Key Insights

- The global market for cellular IoT modules declined 8% in 2020, according to IoT Analytics’ latest data.

- China is the only large country that showed growth in 2020.

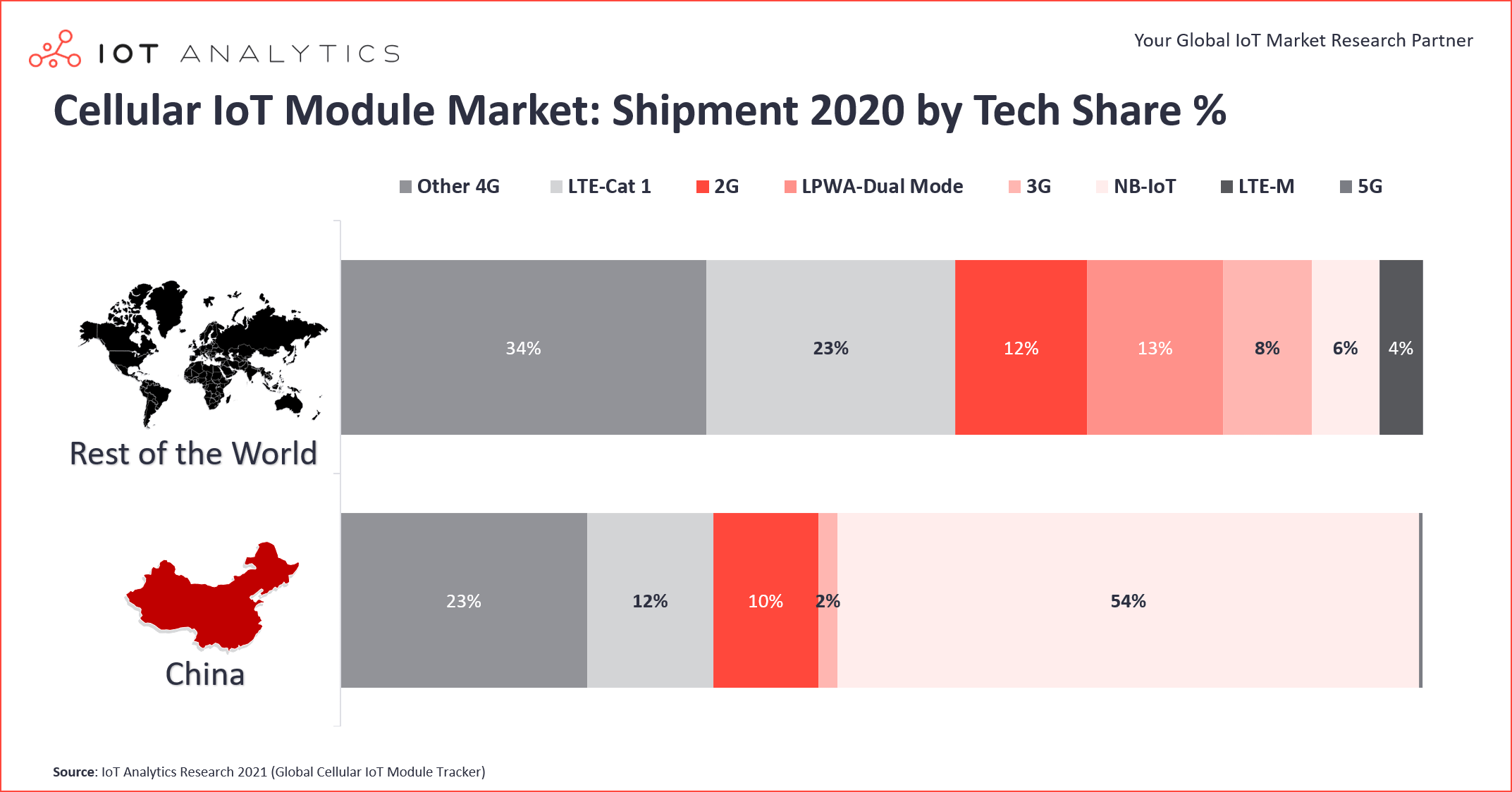

- LTE-Cat 1 technology, which contributes to 23% of cellular IoT modules outside of China and 12% in China, is seeing strong traction for IoT deployments.

