In short

- IoT enterprise spending reached $201 billion in 2022, significantly lower than many had previously predicted.

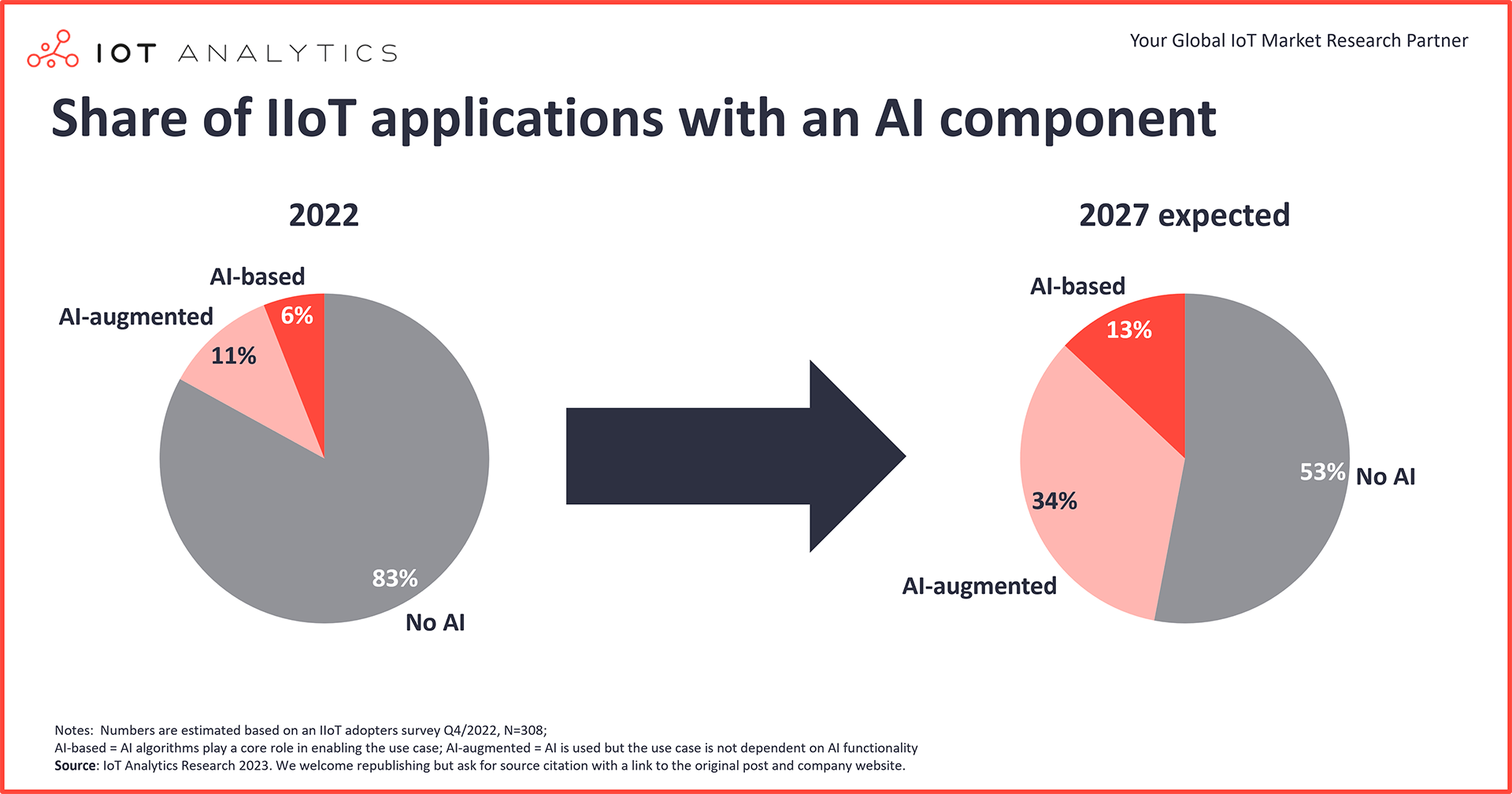

- IoT adopters will focus on building the IoT software backbone, developing IoT applications, and infusing AI in the coming five years. 47% of IoT applications are expected to have an AI element by 2027.

