In short

- The number of IoT platform companies did not grow in the last two years. IoT Analytics’ latest research found 613 IoT platform companies currently operating.

- Since 2019, many IoT platform companies have pivoted their business models: a number of companies no longer focus on IoT or have moved toward selling IoT solutions. Some have ceased to exist.

- The overall number of IoT platforms based in Asia-Pacific (APAC), especially China, increased strongly from 2019 to 2021, while the number of platforms in all other major global regions decreased.

Why it matters?

- IoT topics play an important role IoT platform companies are of major importance for the IoT ecosystem, and their consolidation impacts all other market participants.

Disclaimer: This article does not provide guidance or intend to compare the technical features of different IoT platforms. It looks at the market and compares platforms purely on a market meta level.

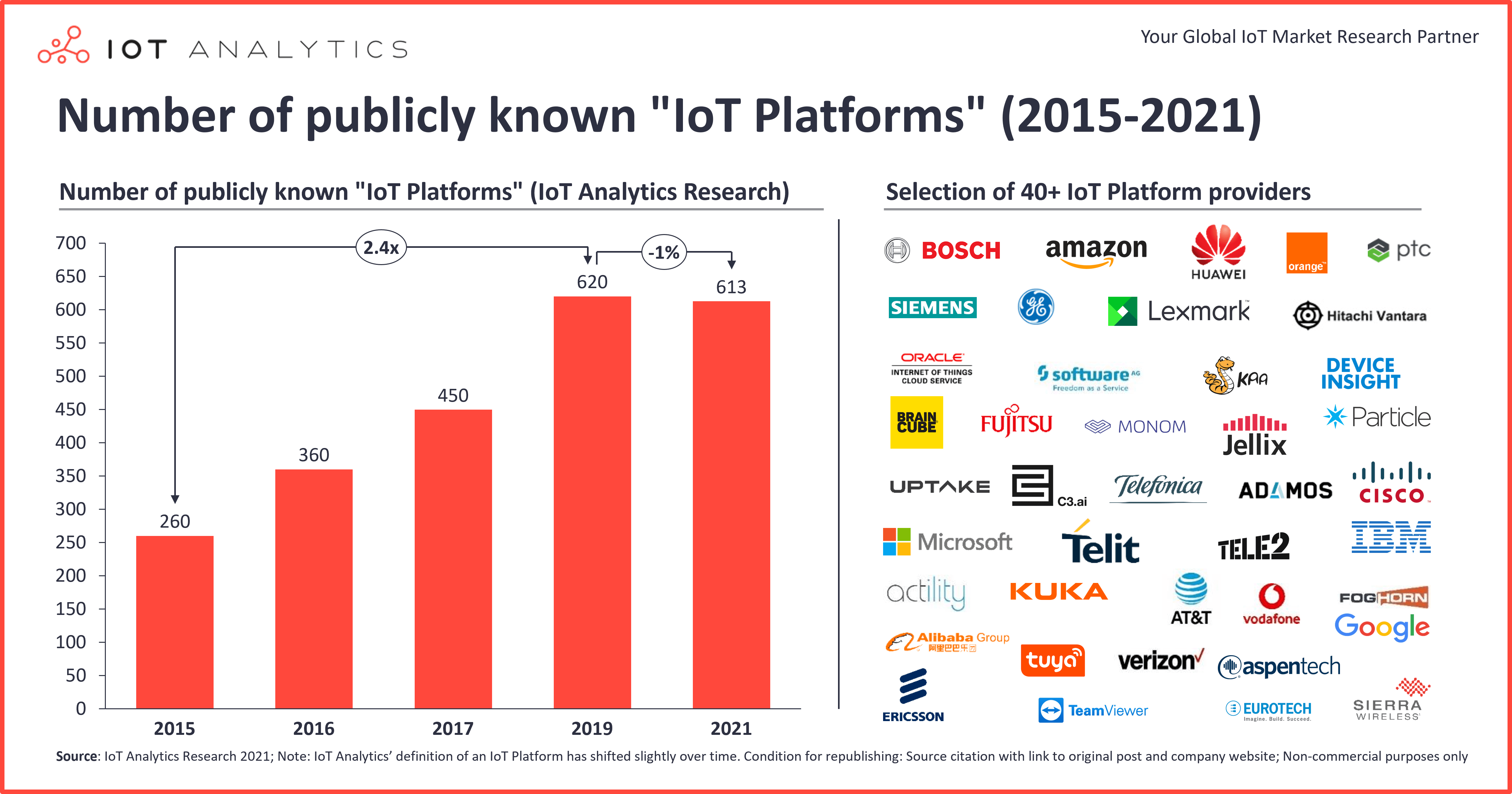

Two years ago, we identified 620 IoT platform companies globally on the open market (up from 450 companies identified in 2017).

