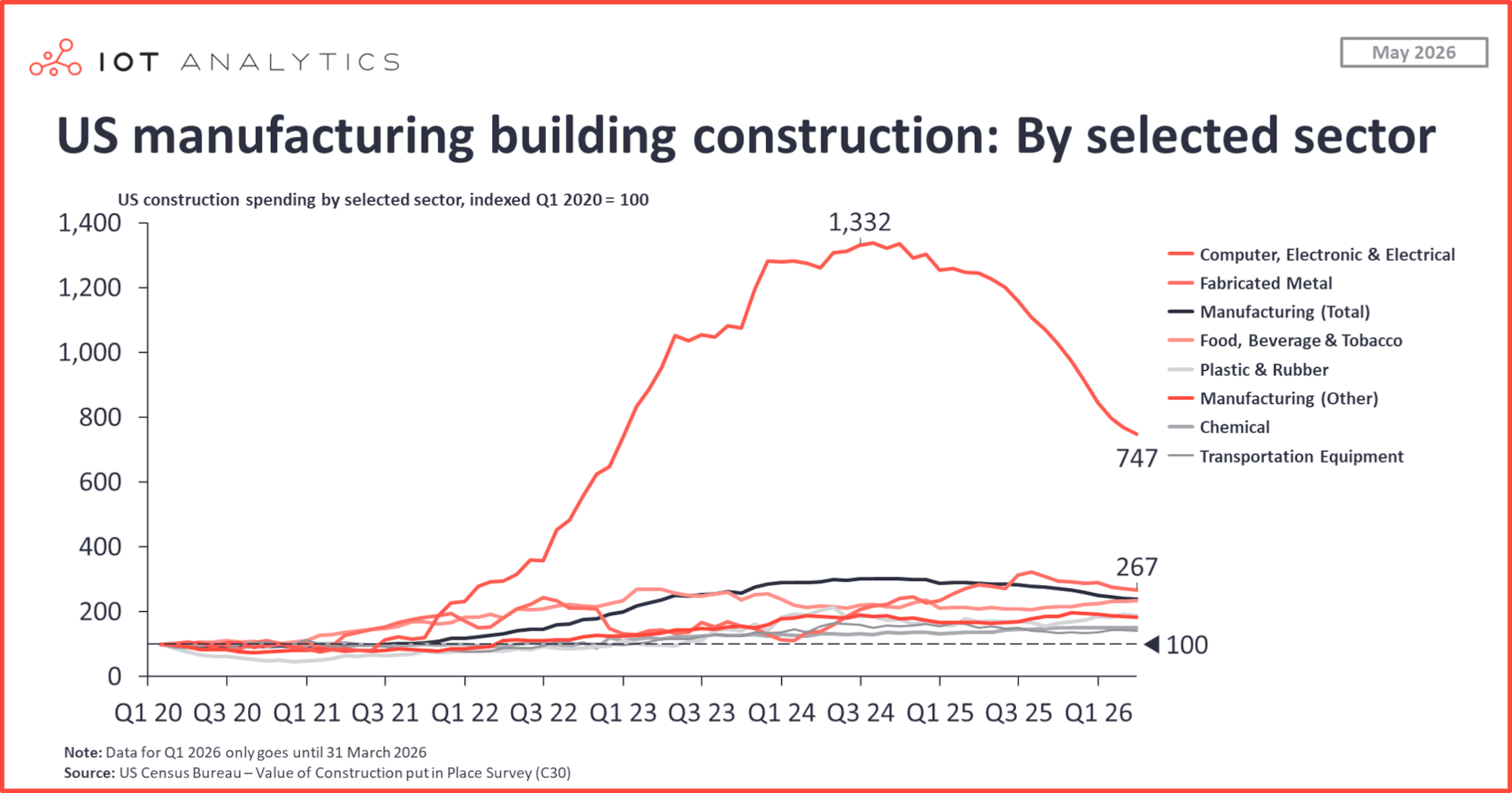

Manufacturing construction spending generally down, dragged down by electronics. Spending on manufacturing construction in the US reached $239 billion in June 2024, according to the US Census Bureau’s Value of Construction Put in Place (or VIP) survey. Since then, spending has declined 21%. This decline is largely attributed to a sharp decline in construction spending in the computer, electronic, and electrical (CE&E) sector, down 44% since its peak in July 2024. Propelled by the 2022 CHIPS Act, this sector accounted for over half of manufacturing construction spending at its peak, but semiconductor fab construction spending has since come down.