- Five things vendors focus on as they evolve their IoT strategies: ecosystem, solutions; AI vision; acquisitions; and open standards

Why it matters

- In a changing IoT market, companies need to constantly re-evaluate their positioning.

In 2017, BCG published a much-cited and discussed analysis, asking: “Where are the growth opportunities in enterprise IoT?” The authors discussed the growth opportunities along the IoT tech stack from 2015 to 2020. The conclusion: The top layers of the tech stack (services, applications, and analytics) will grow the fastest between 2015 and 2020 and will see the highest spending.

Today, six years later, we wonder: How accurate was the assessment by various industry analysts back then, and what does it take to win in a changing enterprise IoT market between 2023 and 2027?

Evaluating the IoT market vs. past predictions

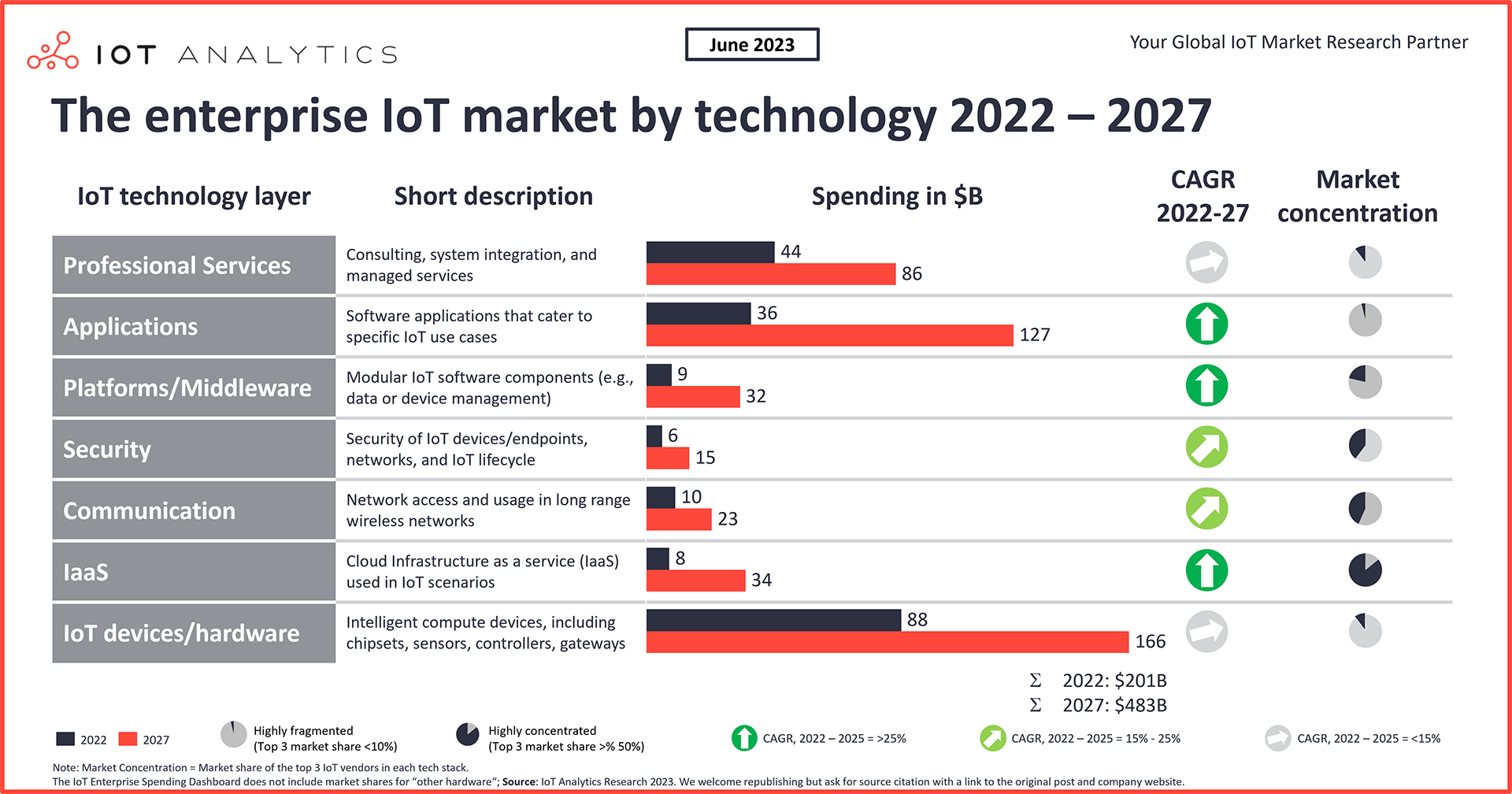

According to our January 2023 IoT market update, IoT enterprise spending reached $201 billion in 2022, up from below $100 billion in 2018. For comparison, this represents roughly 5% of the global IT market in 2022. While we had to lower the outlook for the forecast period of 2023–2027 in our January 2023 update, the market is still expected to grow by +19% annually and reach $483 billion in spending by 2027.

The IoT market is expected to reach $483 billion by 2027

The number of global active IoT connections grew by 18% in 2022 to 14.4 billion active IoT endpoints. In 2023, IoT Analytics expects the global number of connected IoT devices to grow another 16% to 16.7 billion. While 2023 growth is forecasted to be slightly lower than it was in 2022, IoT device connections are expected to continue to grow for many years to come.

How accurate were industry predictions in 2017?

We compare our market tracker that is based on actual revenues of 170+ companies in the IoT market to industry predictions of several third-party data providers that were cited by BCG in its 2017 article.

Our verdict: Industry predictions were directionally correct but too bullish on the pace of IoT adoption and on how fast different technology categories would shift.

- Total market size

- Industry prediction for 2020: $250 billion

- IoT Analytics IoT spending tracker: $136.6 billion. According to our estimates, the IoT market came out 45% lower than estimated. The market grew substantially in the 2015-2020 time frame but did not explode as had been projected by many (some segments, such as services, had been forecasted to grow 40%+ every year).

