In short

- The current state of telecommunications was on full display at MWC Barcelona 2026.

- The IoT Analytics team produced a 39-page MWC 2026 event report, covering 60+ companies, and presents its top 7 notable IoT and telecommunications networking trends here.

Why it matters

- MWC is one of the world’s most important telecommunications trade shows. The showcased technologies are widely applicable to IoT connectivity.

In this article

- MWC 2026

- 7 notable IoT and telco networking themes

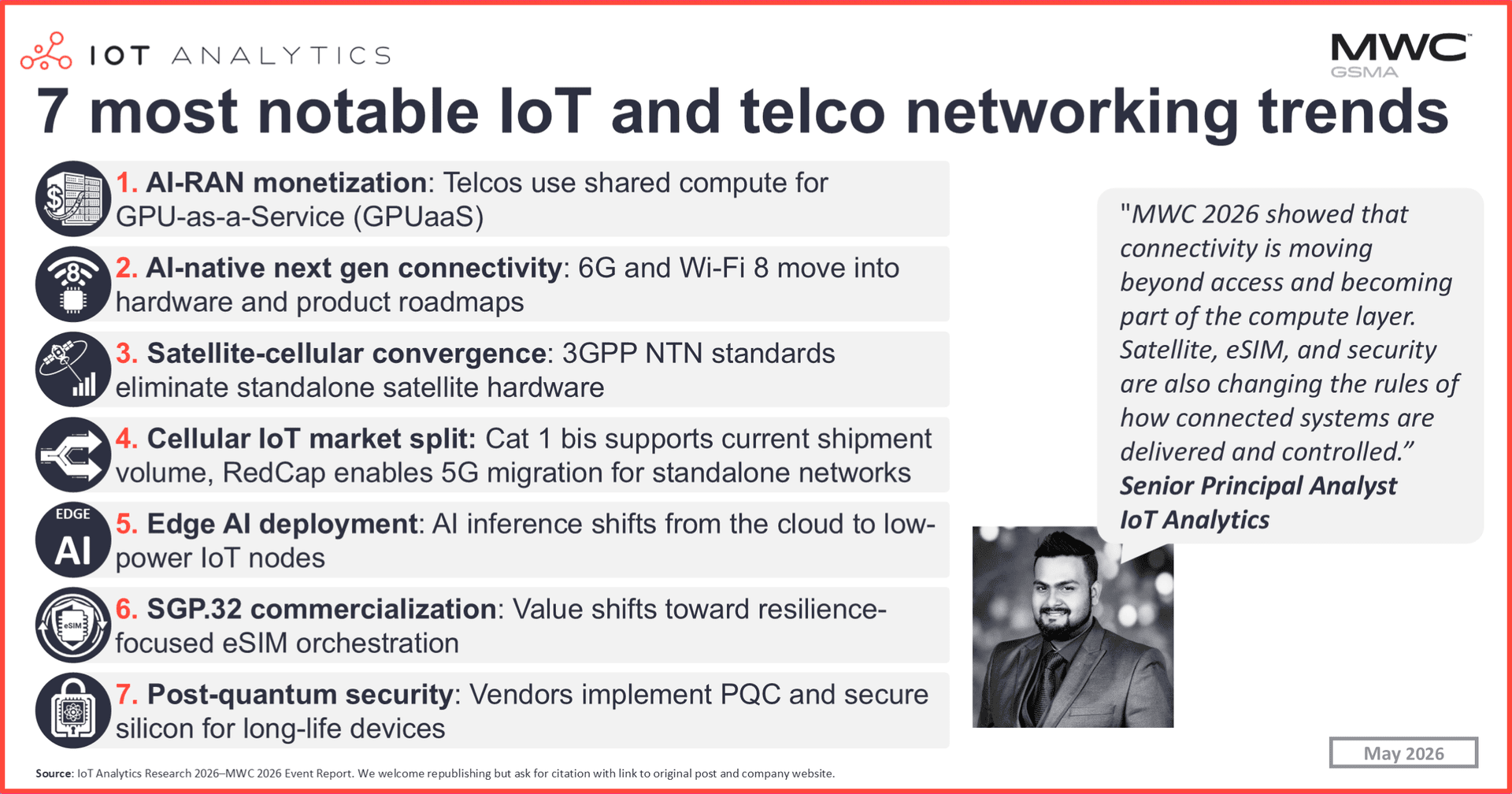

1. Telcos are using AI-RAN to explore shared compute infrastructure

2. Vendors are moving 6G and Wi-Fi 8 future talk into AI-native connectivity roadmaps

3. Mobile operators are integrating satellite and NTN technologies into cellular and IoT connectivity workflows

4. Module vendors are splitting cellular IoT into Cat 1 bis volume now and RedCap/eRedCap migration next

5. Vendors positioning edge AI at low-power IoT nodes

6. Companies are commercializing SGP.32, but value is shifting to eSIM orchestration

7. Vendors are moving IoT security toward post-quantum readiness and secure silicon - Analyst takeaway

- Further analysis

- Key highlights from leading IoT and telco networking companies (Insights+ Exclusive)

MWC 2026

Mobile World Congress (MWC) Barcelona 2026 took place March 2–5, 2026, celebrating its 20th year. As the telecommunication industry’s main event showcasing the latest technologies and solutions, vendors and telecommunications companies (telcos) showcased the latest in network infrastructure, cellular IoT, satellite IoT, eSIM standards and technology, and security.

MWC 2026 had nearly 105,000 visitors (approximately 4% less than in 2025) from over 200 countries, along with 2,900 exhibitors, sponsors, and partners, on par with 2025.

“It just so happens that next week, we celebrate 150 years since Alexander Graham Bell made the first phone call, the first step on a path that would lead us to where we are today. 115 years later, the first GSM call was here in Europe, built on what became a truly global standard that would unlock global scale and global innovation. And this year, we celebrate 20 years of MWC in wonderful Barcelona.”

Vivek Badrinath, Director General, GMSA

