In short

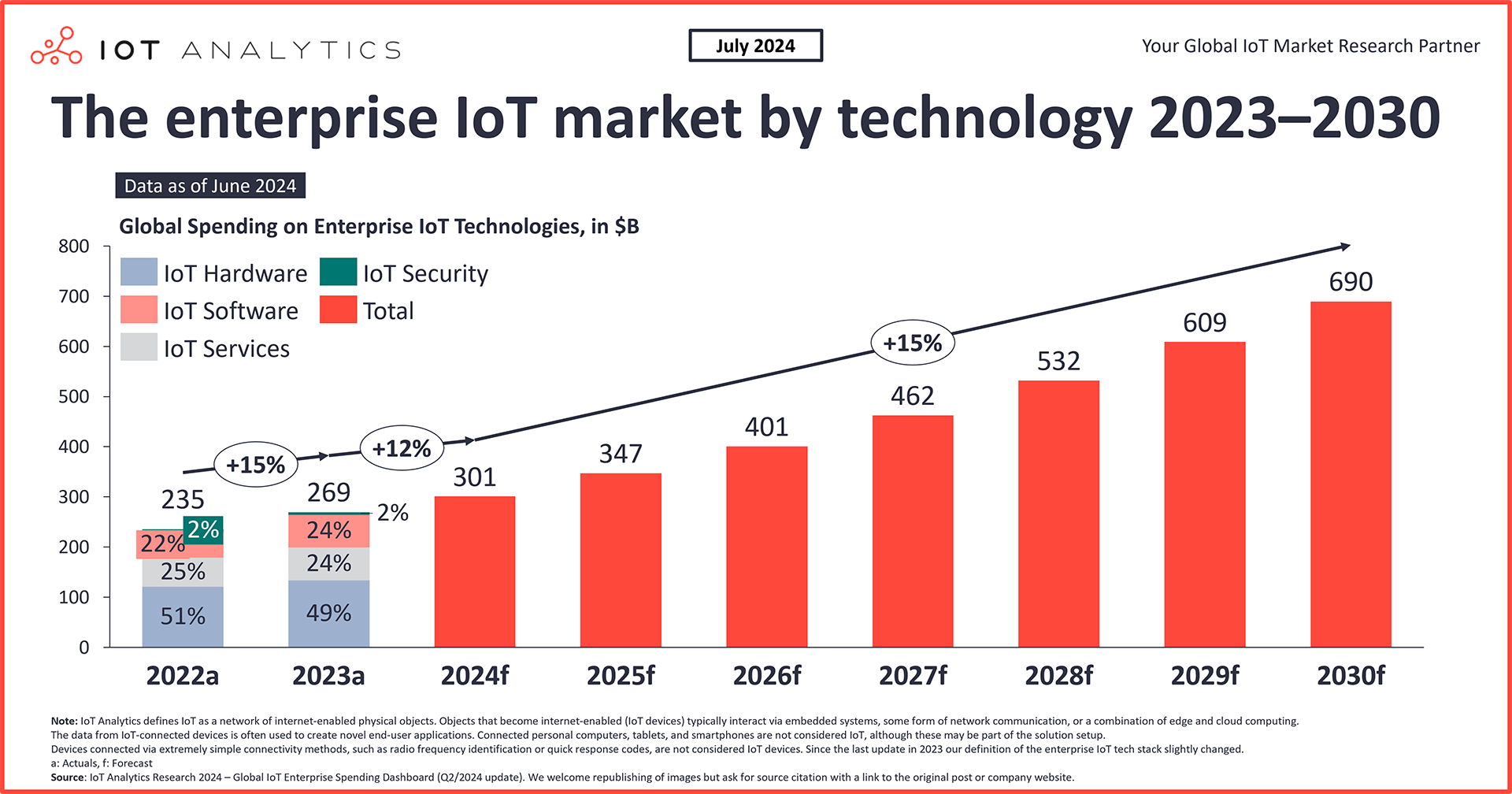

- The enterprise IoT market size reached $269 billion in 2023, representing 15% growth year-over-year, according to the Global IoT Enterprise Spending dashboard (Q2/2024 update). Growth is expected to slow further to 12% in 2024 before re-accelerating in 2025.

- Economic concerns have impacted corporate spending in general, including for IoT. IoT hardware technologies are currently hit the hardest.

- China, India, and the US are expected to lead in spending growth regionally, while automotive and process manufacturers are set to lead by vertical.

- Spending growth for enterprise IoT software is expected to greatly outpace that of enterprise IoT spending in general.

Why it matters?

- For enterprise IoT vendors: Market insights and forecasts can help vendors align their sales efforts with regional and industry trends and capitalize on future growth opportunities.

- For enterprises adopting IoT: Tracking market trends, drivers, and growth forecasts can help adopters make informed decisions about their IoT investments and strategies.

