Key Insights

- The IoT platforms market exceeded forecasts, growing 48% between 2015 and 2020 according to IoT Analytics 2021 market report on IoT Platforms.

- Many large multinationals have adopted IoT Platforms in recent years.

- Microsoft and AWS have emerged as frontrunners in the market.

- IoT platform architectures and business models have undergone large changes.

Why it matters?

- Smaller IoT platform vendors need to be aware of the actions of the cloud hyperscalers in order to avoid being crushed in direct competition.

- Companies looking to realize IoT use cases should seriously consider using an IoT platform as today’s leading platforms are stable, secure, and flexible enough to meet modern architectural and business requirements.

5 years ago, when we forecasted that the IoT platforms market would have a 5-year compound annual growth rate (CAGR) of 35%, we wondered if our growth projection was unrealistically high.

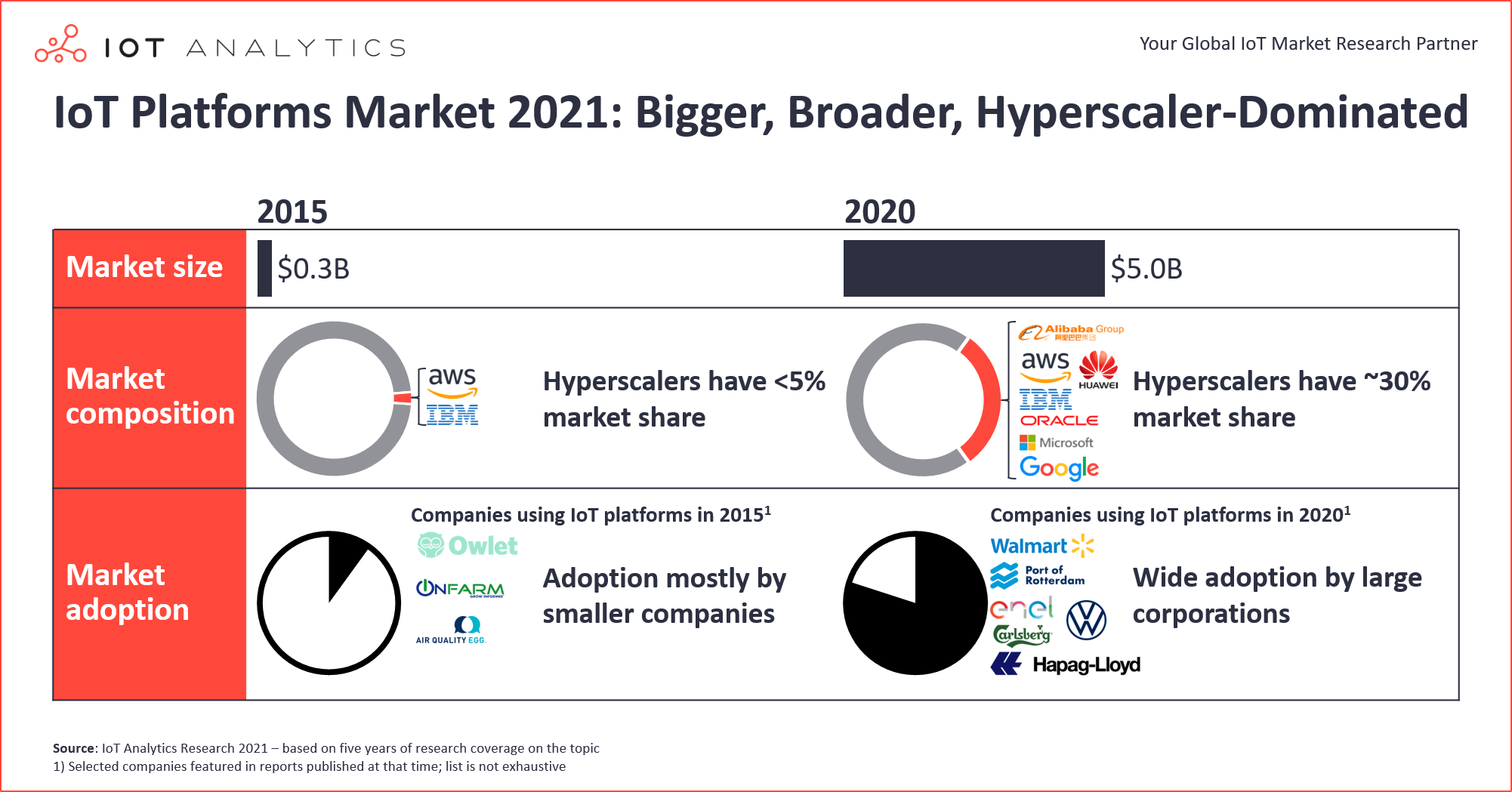

5 years later, it has become apparent that the forecast was actually too low. The IoT Platforms market between 2015 and 2020 grew to be $800 million larger than we forecasted back in early 2016, resulting in a staggering 48% CAGR.