IoT Analytics Senior Principal Analyst Satyajit Sinha was on the ground during the event’s 4 days. He visited over 50+ booths and conducted over 30+ in-person interviews to understand the most recent developments in several focus areas:

- AI-RAN

- Cellular IoT

- Edge AI

- eSIM and SGP.32

- Private 5G

- Satellite IoT and non-terrestrial networks

- IoT security

- Post-quantum security

IoT Analytics’ research clients can refer to the full 39-page MWC 2026 event report to read more about the latest technologies, trends, announcements, and insightful quotes from key telecom industry players. Below, we share 7 of the most notable IoT and telecom networking trends.

Insights from this article are derived from the

MWC 2026 Event Report

A 39-page report presenting the key highlights, trends, and in-depth insights from the Telco communities assembled by the IoT Analytics analyst team at MWC 2026.

7 notable IoT and telco networking themes

1. Telcos are using AI-RAN to explore shared compute infrastructure

Telcos recasting AI-RAN as monetizable shared compute. Telcos brought AI-RAN into MWC 2026 as a shared compute and monetization story, not just a radio optimization upgrade as seen previously. GPU-based architectures are allowing operators to dynamically allocate compute capacity between RAN workloads and AI applications. The business logic behind this shift is that telcos can offer GPU-as-a-Service (GPUaaS) and AI inference on demand, selling whatever GPU capacity is not consumed by RAN operations on the open market.

For example, Japan-based information and communication technology company Fujitsu framed AI-RAN as a shared GPU model: operators can monetize unused compute through GPUaaS or run AI services on top of the same infrastructure.

US-based network infrastructure company Cisco extended the framing further, positioning telcos as future token-generation infrastructure providers. Finland-based telecommunications infrastructure company Nokia, US-based mobile network operator T-Mobile, and Indonesia-based telecommunications company Indosat demonstrated live AI-RAN with concurrent RAN and AI processing, showing that shared GPU-based AI-RAN is moving beyond architectural concepts into operator-facing deployments.

