In short

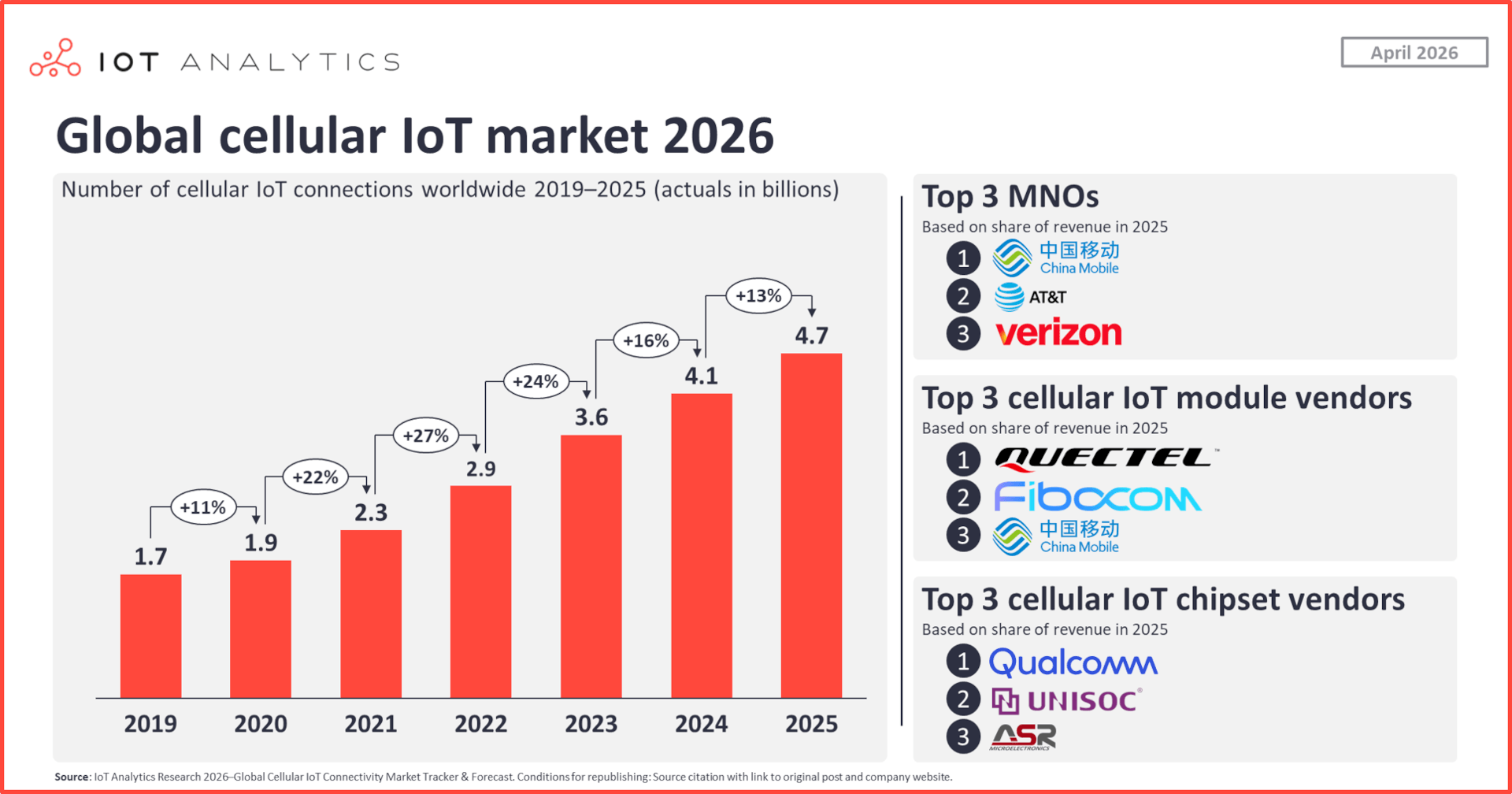

- Cellular IoT connections grew 13.3% in 2025 (the lowest growth rate since 2020), reaching 4.7 billion, according to IoT Analytics’ ongoing tracking and forecasting of global cellular IoT connectivity and cellular IoT modules and chipsets.

- NB-IoT was the leading cellular IoT technology in 2025, followed by LTE-Cat 1 bis and 4G.

- Chinese and US companies continue to dominate the market, but Chinese growth has slowed: China Mobile remained the leading cellular IoT operator globally, with 17% of global cellular IoT connectivity revenue; Quectel remained the leading shipper of cellular IoT modules; Qualcomm remained the leading supplier of cellular IoT chipsets.