Comparing what we “knew” back in 2016 to what we know today provides some clues as to why the market exceeded expectations so much. 5 years ago, no one really knew what an IoT platform was, let alone how big the market would be, which business models would work, how architectures would evolve, and which companies/industries would adopt them. The only thing that was “known” was that the IoT platforms market was a billion dollar “blue ocean” opportunity ready to be captured by innovative companies.

Today we have a bit more clarity on these topics, as the IoT platforms market has grown into a more mature (but still rapidly growing ) $5 billion market. Based on our latest IoT Platforms Market Report 2021-2026, this article looks at 5 things to know about the IoT platforms market today and compares these things to the 5 things to know about IoT platforms analysis we published in early 2016.

1. IoT Platform Definition: The Functionality of IoT Platforms has Expanded

“IoT platform” is still a relatively ambiguous phrase that means different things to different people (much like the term “edge computing”). Before answering the question “What is an IoT platform?” one needs to answer the question “What is a platform?”. A platform is a group of technologies that are used as a base upon which other applications, processes, services, or technologies are developed. Platforms can be hardware (e.g., chips, devices) or software. Types of software platforms include operating systems, development environments (e.g., Java, .NET), and digital platforms. Digital platforms are highly configurable/extensible software tools that sit above traditional development platforms. There are several types of digital platforms, including social (e.g., Facebook, LinkedIn), marketplace (e.g., Amazon, app stores), and IoT platforms. IoT Platform definition: An IoT platform is a type of digital platform that is used for building and managing IoT solutions.