Architecture is diverging in the process. During his MWC 2026 keynote, US-based semiconductor company Qualcomm’s president and CEO, Cristiano Amon, explicitly rejected a one-size-fits-all AI-RAN model at MWC 2026, stating that RAN workloads are better suited to CPUs while AI inference workloads are better suited to accelerators.

“We also see a separation between RAN workloads, which we think are better suited on CPUs, and AI inference workloads, which we think are better suited on accelerators. We do not subscribe to a one-size-fits-all approach.”

Cristiano Amon, President & CEO, Qualcomm (source)

Meanwhile, Fujitsu‘s 1FINITY platform and Taiwan-based high-performance computing solutions company MSI‘s AI-vRAN on US-based semiconductor company NVIDIA’s MGX architecture both demonstrated shared infrastructure that separates and dynamically reallocates RAN and AI compute across DPU, CPU, and GPU resources.

2. Vendors are moving 6G and Wi-Fi 8 future talk into AI-native connectivity roadmaps

Vendors moving 6G and Wi-Fi 8 toward commercialization. At MWC 2026, vendors demonstrated how 6G and Wi-Fi 8 are moving from whitepaper positioning into hardware and coalition activity. Qualcomm framed 6G as a distributed AI computing infrastructure, projecting that 6G networks will embed AI compute at every step (including base stations and edge data centers), positioning traditional telecom infrastructure as AI data center networks. NVIDIA announced a coalition with major telecom and technology partners to build 6G on open, secure, AI-native platforms.

On the Wi-Fi side, Qualcomm launched the FastConnect 8800, its AI-native Wi-Fi 8 portfolio featuring 4×4 Wi-Fi and multi-gigabit performance with AI-driven optimization. China-based telecommunication technology company ZTE introduced fixed wireless access (FWA) products combining 5G-Advanced, Wi-Fi 8, AI optimization, and multi-gigabit throughput.

China-based wireless communication module company Fibocom and Taiwan-based semiconductor company MediaTek unveiled a customer premises equipment reference design combining 5G and Wi-Fi 8 chipsets. These hardware launches indicate that Wi-Fi 8 is now entering product roadmaps, not just standards bodies.

Nokia and US-based hyperscaler Google Cloud also extended the Network as Code ecosystem to support agentic AI use cases, enabling enterprise AI agents to interact directly with telecom network capabilities. This is a step toward the programmable network layer that 6G architects envision.

3. Mobile operators are integrating satellite and NTN technologies into cellular and IoT connectivity workflows

Satellite IoT is no longer a proprietary, stand-alone hardware category. 3GPP NTN standardization is pulling satellite capability directly into mainstream cellular modules, SIMs, and operator workflows, eliminating the need for separate satellite hardware alongside standard cellular components.

US-based satellite communications provider SpaceX anchored this theme at MWC 2026. SpaceX President and COO Gwynne Shotwell and SVP for Starlink Michael Nicolls detailed the second-generation Starlink constellation, which will deploy the 3GPP 5G NR-NTN standard for satellite-to-user links, targeting download speeds up to 150 Mbps. The system plans to use globally harmonized S-band spectrum, with launch targeted for mid-2027. Starlink’s direct-to-cell capability already proved operational during the Los Angeles wildfires, delivering over 250,000 SMS messages and more than 150 wireless emergency alerts.

“We’ll also be utilizing the 3GPP NR-NTN standard, which is specifically designed for the satellite-to-user links… receive download speeds of up to 150 megabits per second.”

Michael Nicolls, SVP of Starlink, SpaceX (source)

Broader market pattern reinforcing the SpaceX keynote. Germany-based telecommunications company Deutsche Telekom and SpaceX’s Starlink announced plans to bring satellite-to-mobile connectivity to Europe. UK-based telecommunications company Vodafone launched Satellite Connect Europe with US-based space-based cellular communications company AST SpaceMobile, partnering with France-based telecommunications company Orange, Spain-based telecommunications company Telefónica, and the multinational telecommunications operator 3 Group. Deutsche Telekom separately launched a multi-orbit IoT roaming service combining terrestrial NB-IoT with GEO and LEO satellite coverage.