Why it matters

- Demand for cellular IoT modules and chipsets continues to grow. Cellular network operators, device, module & chipset manufacturers, and component players should study market projections and how peers are adapting amid geopolitical tensions, new regulations, and market shakeups.

In this article

- Connected IoT device market update – Spring 2026

- Leading cellular IoT technologies in 2025

- Top 5 cellular IoT operators by revenue share

- Top 5 cellular IoT module & chipset vendors by revenue share

- Cellular IoT market outlook

- Further analysis

- Top 5 cellular IoT module vendors in 2025 by shipments (Insights+)

- Top 5 cellular IoT chipset vendors in 2025 by shipments (Insights+)

Connected IoT device market update – Spring 2026

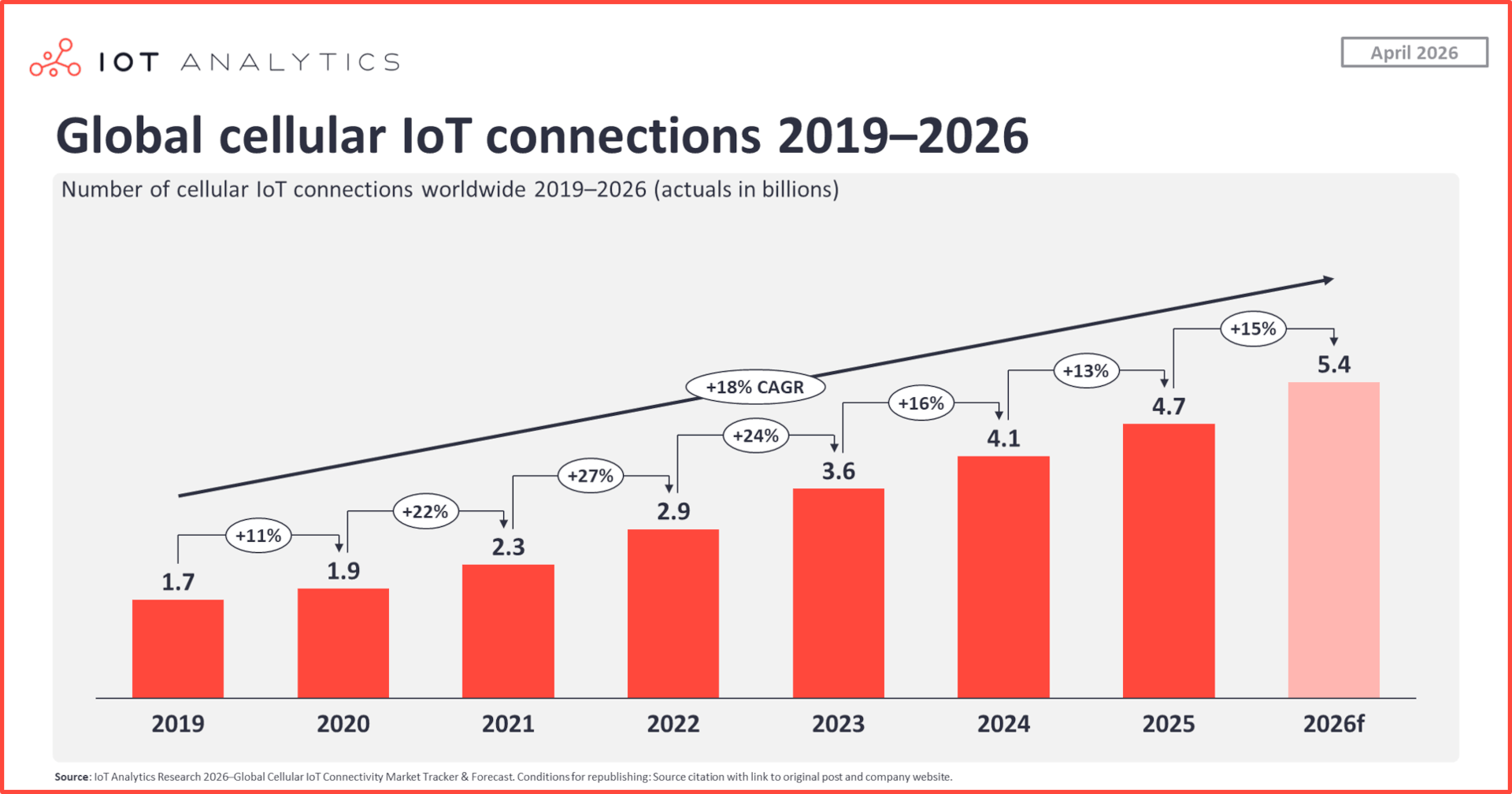

Cellular IoT connections grew 13.3% in 2025; expected to surpass 9 billion by 2030. The number of cellular IoT connections reached 4.7 billion in 2025, representing 13.3% growth over 2024. This is the second-slowest year-over-year (YoY) growth since IoT Analytics began tracking the cellular IoT connectivity market in 2010 (2020 witnessed 11% YoY growth for cellular IoT connections). The slowdown in growth stems from China—previously a major cellular IoT growth engine—becoming a growth laggard in 2025.