Manufacturing construction spending up for most sectors. Looking deeper into the period after the tariffs started, and excluding CE&E from the equation, spending on manufacturing construction increased 5.6% between February 2025 and March 2026, with 3 of 7 selected sectors, along with the remaining sectors collectively, experiencing growth:

- Plastic & rubber – up 6%

- Chemical – up 10%

- Food, beverage & tobacco – up 10%

- Manufacturing (Other) – up 10%

Aside from CE&E, the following sectors experienced a decline since the start of the tariffs:

- Fabricated metal – down 2%

- Nonmetallic minerals – down 22%

- Transportation equipment – down 12%

Inflation chips away at construction spending growth. A 5.6% jump is a positive sign of manufacturing economic activity, but it is not what we would expect with a “reshoring boom.” Additionally, it is worth noting that the VIP survey captures only nominal dollars spent; it does not account for inflation. Annual inflation in the US in March 2026 (so starting in March 2025, just after the initial tariffs took effect) was approximately 3.3%, which chips away at the value of new construction spending and brings adjusted spending growth to approximately 2.3%.

Other macroeconomic indicators: No boom visible

Manufacturing employment and import ratio further support lack of “reshoring boom.” With manufacturing construction as a leading indicator of growth, it is not surprising that other (lagging) indicators, such as employment and imports/exports, also do not support the thesis of a manufacturing reshoring boom. Data from the US Federal Reserve Economic Data (FRED) show that manufacturing employment has declined 1% since the widespread “Liberation Day” tariffs, with only a slight uptick in the latest (February/March 2026) numbers. Meanwhile, Kearney’s Reshoring Index, which measures YoY change in the US manufacturing import ratio, shows that while 2025 was a slightly better year than 2024 for the US (from -115 to -86), the US remained well in negative territory, and manufactured goods output dropped 0.4 percent.

Analyst takeaway: There is no US manufacturing boom, but there is a data center boom and possibly soon a power/grid boom

IoT Analytics analyst Joaquin Fernandez performed the analysis found in the Industrial Macro Pulse – May 2026, which provides the current global economic outlook and projections, identifies expanding and contracting manufacturing economies, shares current component lead times, and gives insights into order books across key industrial sectors.

While there is no evidence of a US manufacturing boom, there is evidence that some of the companies that announced changes to their operational footprint in the US are following through. For example, Apogee closed its plant in Brampton, Ontario, in September 2025 as part of its effort to optimize its manufacturing footprint that serves the northern US.

Additionally, the data show some positive upswings in US manufacturing, as covered in the Insights+ sections below. Here, we show where the real current and future industrial construction booms are: data centers and power infrastructure.