On the device side, fabless wireless communications chip company Nordic Semiconductor launched the nRF9151 with 3GPP-compliant GEO and LEO NTN support alongside its standard LTE-M/NB-IoT capabilities. US-based satellite services provider Viasat positioned 3GPP NTN as a way to simplify automotive satellite adoption by fitting into the existing cellular architecture: one SIM, one device, one antenna. US-based satellite telecommunications company Iridium presented NTN Direct as a standards-based commercial NTN service launching in the second half of 2026.

4. Module vendors are splitting cellular IoT into Cat 1 bis volume now and RedCap/eRedCap migration next

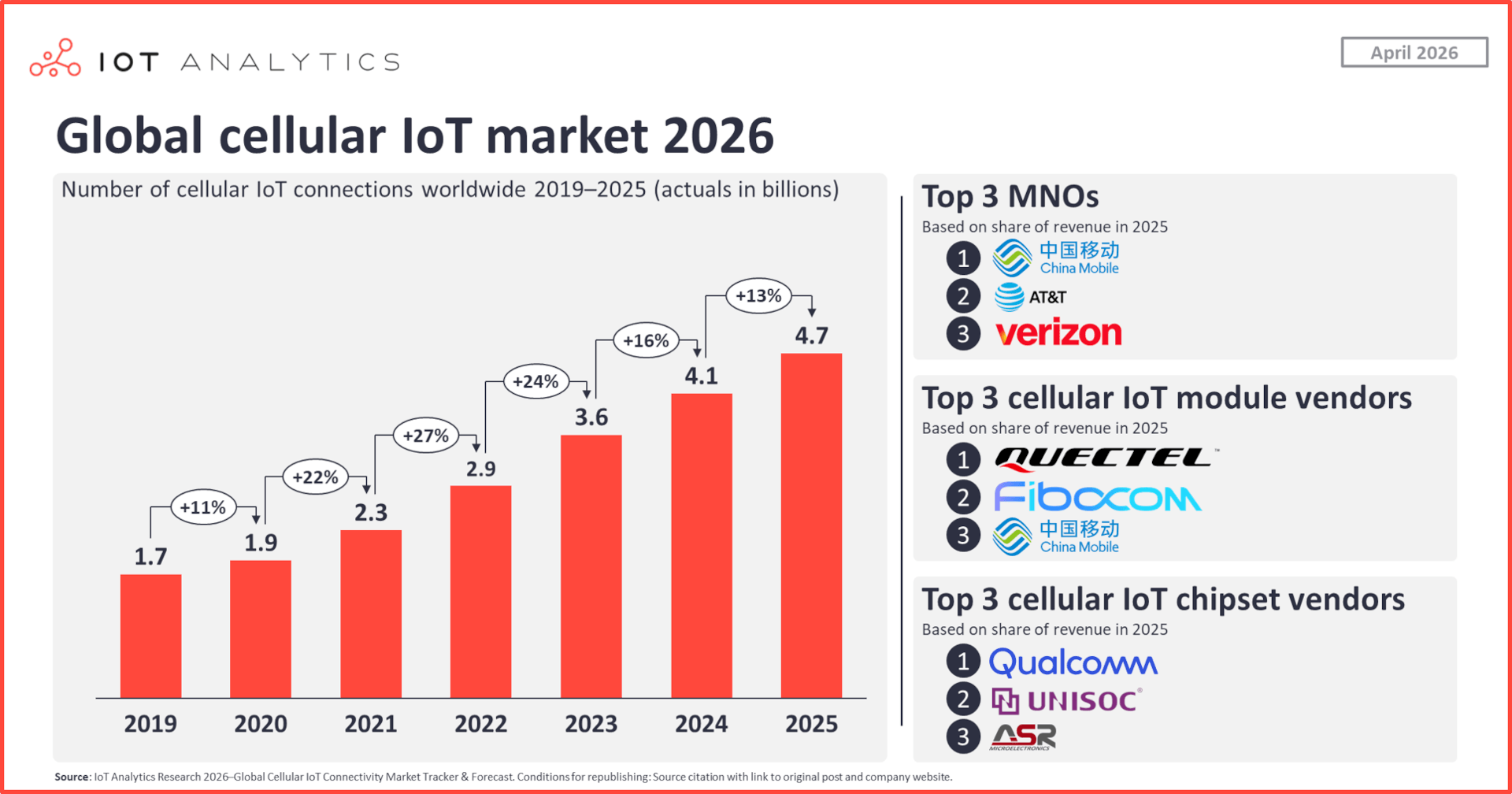

According to the latest update of the IoT cellular connectivity tracker and the IoT chipset & module tracker, there were 4.7 billion cellular IoT connections at the end of 2025, with China Mobile the top operator, Quectel the top module maker, and Qualcomm the top chipset vendor. But the market is shifting going forward.

Cellular IoT following split upgrade paths. Rather than moving through a clean generational upgrade, the cellular IoT market is splitting by deployment reality, with Cat 1 bis winning near-term volume and RedCap and eRedCap defining the 5G migration path for those markets ready for it.

Cat 1 bis anchoring near-term IoT demand. Cat 1 bis has emerged as a dominant commercial choice for global IoT deployments, growing strongly in China and Europe and beginning to compete with LTE-M and NB-IoT in utility use cases. The technology aligns with current buyer requirements: global coverage, mature module availability, acceptable cost, and long device lifecycles, particularly in regions where 5G SA is not yet widespread. Nordic Semiconductor‘s launch of the nRF93M1 Cat 1 bis module at MWC 2026 confirmed that Cat 1 bis remains important enough to anchor new product development, not just support installed base continuity.