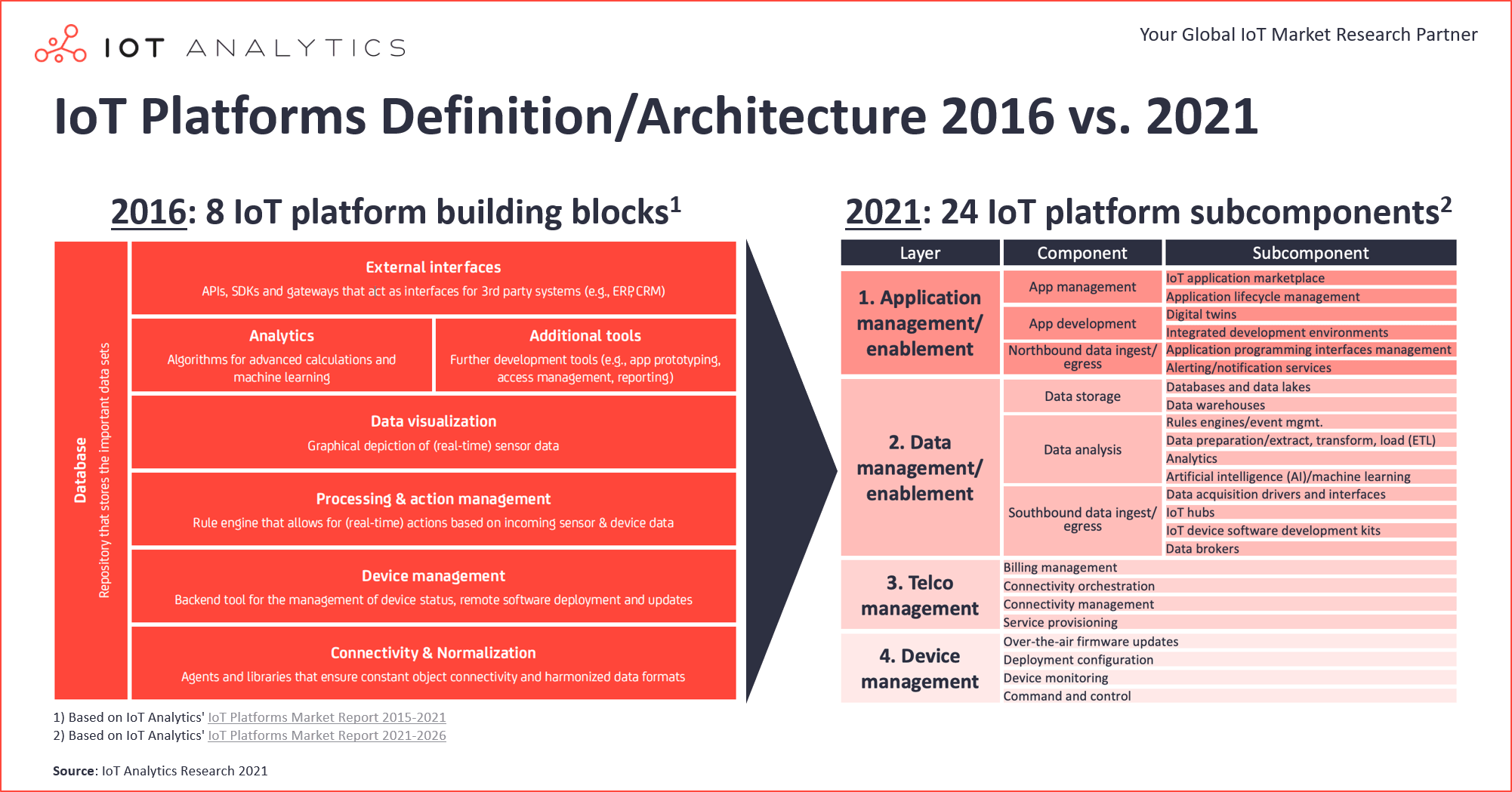

The functionality of IoT platforms (and subsequent definition) has evolved as the volume, variety, and velocity of data that IoT solutions deal with has increased over the past 5 years. IoT Analytics’ definition of an IoT platform has changed as the functionality of IoT platforms has expanded. The picture above compares how IoT Analytics defined 8 components of an IoT platform in 2016 with the IoT Platform definition today – grouped into 24 subcomponents. Many of today’s components are similar to those in the 2016 architecture, but modern IoT platforms have become more specialized (e.g., focusing on device management or telco management), more modular (e.g., via microservices), and more data-centric (by offering data management/enablement components) in nature. The 2021 definition better reflects the reality of today’s modern IoT platforms by segmenting them into four distinct layers, each of which can consist of several components and/or subcomponents. The four main layers are:

- Application management / enablement – providing the ability to rapidly develop, test, and seamlessly manage IoT applications

- Data management / enablement – providing the ability to ingest, store, and analyze data from IoT devices

- Telco management – providing telecommunications companies the ability to manage the connectivity to IoT devices at scale

- Device management – providing the ability to remotely configure, monitor, and manage IoT devices, including over-the-air updates

2. IoT Platforms Market: Growth Has Exceeded Expectations, Driven by Cloud Hyperscalers

Back in early 2016, IoT Analytics forecasted that the IoT platforms market would reach $1.3B by 2020. Our latest report sizes the market at $5.0B in 2020 – almost 4x bigger than we projected in our 2016 report. However, this is a bit of an apples and oranges comparison, as a large part of this underestimation can be explained by our expanded definition of an IoT platform (from just considering application enablement platforms to now considering 4 main platform types). Comparing only the application management/enablement portion of the IoT platforms report still yields a rather humbling (from a forecast accuracy perspective) result; the market is ~60% (or ~$0.8 billion) larger than we forecasted it would be back in 2016. In fact, the IoT platforms market grew at a staggering annual growth rate of 48% between 2015 and 2020, significantly higher than the 35% we forecasted.

A big portion of the growth in the IoT platforms market can be attributed to rapid revenue growth realized by the cloud hyperscalers (most notably Microsoft and AWS), who were just barely dipping their toes into IoT back in early 2016. In fact, AWS IoT Core became generally available in December 2015 and Microsoft’s Azure IoT Hub did not reach GA status until February 2016. Companies like PTC, Ayla Networks, General Electric, and Cisco entered the IoT platforms market earlier than the cloud providers, but eventually realized they needed to partner with (rather than compete with) the cloud hyperscalers in order to stay relevant. A big part of the cloud hyperscalers’ success is their massive investments in IoT which have yielded dozens of new value-creating products and services for IoT end users over the past 5 years. AWS started with one service called AWS IoT and now offers at least 8 IoT-related services including AWS IoT Greengrass, AWS IoT Device Defender, AWS IoT Device Management, and others. Despite hundreds of IoT platforms on the market, hyperscalers, according to our estimate, captured ~30% of the total IoT platforms market in 2020.