The real industrial building construction story: data centers, not factories

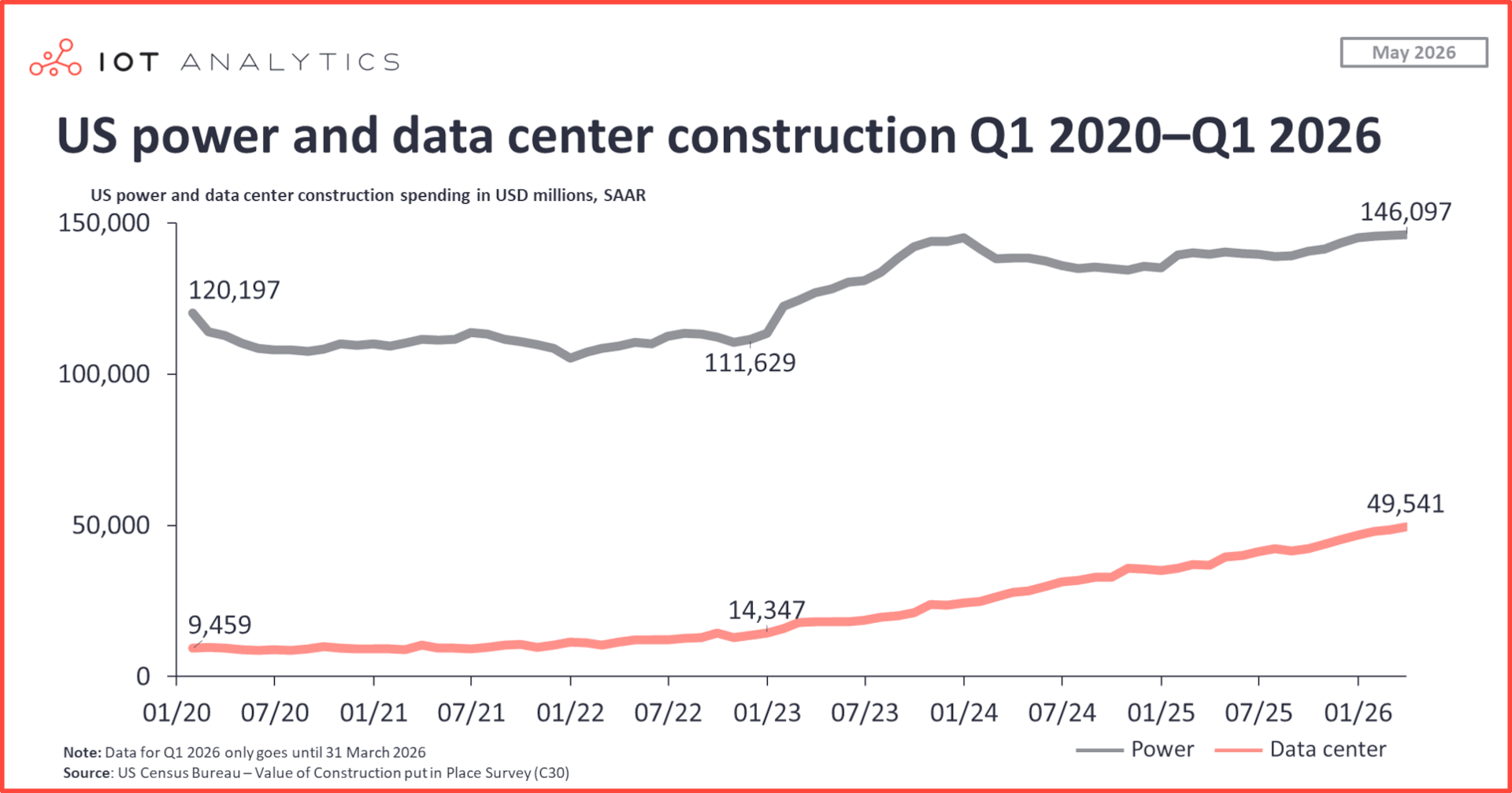

Data center facility spending grows 5x. Data center construction has grown from approximately $9.5 billion annualized in January 2020 to $47 billion annualized in January 2026, with a new all-time high in the January 2026 VIP survey results. YoY growth has stayed above 30% for 4 consecutive years and registered +31% in early 2026, even off a much larger base. Driving this growth is the AI boom, which started before the current US administration and the tariffs.

Hyperscaler CapEx drives AI/data center infrastructure. US-based hyperscalers Amazon, Microsoft, Google, and Meta collectively spent over $410 billion on CapEx in 2025, up from $200 billion in 2024, with each company’s spending reaching all-time highs.

The next construction boom: Power infrastructure

Grid constraints are driving a utility CapEx surge. Data center growth is increasingly running into a constraint: the grid. The construction data shows power infrastructure spending was largely flat from 2020 to 2022, up in 2023, and plateaued in 2024. However, the YoY growth rate has been quietly accelerating through 2025, from ~1% in early 2025 to roughly 6% by year-end.

Forward-looking utility CapEx commitments suggest a much larger cycle is coming. S&P Global‘s Regulatory Research Associates forecasts roughly $1.3 trillion in aggregate US energy utility CapEx between 2026 and 2030—a record, driven primarily by data center demand. According to Utility Dive, global credit rating agency Morningstar DBRS expects a 5-year utility CapEx super-cycle, with $1.4 trillion in electricity infrastructure investment projected for 2025 to 2030, double that of the prior decade. Here, US policy is actually a significant driver: the One Big Beautiful Bill Act, for example, mandates 30 offshore lease sales over the coming years along the southern US coast. The first lease sale was held on December 10, 2025, generating over $300 million in high bids.

Further analysis

While there is no “reshoring boom,” US manufacturing has experienced a cyclical uptick, according to analysis in the Industrial Macro Pulse – May 2026 report. The global manufacturing PMI, cited in the aforementioned White House report and discussed in the IoT Analytics report, shows a strong sector in the US, but if this were the start of a larger boom, the data does not show that yet.

Below in our Insights+ section, we share some of these positive health signs for the US manufacturing sector, including US manufacturing orders data and an update on industrial automation lead times.

Access key market data for $99/month per user

The Insights+ Subscription unlocks exclusive facts & figures. You will gain access to:

- Additional analyses derived directly from our reports, databases, and trackers

- An extended version of each research article not available to the public

Full report access not included. For enterprise offerings, please contact sales: sales@iot-analytics.com