RedCap commercialization advancing ahead of eRedCap migration. RedCap is entering commercial reality in markets with mature 5G SA deployments, primarily China, the US, and some private 5G environments. China-based IoT connectivity modules company Quectel highlighted its RM255C-GL 5G RedCap module for mid-tier IoT applications requiring more capability than LPWA but not full 5G eMBB. France-based fabless semiconductor company Sequans showcased its third-generation migration platform, with Monarch 3 providing a migration path from LTE-M/NB-IoT and Calliope 3 targeting Cat 1 bis migration toward 5G NR eRedCap.

eRedCap is being positioned further out as the next-generation low-power alternative, lower-cost and lower-power than RedCap. Nordic Semiconductor‘s roadmap includes a formal path to eRedCap, with sampling expected in late 2027 or early 2028.

LoRaWAN continuing growth as licensed LPWAN matures. LTE-M and NB-IoT are transitioning from growth to maturity globally, with multiple vendors confirming that connection growth has flattened. In contrast to these, discussions at MWC with LoRaWAN ecosystem players suggest that LoRaWAN, the main unlicensed LPWAN alternative to LTE-M and NB-IoT, has not reached the same plateau.

5. Vendors positioning edge AI at low-power IoT nodes

Vendors pushing AI inference into connected devices. Vendors are moving AI inference from gateways, cloud platforms, and high-end edge servers into the devices themselves. The shift is being driven by tighter power budgets, higher connectivity costs in remote deployments, and the need to avoid sending raw sensor data over cellular or LPWA links. Rather than treating inference as a cloud function, vendors are embedding lightweight AI models directly into devices powered by LPWA and cellular IoT connectivity.

Hong Kong-based full-stack IoT solutions company SG Wireless demonstrated this at MWC 2026 with the F1 TinyML over LTE-M solution for local person detection. The device performs inference locally and sends only metadata (not raw video) over the LTE-M link. No cloud connection is needed for the inference step itself.