“In Q2 2019, we closed 35 deals together with Microsoft, roughly tripled the deal count of Q1 2019, and the active co-sell pipeline has grown to 240. While Microsoft was initially envisioned to be an important element of our smart connected products go-to-market strategy, we are beginning to close a number of deals in factory and AR use cases with them.”

Jim Heppelmann, CEO at PTC

3. IoT Platform Business Models: New Pricing Strategies and Revenue Streams Have Emerged

The entrance of the cloud hyperscaler giants into the market in early 2016 provided validation that the IoT platform market opportunity was real. The entrance (among other things) also led to the emergence of new pricing and revenue strategies for new and existing IoT platform vendors.

New pricing strategies

New pricing strategies/themes that have emerged include:

- More subscription pricing (e.g., PTC transitioned ThingWorx to 100% subscription in early 2019)

- More granular pricing (e.g., ThingLogix charges based on the number of Foundry events consumed)

- More complex pricing (e.g., AWS IoT Core was initially priced based on number of messages sent, now each service has a unique pricing scheme based on a variety of metrics such as “things registered”, “analytics compute units”, and others)

- More (but still rare) outcome-based pricing (e.g., Relayr’s “business outcome as a service” solutions)

New revenue streams – OEMs

Our 2016 article on IoT Platforms highlighted the fact that data that is collected by IoT platforms will lead to the creation of IoT services for connected businesses. Today, product companies (OEMs) are using IoT platforms to efficiently add IoT connectivity to their offerings and enable new connected software/service revenue streams alongside their equipment/products (see our IoT Commercialization & Business Model Report for more information).

New revenue streams – Vendors

Today’s IoT platform market provides revenue opportunities beyond traditional platform revenues, including:

- Applications. Both platform vendors themselves and 3rd parties are monetizing the applications built on top of IoT platforms (e.g., Siemens’ Closed-Loop Foundation application for MindSphere, Edge2Web’s Director application for MindSphere)

- Compute infrastructure. Cloud hyperscalers are realizing IaaS revenue by hosting other companies’ IoT platforms on their infrastructure (e.g., MachineMetrics on AWS, Uptake on Azure, Oden Technologies on Google Cloud).

- Services. Platform vendors themselves as well as third party systems integrators offer services related to designing, integrating, and operating IoT platforms (see our blog post on IoT system integration services for more info).

- Connectivity. Telco companies are bundling their own IoT platforms with connectivity services (e.g., Verizon’s network + ThingSpace) or integrating with existing IoT platforms to provide seamless connectivity (e.g., Eseye + AWS).

- End-to-end solutions. As the platform layer becomes less differentiated, companies are increasingly offering more vertical or use case specific solutions that include hardware and software and leverage some underlying IoT platform technology (e.g., ABB Ability solutions, AWS Monitron).