The trend of more and more IoT platform companies on the market seems to have stopped and is now reversing, at least in the Americas, Europe, and the Middle East and Africa (MEA). For the first time, more IoT platform companies discontinued their operations than new ones were created. As a result, the number of IoT platforms is consolidating, and there are 613 IoT platform providers based on IoT Analytics’ latest research: IoT Platform Companies Landscape 2021 and 2021 List of IoT Platform Companies.

| What is an IoT platform?

An IoT platform is a specialized software tool used to build and manage IoT solutions. IoT Analytics classifies five different types of platforms: application enablement/management, device management, data management, telco connectivity/management, and IoT-based Infrastructure-as-a-Service (IaaS).

This latest research publication details the IoT platform company competitive landscape, classifies the technological capabilities of each IoT platform, identifies the main segments each platform targets, and ranks the leading platforms based on revenue and market share.

Some of the key findings from the competitive landscape report include:

1. The number of IoT platforms is no longer growing.

For the first time since 2015, the IoT platforms market is not growing. From 2015 to 2019, the number of publicly known IoT platforms more than doubled from 260 to 620. However, since 2019, that number has decreased slightly to 613.

The number of IoT platforms might have stopped growing, but the size of the market has still increased substantially. In 2020, $5 billion were spent on IoT platforms. The market is expected to grow to $28 billion in 2026. That constitutes a 33% compound annual growth rate (CAGR) for 2020 to 2026. The growth is fueled by the rapid adoption of cloud-based IoT platforms and the increasing number of customers choosing to buy (not make) IoT platforms.

Most IoT platforms offer application management/enablement capabilities (58% of the 613 IoT platforms). Data management is offered by 43% of all IoT platforms, and 35% offer device management. Fewer IoT platforms offer IoT telco management capabilities (7%) or infrastructure services/IaaS (3%).

For a detailed look at the typical components of IoT platforms, check out our recent analysis, Five things to know about the IoT platform market.

2. In the past two years, 188 IoT platform companies have discontinued operations.

Of the 620 IoT platform companies we identified in 2019, the majority (426) are still alive and active in 2021.

However, 188 of those companies are not considered IoT platform companies anymore:

- Some companies (26%) have ceased to exist and no longer offer their services.

Examples include DevicHub.net, iota Computing, and Yoics.

- Some companies (24%) no longer focus on IoT (but still offer a platform).

One example is Accenture, which rebranded its Insights Platform as AIP+ and now offers a collection of modular, pre-integrated AI services and capabilities not focused on IoT.

- Some companies (21%) have pivoted toward selling an IoT application or vertical solution or now have a security focus. Examples include Tellu and Centerity.

Tellu used to offer an IoT platform (TellluCloud) for all verticals but has pivoted to eHealth solutions. While the company still markets an eHealth platform, the main focus is on two healthcare solutions: digital supervision and remote patient monitoring.

Centerity in 2018 offered a broad data management solution, including a specific offering for original equipment manufacturers of connected products. The company has pivoted toward security and now offers one platform for advanced monitoring and security, in which IoT plays a minor role.

Seven IoT platform companies have been acquired since 2019, adding to a growing list of 84 IoT platforms acquired since we started tracking the market in 2015. Most of the acquired IoT platforms still operate today. Examples of IoT platforms acquired after 2019 include Brightwolf, which was acquired by Cognizant in November 2020 and is still active and operating, and Sprint’s Curiosity IoT platform, which was acquired by T-Mobile in April 2020 and is now fully consolidated into its parent company.

In addition, 182 new IoT Platform companies have emerged since 2019. The fact that 30% of all market players discontinued and almost the same percentage joined the market demonstrates that the market environment remains highly dynamic.

3. Many platform companies have pivoted their business models.

In the last two years, 30 platform companies have pivoted to an application or now offer a vertical solution instead of a horizontal IoT platform, and 10 now offer a security platform. Rather than choosing to compete with 620 other companies and invest millions of dollars into maintaining a highly modular and scalable software platform, those providers followed the demand for specific—sometimes niche—applications that allow them to build out competitive advantages in vertical-specific solutions.