This article is based on insights from:

Global IoT Enterprise Spending (Q2/2024 Update)

- Experience a walk-through of the dashboard via screen share

- Get your specific questions addressed

- Explore how our research can add value to your organization

Already a subscriber? See your dashboard here →

Enterprise IoT market overview

Enterprise IoT market size grew 15% to $269 billion in 2023 year-over-year (YoY). This is lower than the 18% YoY growth in 2022, according to IoT Analytics’ Global IoT Enterprise Spending dashboard—which was updated in June 2024 and includes a look at enterprise IoT spending by region, vertical, and technology, along with a look at 100+ companies. For 2024, IoT Analytics expects growth to slow further to 12%, with the IoT market size expected to reach $301 billion.

Market recovery on the horizon. Enterprise IoT spending shows signs of growth rate recovery starting in 2025, with a CAGR of 15% projected until 2030.

Factors contributing to slower IoT market growth in 2024

Economic concerns weigh heavily on spending growth. Throughout 2023 and into 2024, economic concerns remained the top topic of CEOs during earnings calls. These concerns have generally led to reduced corporate spending, including for IoT.

Hardware spending is dragging the overall enterprise IoT spending growth rate down. Corporate curtailment of spending has hit IoT hardware the hardest. Out of the entire IoT tech stack—security, services, software, and hardware—hardware is likely to have the lowest growth rate in 2024 at 5%, according to the Global IoT Enterprise Spending dashboard. Specifically, the computers, controllers, and gateways segment is expected to experience a drop in actual enterprise IoT spending. One of the reasons is the high inventory levels that customers stockpiled in the last quarters.

Hardware companies express doubt about growth expectations in 2024. During individual interviews with over 300 exhibitors at Hannover Messe 2024, vendors with a heavy hardware footprint (e.g., large industrial automation suppliers) expressed caution when discussing their 2024 business outlooks—some citing customer inventory surplus and limited demand, which can lead to sales dips. Additionally, in May 2024, the CEOs of Siemens and Rockwell Automation—two leaders in this area—highlighted the muted industrial demands and high stock levels (particularly in China) during their Q2 earnings calls.

IoT market drivers in 2024 and beyond

IoT has a strong impact on the bottom line. According to IoT Analytics’ upcoming IoT Use Case Adoption Report 2024, enterprise IoT investments are overwhelmingly paying off—a finding likely to drive enterprise IoT market size growth in the coming years. Findings from the ongoing research show that the share of companies that report a positive ROI from IoT adoption has increased, and boardrooms are convinced about IoT’s positive impact.

The Global IoT Enterprise Spending dashboard shares data across regions, verticals, technology, and use cases with notable leaders in market growth in 2024 through the rest of the decade:

- Regional: China, India, and the US

- Vertical: Automotive and process manufacturers

- Technology: IoT software

- Use case: IoT-based process automation and IoT-based asset/plant/operations performance optimization

Note: IoT Analytics plans to release its IoT Use Case Adoption Report 2024 in Q3 2024. Those interested in accessing these reports when they are released can sign up for IoT Analytics’ IoT Research Newsletter at the top right of this article to receive updates on the release of these and other reports.

Regional market drivers

China, India, and the US expected to drive market growth. In 2024, companies in China, India, and the US are expected to grow their IoT spending by 17%, 14%, and 13%, respectively. IoT Analytics forecasts higher growth for these countries in the coming years, with China and the US expected to exceed the YoY global growth average through the end of the decade and India to exceed until 2028.

Vertical market drivers

Automotive and process manufacturers to consistently outpace enterprise IoT spending growth through 2030. The dashboard projects automotive manufacturers to grow their enterprise IoT spending by 14% in 2024 and 18% in 2025. Through the decade’s end, the difference between their enterprise IoT spending growth rate and the global average is predicted to remain between 1 and 3 percentage points higher.

The automotive sector is undergoing significant change towards electric vehicles (EVs), autonomous driving, and software-defined vehicles. This transition requires substantial investment in IoT for vehicle connectivity, real-time data processing, and integration of advanced driver-assistance systems (ADAS). Moreover, car manufacturers must redesign entire factories from producing vehicles with combustion engines to putting out smart electric vehicles. As the CEO of Renault, Luca de Meo, put it in the company’s Q1 2024 earnings call, “Transforming our industrial base puts us on track to reduce production costs by 30% for ICE and hybrid cars and by 50% for EVs by 2027. For example, deploying predictive maintenance AI tools resulted this year in a €270 million saving on energy and maintenance.”

Meanwhile, process manufacturers—those that utilize chemical, physical, or compositional changes to convert raw materials or feedstock into products—are expected to grow their enterprise IoT spending by 13% in 2024 and remain 1 to 2 percentage points above the YoY growth averages through 2030. Process manufacturers use IoT with the intent to enhance operational efficiency, improve safety, foster better communication, modernize operations, achieve scalability, and provide accessible data for informed decision-making. Examples of heavy IoT investment in this sector include Dow Chemical’s deployment of private LTE networks to modernize operations and enhance efficiency across their extensive Freeport manufacturing site. Such initiatives aim to improve operational efficiency, enhance worker safety, and streamline communication and collaboration.