Nordic Semiconductor‘s nRF92 combines NTN support with an Axon NPU for on-device edge AI, integrating inference capability directly into the cellular module. Nordic’s edge AI demo linked on-device inference to lower power use and reduced data traffic, making AI relevant to LPWA and cellular IoT rather than only to high-bandwidth 5G use cases.

US-based semiconductor and IoT systems company Semtech‘s approach keeps intelligence in the end device or partner MCU, using LoRa for connectivity and signal optimization. This is a partner-led device architecture that extends edge AI to LoRa-connected sensor nodes.

6. Companies are commercializing SGP.32, but value is shifting to eSIM orchestration

Vendors bringing SGP.32 into commercial IoT deployment. SGP.32 crossed from standards work into commercial deployment at MWC 2026. Sweden-based managed IoT connectivity company Tele2 IoT, France-based secure payments and telecommunications company IDEMIA Secure Transactions, and Cisco launched the first commercial end-to-end SGP.32 IoT solution in March 2026, combining Tele2 IoT connectivity, IDEMIA’s certified SGP.32 stack, and Cisco networking. IDEMIA disclosed more than 15 commercial deployments and 40 proofs of concept. Telit Cinterion, Emnify, and Soracom all showed live demos, pre-order programs, or customer testing activity.

SGP.32 shifting value toward connectivity orchestration. What MWC 2026 made clear, however, is that SGP.32 on its own does not deliver fleet-level operational value. Vendors are building orchestration layers on top of the standard to determine when, why, and how profiles should be changed across devices, operators, and regions. France-based electrical systems company Thales positioned Adaptive Connect as an SGP.32-compliant orchestration stack covering manufacturing, logistics, and field operations. Cellular IoT network operator Transatel (part of Japan-based NTT) described a strategy shift from selling connectivity to selling services and business outcomes.

“We shift from selling connectivity to… selling a service and a business outcome… We can help you orchestrate the connectivity, and based on the network events that we gather, you can choose the right time when you push the updates.”

Transatel representative at MWC 2026

UK-based eSIM and iSIM security software company Kigen positioned its SGP.32 stack as part of the security and compliance workflow for long-life IoT devices and expanded SGP.32 adoption through several partners:

- floLIVE, based in the UK

- Stacuity, based in the UK

- Trasna, based in Ireland

- NuvoLinQ, based in Canada

- Soracom, based in Japan

SGP.32 serving as fallback rather than switching engine. Early adopters are treating SGP.32 primarily as resilience and fallback insurance rather than a day-to-day fleet-switching engine. Germany-based cloud-native cellular IoT connectivity provider emnify described the typical customer reaction as follows:

“The main customer reaction is: this sounds promising, but right now I want an insurance policy. With SGP.32, we can deploy a secondary profile that is ready to switch to if needed. Customers are willing to pay slightly more for that fallback capability.”

emnify representative at MWC 2026

Commercial switching costs, eIM ownership fees, APN configuration complexity, and contractual lock-in are all constraining frequent, large-scale profile switching.

7. Vendors are moving IoT security toward post-quantum readiness and secure silicon

Post-quantum cryptography (PQC) moving from standards discussions into practical deployment proposals at MWC 2026. Multiple vendors presented hardware- and firmware-based PQC solutions applicable to existing devices and network equipment without requiring full hardware replacement. The urgency is not hypothetical: IoT devices deployed today may remain in the field for 10 to 15 years, during which quantum-capable adversaries could break current asymmetric encryption via ‘harvest now, decrypt later’ attacks.

South Korea-based semiconductor and cybersecurity company ICTK introduced PQC physical unclonable function (PUF) security chips for USIM and eSIM, combining post-quantum algorithms with a hardware root of trust based on PUF technology. Thales is implementing hybrid PQC in eSIM-related security flows and pushing customers to prepare for harvest-now-decrypt-later risk. IoT security company Pairpoint and US-based edge AI and IoT solutions company Lantronix signed an MoU to deploy PQC protection for existing industrial IoT routers and gateways, framing PQC as something operators can adopt without replacing installed infrastructure. France-based embedded cybersecurity company Secure-IC showcased its Securyzr neo Core Platform, integrating post-quantum crypto, secure key management, anti-tampering, and firmware lifecycle functions into an embedded security architecture.