This trend of pivoting toward solutions is more significant than the numbers suggest. Most current IoT platform companies are now offering vertical solutions alongside their platform offering.

One example is Device Insight. While the company maintains its IoT platform, CENTERSIGHT, it is increasingly focused on providing software for specific applications. Currently the company markets five individual IoT solutions: advanced analytics and predictive maintenance, condition monitoring and alarming, connected products, telematics/connected cars, and remote service and augmented reality.

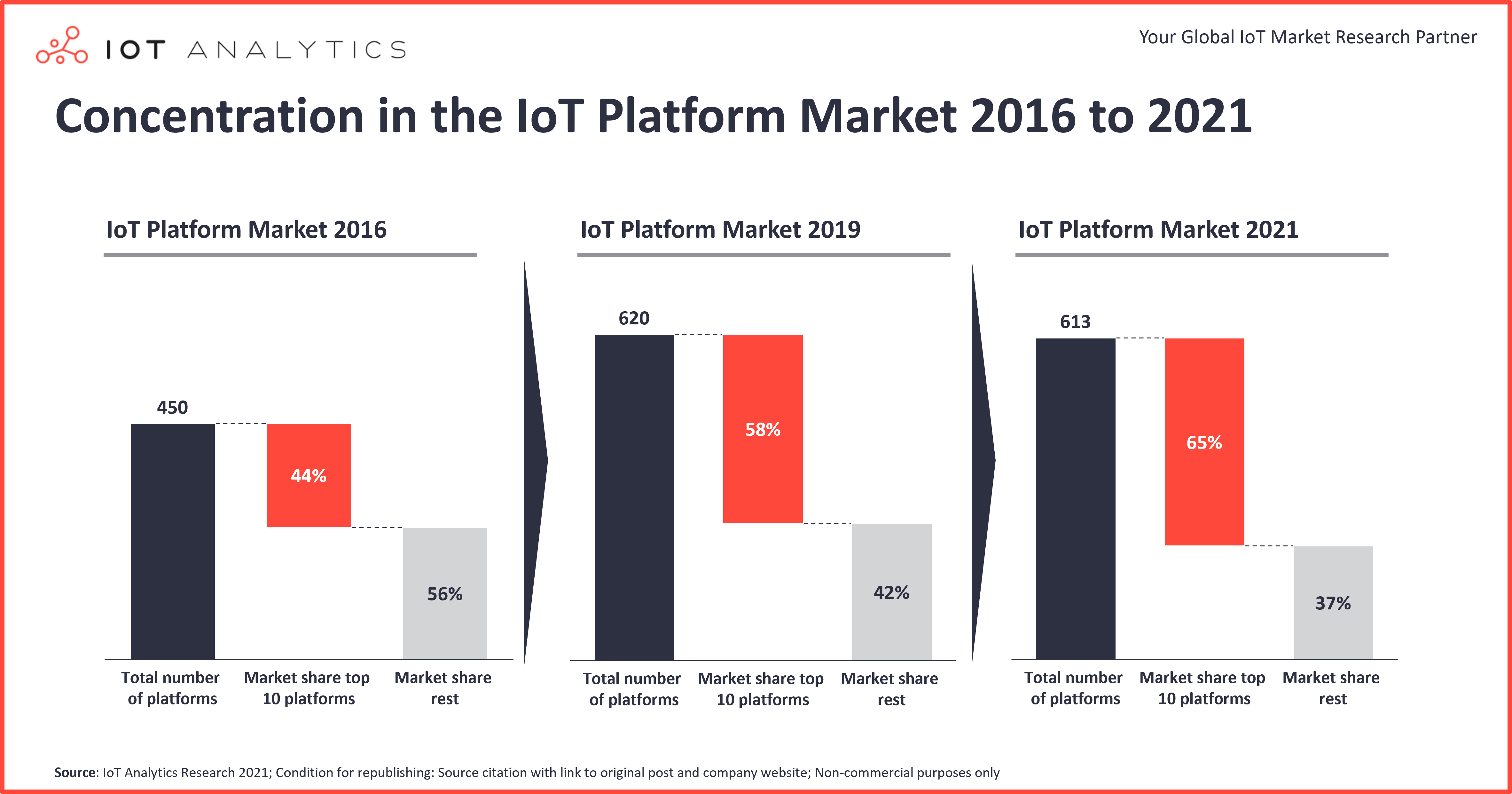

4. The market is concentrating further around a few providers.

The market for IoT platforms continues to concentrate, with the top 10 companies now controlling almost two-thirds (65%) of the entire market, compared to 58% in 2019 and 44% in 2016. The hyperscalers (Microsoft, AWS, and, to a lesser degree, Google Cloud, Alibaba, and some others) have become market leaders, and they continue to outgrow the overall market with growth rates of 50%+ per year.

Both AWS and Microsoft continue to add new capabilities to their growing portfolios of IoT platform services. Earlier this year, AWS introduced AWS SiteWise Edge to a wider audience, which allows customers to keep their industrial data on-premises, e.g., for lower latency or security reasons. Microsoft recently presented new capabilities of its IoT solutions for retailers utilizing cameras and sensors to enable smart spaces. Additionally, the company showcased its own use of Azure Digital Twins for building management. Microsoft aims to standardize a shared data model for Digital Twins (e.g., in the building space) as part of its cloud services.