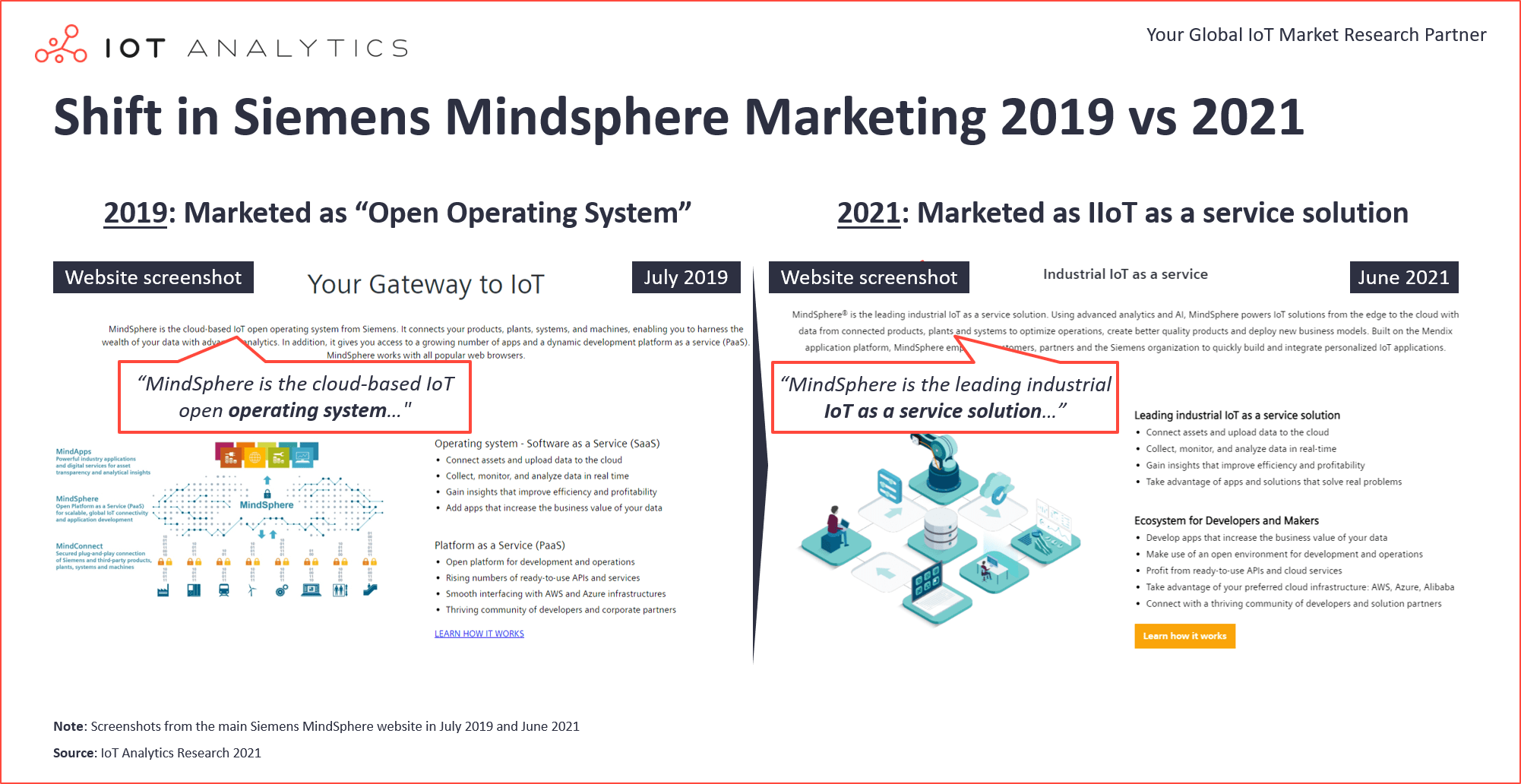

Cloud hyperscalers are capturing an increasing amount of platform revenue (via PaaS) as well as compute infrastructure revenue by providing IaaS for other platform providers moving their offerings to the cloud. Not wanting to compete with the hyperscalers, non-hyperscaler vendors are increasingly focusing on more vertical specific applications (e.g., GE Digital is now focusing on purpose-built applications as opposed to being a core platform player), services (e.g., Accenture seemingly stopped promoting its IoT platform), and solutions (e.g., Siemens’ shift of MindSphere to an “industrial IoT as a service” solution).