Vendors aligning security silicon with CRA readiness. Embedded security silicon is simultaneously being redesigned for EU Cyber Resilience Act (CRA) compliance, rather than treating CRA and PQC as sequential projects. Kigen linked its eSA-certified eSIMs and SGP.32-certified eIM to security patching, auditable remediation workflows, and CRA readiness across manufacturing and fleet provisioning. Thales showcased an IoT Security Manager as a modular compliance stack covering firmware updates, anomaly detection, and identity management.

Analyst takeaway

IoT Analytics Senior Principal Analyst Satyajit Sinha attended MWC 2026 and produced the MWC 2026 Event Report based on his numerous discussions and observations. Below are a few opinions on the trends mentioned above, categorized by network infrastructure, cellular/satellite IoT, eSIM, and security.

Network infrastructure

AI-RAN should not be viewed only as another RAN optimization cycle. The more important implication is that operators are looking for a revenue logic to justify the next infrastructure investment cycle. Shared GPU capacity, AI inferencing at the network edge, and GPU-as-a-Service give operators a potential bridge between their 5G spending and the capital required for 6G. The risk is that not every operator will have the demand density, enterprise relationships, or operational maturity to turn network AI infrastructure into a real business.

Cellular and satellite IoT

Cellular IoT is not moving through a clean generational upgrade from LTE-M and NB-IoT to RedCap. The market is split by deployment reality. Cat 1 bis is winning near-term volume because it fits current coverage, cost, and utility requirements. RedCap is more dependent on 5G SA availability and is therefore strongest in China, the US, and private 5G environments. The more interesting long-term change is that connectivity and compute are converging even in low-power devices. TinyML and node-level inference can reduce traffic, power consumption, and cloud dependency, making AI relevant to LPWA and cellular IoT rather than only to high-bandwidth 5G use cases.

The satellite IoT story is becoming more credible because 3GPP NTN brings it into the existing cellular ecosystem. That changes the market from proprietary satellite hardware toward standard modules, SIM workflows, and operator partnerships. However, the market still needs more discipline on coverage claims. Vendors should distinguish between theoretical global reach and reliable service availability, especially when constellations are still being expanded. For early adoption, SOS, personal tracking, fleet monitoring, and remote asset use cases look more credible than broad claims of universal IoT coverage.

eSIM

SGP.32 is important, but it should not be interpreted as a simple fleet-switching button. The standard creates a better technical route for profile changes, failover, and long-term provider flexibility. However, large-scale switching will still be limited by fees, contracts, APN changes, eIM ownership, and value-added service lock-in. The near-term value is therefore resilience and orchestration, not mass churn. 2026 looks like a year of commercialization and testing, while broader deployment is more likely to be built in 2027.

Security

Security was underrepresented at MWC 2026 relative to the risk profile of long-life IoT, automotive, and infrastructure deployments. The industry is still treating security as a supporting topic, even though connected devices being deployed today may remain in the field for 10 to 15 years. That makes PQC readiness, secure elements, eSIM security workflows, and hardware roots of trust urgent design issues rather than future roadmap items. The most important gap is that PQC is still not central enough in discussions of 6G and IoT infrastructure, despite the “harvest now, decrypt later” risk posed by asymmetric encryption.

Further analysis

Below, in our Insights+ section, we share 15 highlights from Qualcomm, Deutsche Telekom, Nokia, SpaceX, Vodafone, and Huawei, including select quotes from leaders of these companies.

Access key market data for $99/month per user

The Insights+ Subscription unlocks exclusive facts & figures. You will gain access to:

- Additional analyses derived directly from our reports, databases, and trackers

- An extended version of each research article not available to the public

Full report access not included. For enterprise offerings, please contact sales: sales@iot-analytics.com