5. The number of IoT platforms in APAC and China is rising.

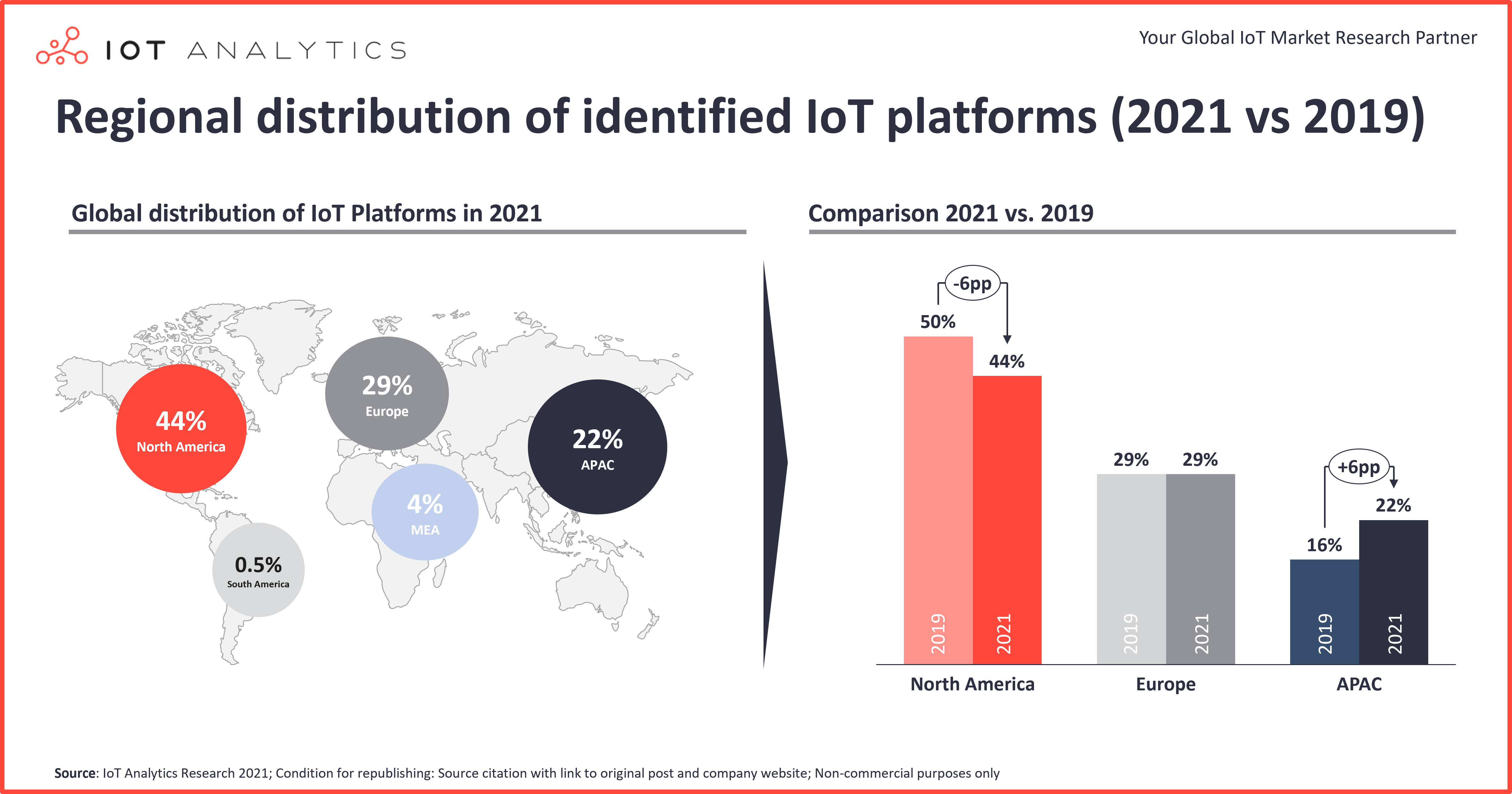

In June 2021, the Chinese government announced its goal of 3–5 industrial IoT (IIoT) platforms with international influence “made in China” by 2023. This agenda is being reflected in our research: the number of vendors from APAC (and especially China) has increased from 16% in 2019 to 22% in 2021. Shenzhen and Beijing are now among the top five cities for IoT platform company headquarters. While most IoT platform companies are still headquartered in North America (44%), their share has decreased by six percentage points in the last two years. Examples of the 66 Chinese IoT platform companies identified include tuya, Alibaba Cloud, Baidu IoT Core, and the Huawei Connection Management Platform.

More information and further reading

Are you interested in learning more about IoT Platforms?

The IoT Platform Competitive Landscape 2021 is part of IoT Analytics’ ongoing coverage of IoT Software/Platforms and helps executives gain an understanding of the different Internet of Things platforms across various geographies and industry verticals. The 84-page report provides insights on the Global IoT Platforms Landscape including:

IoT Platforms Competitive Landscape 2021

This 84-page insights report helps executives gain an understanding of the different Internet of Things platforms across various geographies and industry verticals.This report provides answers to the following questions (among others):

- How many IoT Platforms are in the global market and who are they?

- Which IoT Platforms have the largest market share?

- What is the market share breakdown by IoT platform type?

- Which segment do individual IoT Platforms focus on?

- What type of IoT technology do individual IoT Platforms focus on (on a high level e.g., application enablement, device management, data management, cloud storage/IaaS, Telco connectivity)?

- What are some of the recent platform trends and news?

- And more …

Sample

The sample of the report gives you a holistic overview of the available analysis (outline, key slides). The sample also provides additional context on the topic and describes the methodology of the analysis. You can download the sample here:

The report includes the 2021 List of IoT Platform Companies, a comprehensive company database, which is a structured repository classifying 600+ IoT Platforms that focus on providing modular software platforms for the Internet of Things.

The file also contains a structured list of 84 merged or acquired IoT Platforms as well as a structured list of 188 discontinued IoT Platforms (with reasons why the platform has been discontinued).

2021 List of IoT Platforms Companies

A comprehensive company database, classifying IoT Platforms, including revenue & market share estimates for 600+ IoT Platform vendors.

- General company information (company name, platform description, URL, company type, platform name and HQ location)

- Platform type (application enablement, device management, data management, cloud storage/IaaS, Telco connectivity)

- Other IoT technologies offered (Processors/Semiconductors, Communication hardware, Developer Tools, Analytics, etc.)

- Segment focus (Industrial/Manufacturing, Energy, Supply chain, Automotive, Smart Home, etc.)

- Further information (founding date, case studies, partner ecosystem, key customers, revenue estimates, etc.)

Bonus: The file also includes a list of recently merged or acquired IoT Platforms and recently discontinued IoT Platforms

Sample

The sample of the report gives you a holistic overview of the available analysis (outline, key slides). The sample also provides additional context on the topic and describes the methodology of the analysis. You can download the sample here:

Related articles

- 5 Things to Know About the IoT Platforms Market

- IoT Platform Companies Landscape 2019/2020: 620 IoT Platforms globally

- 6 IoT adoption trends for 2022

Are you interested in continued IoT coverage and updates?

Subscribe to our newsletter and follow us on LinkedIn and Twitter to stay up-to-date on the latest trends shaping the IoT markets. For complete enterprise IoT coverage with access to all of IoT Analytics’ paid content & reports including dedicated analyst time check out Enterprise subscription.