4. IoT Platform Adoption: Large Enterprises Have Made Their (Initial) IoT Platform Decisions

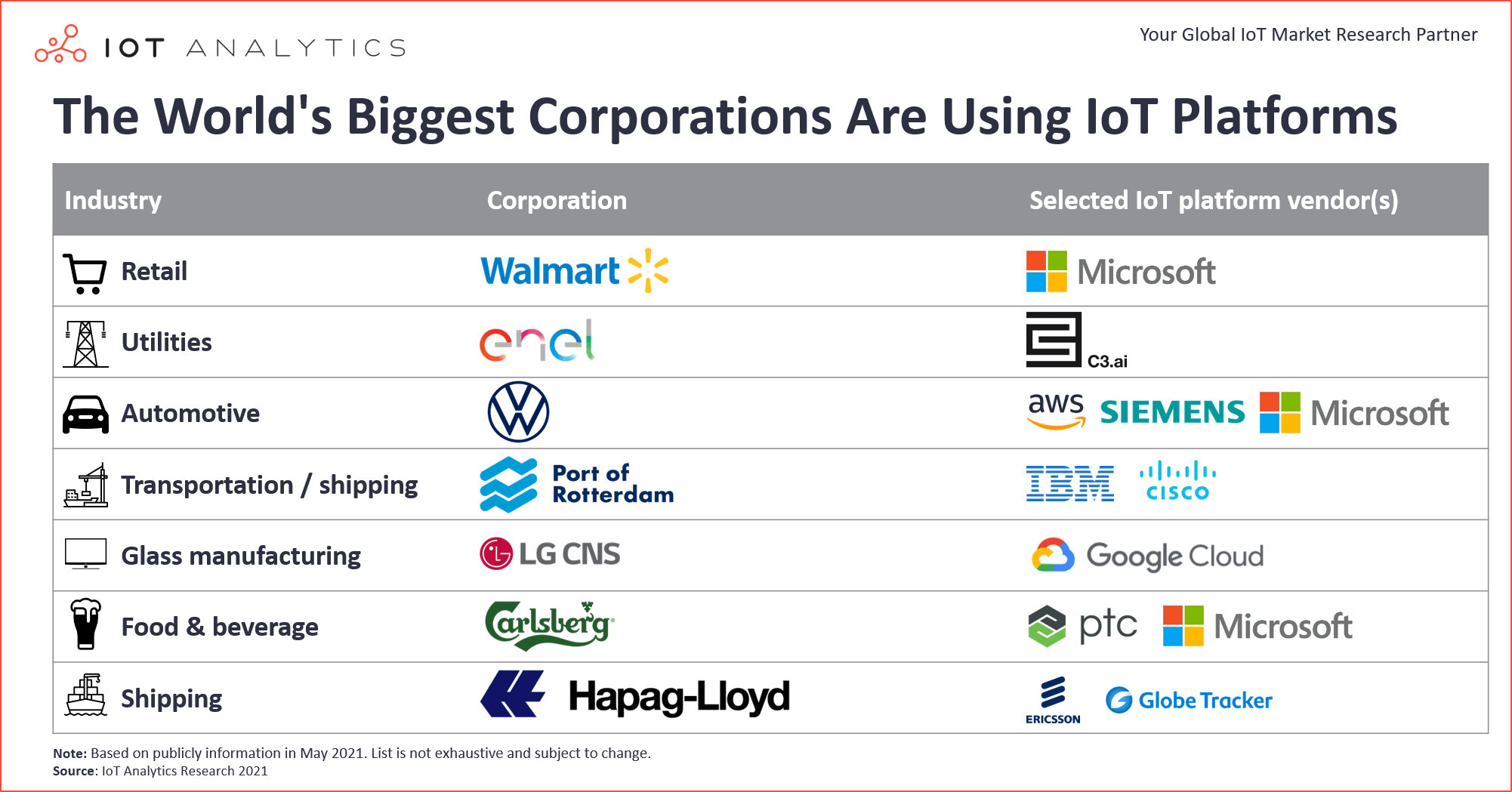

5 years ago, very few large companies had adopted IoT platforms and those that had were in the very early stages of their roll outs. Today, large, multinational corporations have gone through extensive decision-making processes and selected their platforms, and there are several deployments approaching 1 million endpoints. Companies like Walmart (Azure), Volkswagen (Siemens, AWS, and Azure), and Enel (C3.ai) have all made large investments in one or more IoT platforms that will eventually collect data from millions of IoT endpoints.

5. IoT Platform Architectures: Modernized, More Modular, And In The Cloud

Changes in end user preferences over the past 5 years have caused application and hosting architectures for IoT platforms to significantly evolve.

Application architectures for IoT platforms have evolved from monolithic to modular, leveraging modern technologies like containers and serverless computing. Several vendors who were relatively early entrants in the IoT platforms space (such as Braincube, MonoM, Jellix, and Siemens) have redesigned their platforms to leverage modern technologies, and start-up companies like ThingLogix have built platforms that are 100% serverless.

“Our platform architecture in 2016 was based on a core (monolithic) module that we continually added services to. If a customer only wanted a portion of the core module, we just gave them the whole thing – back then we did not think that was a problem. Over time we realized that every customer need and deployment is slightly different, and that is why we completely redesigned our platform to be based on containers. Today, containers are a must-have.”