The 4.7 billion cellular IoT connections make up approximately 22% of the 21.1 billion overall IoT connections in 2025. Looking ahead, IoT Analytics expects the number of cellular IoT connections to reach 5.4 billion in 2026 and to continue growing at a 14.3% CAGR through 2030, reaching 9.2 billion.

Insights from this article are derived from

Cellular IoT Module and Chipset Market Tracker & Forecast

An interactive dashboard and structured market tracker that includes quarterly data on worldwide cellular IoT modules and chipsets from 2018 to Q4 2025, including a quarterly and annual forecast from Q1 2026 to 2029.

Already a subscriber? View your trackers here →

Leading cellular IoT technologies in 2025

Based on updated cellular IoT module and chipset shipment data for 2025, the top 3 cellular IoT connectivity technologies by share of overall shipments were:

- NB-IoT – 33.5%

- LTE-Cat 1 bis – 21.4%

- 4G – 18.6%

While NB-IoT leads in volume, the landscape changes significantly when looking at revenue (market value), where higher-bandwidth technologies dominate:

- 5G

- 4G

- LTE-Cat 1 bis

Top 5 cellular IoT operators by revenue share

Mobile network operators (MNOs) worldwide generated $20.8 billion in revenue from the 4.7 billion cellular IoT connections in 2025. The top 5 MNOs by revenue, listed below, managed over 60% of all global cellular IoT connectivity revenue in 2025:

- China Mobile – 17% of global cellular IoT connectivity revenue

- AT&T – 12% of global cellular IoT connectivity revenue

- Verizon – 11% of global cellular IoT connectivity revenue

- China Unicom – 11% of global cellular IoT connectivity revenue

- Vodafone – 9% of global cellular IoT connectivity revenue

The top cellular IoT module & chipset vendors by revenue share

Top 5 cellular IoT module vendors by share of revenue in 2025:

- Quectel – 34%

- Fibocom – 14%

- China Mobile – 10%

- Meig – 7%

- Telit Cinterion – 5%

Top 5 cellular IoT chipset vendors by share of revenue in 2025:

- Qualcomm – 73%

- UNISOC – 10%

- ASR – 6%

- HiSilicon – 5%

- MediaTek – 3%

Cellular IoT market outlook

Cellular IoT is entering a two-track growth phase. NB-IoT and LTE Cat 1 bis are likely to keep driving connection and module shipment volumes, especially in cost-sensitive use cases such as metering, tracking, and basic monitoring. However, 5G, 5G RedCap, and eventually 5G eRedCap are likely to shape the premium revenue pool, as enterprises adopt higher-bandwidth, lower-latency, and more compute-capable cellular IoT devices.

IoT Analytics expects that the next growth wave will not come from connectivity alone. More cellular IoT endpoints are expected to require local processing, stronger security, and AI inference at the device level to reduce cloud dependency and improve responsiveness. This points to a hardware upgrade cycle across modules, chipsets, and connected devices. It also shifts value toward vendors that can combine cellular connectivity, edge computing, power efficiency, certification support, and regulatory compliance.

In 2026 and beyond, 3 themes are worth watching:

- Cat 1 bis replacing legacy 2G/3G and parts of traditional 4G IoT

- RedCap and eRedCap expanding the mid-tier between low-power IoT and full 5G

- Module/chipset competition intensifying as geopolitics, certification rules, and regional supply-chain preferences influence vendor selection

Further analysis

Below in our Insights+ section, we share the top cellular IoT module and chipset vendors by shipments in 2025. Those wanting to dive deeper into the cellular IoT connectivity market can use our structured Global Cellular IoT Connectivity Tracker & Forecast and our Global Cellular IoT Module and Chipset Market Tracker & Forecast.

Access key market data for $99/month per user

The Insights+ Subscription unlocks exclusive facts & figures. You will gain access to:

- Additional analyses derived directly from our reports, databases, and trackers

- An extended version of each research article not available to the public

Full report access not included. For enterprise offerings, please contact sales: sales@iot-analytics.com