Technology market drivers

IoT software expected to see strong growth through the end of the decade. All three subcategories of the IoT software segment—platforms (including platforms as a service), infrastructure as a service (IaaS), and applications (including software as a service)—are set to expand strongly in the next few years, following only a slight growth dip in 2024. IaaS and applications both appear set for continued 20%+ CAGRs.

AI integration set to drive enterprise IoT software spending. The integration of IoT with other emerging technologies, such as AI and machine learning, offers advanced features like predictive analytics, real-time monitoring, and AI-driven insights. That has the potential to enhance the appeal and utility of IoT software solutions. Based on IoT Analytics’ interviews with exhibitors at Hannover Messe 2024, and in contrast with their hardware counterparts, software vendors have a positive business outlook in 2024, largely driven by the excitement surrounding AI products and their growing adoption. Major IT vendors such as Microsoft, Amazon, and SAP, as well as systems integrators like Avanade and Cognizant, highlighted a strong focus on new AI and data-related projects.

Use case market drivers

IoT-based process automation and asset/plant/operations performance optimization are top priorities for enterprises. The use cases that are expected to see the highest spending growth are IoT-based process automation and asset/plant/operations performance optimization. Both are forecasted to see the highest levels of growth in 2024 and 2025 and exceed the average YoY global growth rates through 2030. And rightly so, since the investment usually pays off. One finding of the upcoming IoT Use Case Adoption Report 2024 is that only 2% of end-users who invest in an IoT-based process automation report a negative/zero ROI.

IoT market company dynamics

Among the 100+ companies included in the Global IoT Enterprise Spending dashboard, most can be grouped into one of six categories, each with distinct IoT market dynamics.

- Semiconductor companies: On average, the IoT portfolio of leading semiconductor companies had an overall revenue decrease of 6% in 2023. Strong demand for AI chips in IoT setups positively impacted companies such as NVIDIA and AMD, but this was insufficient to offset the economic and supply chain challenges that affected the industry.

- Industrial automation companies: Schneider Electric, Keyence, and Yokogawa were notable outperformers in this sector. Overall, industrial automation companies grew their IoT portfolios by 10.5% in 2023 despite economic challenges impacting the industry.

- Hyperscalers: Hyperscalers like Microsoft, Google, AWS, and Alibaba Cloud experienced an average growth of 19.2% for their respective IoT portfolios in 2023. The AI boom and strong adoption of new technologies globally drove this growth. Microsoft and AWS emerged as the primary beneficiaries of this and experienced solid growth in 2023.

- Professional services companies: This sector experienced modest growth, with an overall increase of 2.8% for IoT-related professional services in 2023. Deloitte and Infosys were notable above-average performers.

- Telcos: Telecommunications companies saw substantial revenue growth in 2023, with an overall increase of 19.7% for their IoT services. China Mobile, AT&T, and Vodafone were among the fastest-growing companies.

- Other IT companies: The IoT portfolio of other IT companies saw an average growth of 9.5% in 2023. Examples of companies with IoT offerings in this category include IBM, C3.ai, and HPE.

Analyst takeaway

Economic challenges—inflation, higher interest rates, or supply chain shortages—have impacted enterprise IoT market growth across the board. However, the Global IoT Enterprise Spending dashboard shows growth is around the corner in 2025. Already in 2024, we see market recovery for cellular IoT modules, which experienced a drop in shipments in 2023 due to inventory strategies stemming from supply chain issues. This rebound is just one of several positive indicators as we look forward to 2025. Also supporting this projected spending/revenue growth, senior enterprise IT decision-makers recently ranked IoT as 5th in tech prioritization for 2024 and 2025, a climb of one over 2023.

Note: This article updates previously shared IoT market size and enterprise IoT spending growth information with the latest market data and insights from IoT Analytics.

More information and further reading

Are you interested in learning more about the IoT market?

Global IoT Enterprise Spending (Q2/2024 Update)

An interactive dashboard and nested tracker containing global IoT enterprise spending data from 2019 to 2030.

Already a subscriber?

Browse your dashboard here →

Related dashboard and trackers

You may also be interested in the following dashboards and trackers:

Related publications

You may also be interested in the following reports:

- Quarterly Trend Report: What CEOs talked about in Q2/2024

- State of IoT Spring 2024

- IoT Enterprise Projects Adoption Report 2024

- 5G IoT & Private 5G Market Report 2024–2030

- IoT Mobile Operator Pricing and Market Report 2024-2030

Related articles

You may also be interested in the following articles:

- State of IoT Spring 2024: 10 emerging IoT trends driving market growth

- What CEOs talked about in Q2 2024: AI, data centers, and up-and-coming LLMs

- Top 5 enterprise technology priorities: AI on the rise, but cybersecurity remains on top

- Winning in IoT: How the enterprise IoT market is evolving

Subscribe to our newsletter and follow us on LinkedIn and Twitter to stay up-to-date on the latest trends shaping the IoT markets. For complete enterprise IoT coverage with access to all of IoT Analytics’ paid content & reports including dedicated analyst time check out Enterprise subscription.