Head of Industrial Solutions at IoT Platform Company

Hosting architectures for IoT platforms, over the last 5 years, have evolved from private on-premises being the most popular deployment type to public cloud being the most popular deployment type. Hybrid architectures (where some compute is on-premises and some is in the cloud) are quickly catching up to public cloud architectures as end users look to move some capabilities on-premises (e.g., data filtering, real-time decision making) while leaving others in the cloud. This move to the cloud is being led by end users who are investing in the cloud across their entire organization. IoT platform vendors with modern architectures are helping customers leverage their massive cloud investments by deploying the platforms within the customers’ own cloud environments instead of on the vendor’s cloud.

“5 years ago, 99% of our IoT platform instances were running on our own hosted servers. Today that number is closer to 80%, as large companies insist that the IoT platforms are hosted on their virtual private networks which have been established with the hyperscalers.”

CEO at Industrial IoT Platform Company

Conclusion and 5-Year Outlook

The way IoT platforms evolved over the past 5 years is truly transformational: Hyperscalers are now dominating the market, platforms are more modular, hosting preferences have shifted to the cloud, and end users are realizing value from IoT platforms at scale.

Despite the surprisingly high growth over the past 5 years, all signs point to strong continued growth (~30% CAGR) in the IoT platforms market for the next 5 years. Growth will be driven by both existing customers (that are expanding their IoT platform rollouts) and new customers (that will increasingly opt for IoT platforms instead of home-grown solutions). Hyperscalers (specifically AWS and Microsoft) are particularly well-positioned to maintain their market leadership and capture a good chunk of this growth.

While we cannot fully predict what the IoT platform market ecosystem will look like 5 years from now, we can say that it will be at least partially shaped by the way a few key questions are answered by the hyperscale vendors and everyone else in the ecosystem. For hyperscale vendors, the key questions include:

- “How supportive will we be of multi-cloud architectures?”

- “How much should we compete with our partners?”

The key questions for all other players in the ecosystem (e.g., non-hyperscale vendors, end users, service providers) include:

- “Which hyperscaler(s) should we partner with?”

- “How deeply should we integrate with them (e.g., IaaS or PaaS)?”

The correct answer to each of those questions will vary for every organization and be further complicated by uncertainty around other developing trends such as the adoption of multi-cloud setups and the emergence of IoT platform marketplaces.

Stay tuned to see how the IoT platform market evolves over the next 5 years.

More information and further reading

Are you interested in learning more about the IoT Platforms market?

The “IoT Platforms Market Report 2021-2026” is the 3rd major update of IoT Analytics’ ongoing coverage the IoT platforms market (IoT Platforms & Software workstream). The report includes updates on definitions of the different types of IoT platforms and components, market forecasts (by IoT platform type, hosting type, region, ISIC classification, and country), and market shares (by IoT platform type). Several new drivers, trends, and challenges are highlighted, and new deep dives on select topics are provided.

This report provides answers to the following questions (among others):

- How the IoT market has evolved since 2018

- How big the IoT platform market is and how fast it is growing across the following dimensions:

- By IoT platform vs. IoT IaaS

- By IoT platform type (4 types)

- By hosting type (4 types)

- By IoT segment (10 segments)

- By industry / ISIC code (41 codes)

- By country (57 countries)

- Which companies are leading the IoT Platforms market (by type, including market shares)

- How IoT Platforms solutions are being implemented today (list of 33 real enterprise IoT case studies with 6 detailed cases)

- Which types of IoT platform start-ups are being funded and by which investors (top 50, since 2018)

- Which notable IoT platforms have been acquired since June 2018

- 4 adoption drivers, 12 trends, and 5 overall challenges associated with IoT platforms

- 6 trends related to specific layers of IoT platforms

- How hyperscalers like Microsoft and Amazon are positioned in the IoT platform space

- How the interplay of the cloud and the edge is affecting IoT platform architectures and feature development

- How IoT platform vendors are using their own offerings to realize value internally

- Which IoT platforms are used by which automotive OEMs

And more …

Sample:

The sample of the report gives you a holistic overview of the available analysis (including the outline and key slides). The sample also provides additional context for the topic and describes the methodology of the analysis. You can download the sample here:

Are you interested in continued IoT coverage and updates?

Subscribe to our newsletter and follow us on LinkedIn and Twitter to stay up-to-date on the latest trends shaping the IoT markets. For complete enterprise IoT coverage with access to all of IoT Analytics’ paid content & reports including dedicated analyst time check out Enterprise subscription.