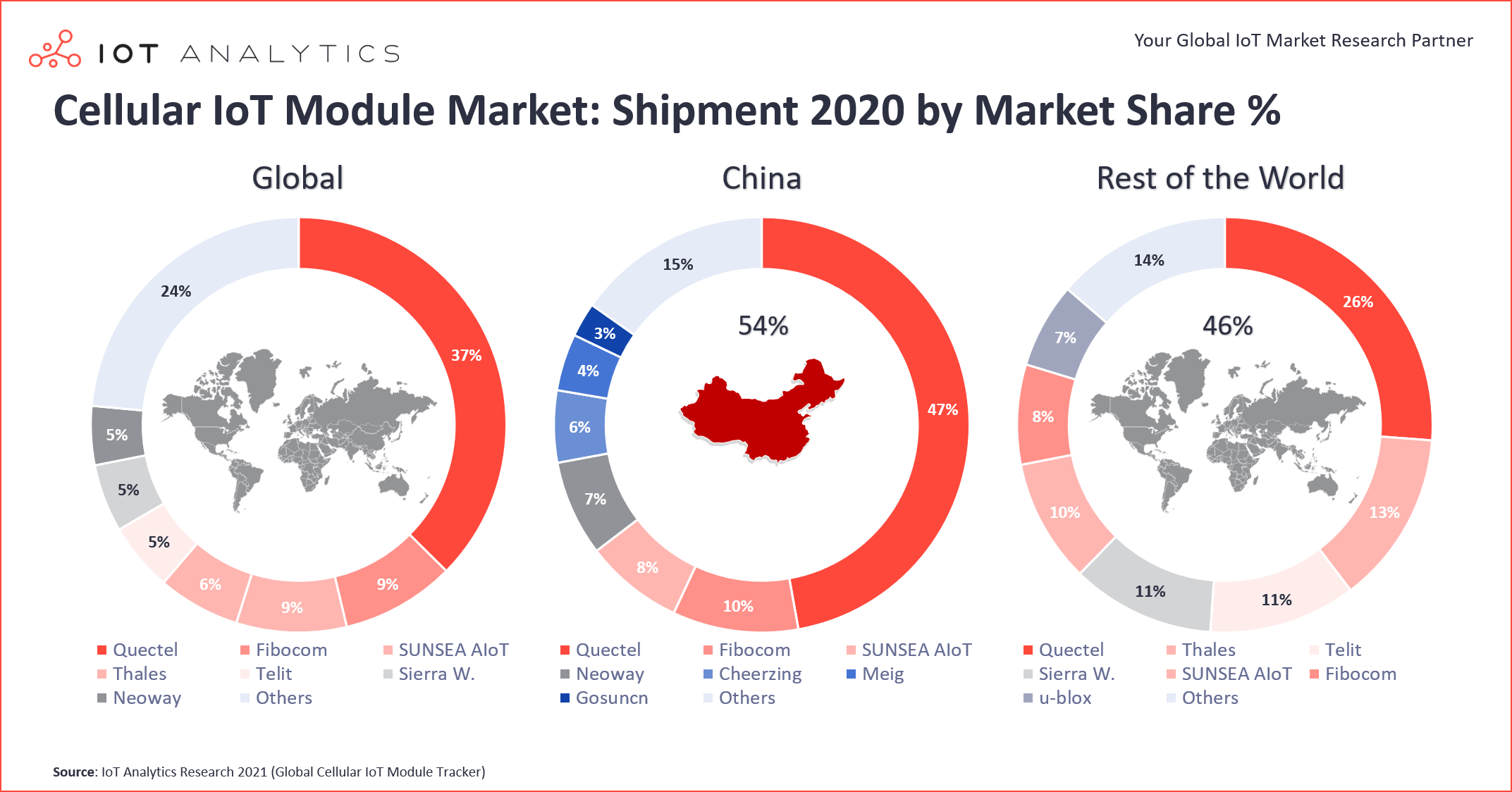

- Quectel expanded its market-leading position for total overall cellular IoT module shipment and revenue in 2020.

- The current global semiconductor shortage is expected to weigh heavily on 2021 growth.

The Cellular IoT Module Market: Overview

As part of IoT Analytics’ expanding market coverage of IoT markets, IoT Analytics this month launched an in-depth cellular IoT module market tracker that provides a quarterly look at the revenues and shipments of 33 companies providing cellular connectivity hardware modules for IoT deployments. With 4.5 billion cellular IoT connections expected by 2025, the market for cellular IoT modules is in a long-term cyclical uptrend (which was disrupted in 2020 by COVID-19). Every connected device that makes use of a cellular connection (e.g., 2G, 3G, 4G, or 5G) uses either a cellular IoT module or a cellular chipset embedded directly into the printed circuit board of a device or a piece of equipment. The promise of pre-configured IoT modules has become increasingly attractive in recent years, as customers are looking to decrease time-to-market for IoT solutions and multi-connectivity setups have made it more complicated for companies to develop their own solutions.

The data analysis performed by IoT Analytics shows that the global cellular IoT module market took a strong hit in 2020 due to COVID-19, with global revenues declining 8% year-over-year (YoY) to $3.1 billion. The situation was different in China. Cellular IoT module shipment in China grew 14% YoY in 2020, while cellular IoT module shipment in the rest of the world declined.

The reason the Chinese market expanded while other markets contracted is simple. Many IoT initiatives were halted or, in some cases, cancelled in 2020 due to COVID-19. IoT initiatives in China, however, were much less affected and continued as planned after a short COVID-19 lockdown.

Cellular IoT Module Market Technology Deep Dive: LTE-Cat 1 and LTE-Cat 1 bis

IoT Analytics segments the cellular IoT module market by connectivity technology, including two different subsegments of 4G: LTE-Cat 1 and other 4G.

One of the exciting trends that has emerged from the research is that the connectivity picture in China is quite different than in the rest of the world.

Outside of China, LTE-Cat 1 penetration is much stronger than, for example, narrowband (NB)-IoT penetration. LTE-Cat 1 makes up 23% of the market outside of China but only 12% in China. Cellular/licensed low-power wide-area (LPWA) shipments (NB-IoT and long-term evolution-machine type communication (LTE-M)) contributed to only 10% of the market outside of China in 2020. China is focused on NB-IoT; 90% of all NB-IoT shipments in 2020 originated there.

The rise of LTE-Cat 1 started in North America a few years ago. That is when LTE-Cat 1 started to become the go-to alternative for 2G and 3G IoT applications as 2G networks were retired by network operators. The massive migration from 2G/3G to LTE-Cat 1 started in 2018. Telit, Thales, and Sierra Wireless, for example, have collectively shipped more than 40 million LTE-Cat 1 modules in the last three years in the outside-China region. As evidenced in the data, the decline in shipments of 2G/3G modules was directly proportional to the increase in shipments of LTE-Cat 1 modules outside of China.

In recent years, NB-IoT has become the new alternative for 2G IoT applications in China. NB-IoT thus became the licenced LPWA technology of choice in China. However, the absence of LTE-M in China and technical limitations within NB-IoT have led to a rise in demand for a new segment: low-cost LTE-Cat 1 bis modules. Cat 1 bis, which is based on the 3rd Generation Partnership Project’s (3GPP) Release 13, is characterized by a single antenna and is optimized for low-power applications. This is in contrast to the LTE-Cat 1 standard adopted in North America, which is defined by 3GPP’s Release 8 and is supported by two receive (Rx) antennas. 3GPP’s Release 8 LTE-Cat 1 is based on Intel and Qualcomm chipsets, whereas 3GPP’s Release 13 LTE-Cat 1 bis is driven by UNISOC 8910DM.The Release 8 LTE-Cat 1 modules cost, on average, $10 more than the Release 13 LTE-Cat 1 modules.

Cellular IoT Module Vendor Landscape: Chinese suppliers continue to gain market share

In contrast to five years ago, the cellular IoT module market today is dominated by Chinese providers. Quectel, Fibocom, and SUNSEA AIoT have established themselves as market leaders, and the market expansion in China during 2020 has increased their market position (although 2020 growth rates among Chinese players are quite different).

Quectel’s revenue from cellular IoT modules grew 44% YoY in 2020 due to an increase in LTE-series and LPWA module shipments. In addition, a significant increase was reported in the company’s embedded automotive segment, which served more than 60 Tier I suppliers and more than 30 vehicle original equipment manufacturers (OEMs). Fibocom’s revenue from cellular IoT modules grew at a similar rate in 2020 due to increased LTE-Cat 1 bis and NB-IoT module shipments. In response to customer demand, Fibocom increased its IoT module production by 65% YoY in 2020.

Revenues declined for all European and North American providers in 2020. Thales’ decline was due to the adverse impact of COVID-19 on the automotive and point-of-sale sectors. Telit’s revenue decline was partially explained by the downturn in the deployment of smart meters for water and electricity in Asia-Pacific. Sierra Wireless’s revenue declined due to the divestiture of its automotive-embedded module product line to Rolling Wireless, a consortium led by Fibocom Wireless Inc., and lower sales of mobile computing and networking modules caused by the design losses of two higher-margin computing module customers. Tight component supply in late Q3 and Q4 2020 was also a factor.

Key cellular IoT module market trends to watch

A global chip shortage is affecting 2021 shipment volumes and profit margins.

According to IoT Analytics data, the global chip shortage had already affected some cellular module companies in Q4 2020. Most cellular module companies have a large backlog of orders in hand, and chip shortages have led to higher chip price volatility. Hence, in 1H 2021, we expect a global decline in shipment volume for the overall cellular IoT module market and a decrease in profit margins for module makers. The chip shortage is therefore hampering the COVID-19 cellular IoT recovery in Europe and North America. Markets there are not expected to grow as much as they could.

Many automotive IoT modules are changing to soft-subscriber identity modules (SIM).

The global automotive IoT cellular connectivity module market has undergone structural changes in recent years, as the market is now dominated by Chinese module players. In early 2019, Telit divested its automotive segment to TUS International’s Titan Automotive solution company. In 2020, Sierra Wireless sold its automotive division to Rolling Wireless, a consortium led by Fibocom Wireless Inc. Thales and uBlox remain as the only non-Chinese module players engaged in the automotive segment. Chinese module players depend on soft-SIM, while companies like Thales promote the advantages of a secure automotive module embedded within a secure element and a hardware-based eSIM.

Europe is adopting LTE-Cat 1 bis.

The Chinese adoption of LTE-Cat 1 bis is starting to also gain traction in Europe. Since the alternative, LTE-M, is still fragmented and is not available on a multi-country scale across all of Europe, LTE-Cat 1 bis is emerging as a viable alternative. LTE-Cat 1 in general comes with the benefit that it does not require software and hardware upgrades for the base station, so there are no additional network coverage costs.

More information and further reading

Are you interested in learning more about the cellular IoT module market?

The “Global Cellular IoT Module Tracker 2021” provides a holistic view and includes technological and regional deep dives into the global cellular IoT module market. It also contains detailed market sizing by region, technology, and 33 key companies. The tracker is based on publicly available information and IoT Analytics intelligence gathered from companies active in the market via telephone interviews and personal meetings at business events during the last three years.

This tracker provides answers to the following questions (among others):

- What is the global cellular IoT market size in terms of shipment and revenue?

- Who is the leading player globally and in each region?

- What is the growth of cellular LPWA?

- What are the trends for wholesale average selling price (ASP) by cellular connectivity technology and region?

- Which cellular connectivity technology is leading globally and in each region?

- How is LTE-Cat 1 performing in China and the rest of the world?

- Which regions are leading in terms of market growth and market share?

- Which companies are leading in terms of market growth and market share?

And more …

Sample:

The sample of the report gives you a holistic overview of the available analysis (including the outline and key slides). The sample also provides additional context for the topic and describes the methodology of the analysis. You can download the sample here:

Are you interested in continued IoT coverage and updates?

Subscribe to our newsletter and follow us on LinkedIn and Twitter to stay up-to-date on the latest trends shaping the IoT markets. For complete enterprise IoT coverage with access to all of IoT Analytics’ paid content & reports including dedicated analyst time check out Enterprise subscription.