- Tech stack changes:

- Industry prediction for 2020: Services, applications, data analytics, and software platforms would substantially outgrow other parts of the tech stack.

- IoT Analytics IoT spending tracker: According to our data, this did happen. However, data analytics, applications, and services captured 39% of the market in 2020 and not 60% as forecasted by some data providers.

- Segment changes:

- Industry prediction for 2020: Discrete manufacturing, utilities, and logistics would make up the largest share of the market.

- IoT Analytics IoT spending tracker: Our data also show these three segments as being among the largest, but our view is that discrete manufacturing is even bigger than predicted.

Although we believe that general industry predictions (including our own predictions) were too bullish, we do see strong evidence that the market is growing further and now believe that the projected 2020 IoT market size of $250 billion will be surpassed at some point in 2024.

The IoT market in 2023 and beyond

IoT technology in 2023 adds value to organizations in all verticals, from manufacturing (e.g., factories) to retail (e.g., warehouses) and transport (e.g., cars). The IoT market has moved past headlines such as the infamous “3/4 of all IoT projects fail” (Cisco 2017).

87% of all IoT projects meet or exceed expectations

In 2023, 87% of all IoT projects met or exceeded expectations, based on a 2023 survey of 300 IoT decision-makers that will be published in an upcoming IoT Analytics adoption report. Some companies have connected millions of connected IoT devices (e.g., Walmart, Tesla, and Hapag-Lloyd) and are looking to expand with more sophisticated software tools. Despite several key challenges remaining related to interoperability, skills and know-how, and chipset supply, companies do not question if they should do IoT but rather how it will be scaling from here.

IoT technology maturity framework

To understand how the IoT tech stack is changing and where the growth opportunities in IoT are going forward, one needs to consider a typical technology-focused maturity curve an IoT adopter goes through:

Stage 1: Enabling the asset

In the first stage, whether it is a smart washing machine, a heavy asset in a factory, or a ship at sea, companies need to invest in sensors and local controllers/gateways to be able to process IoT data. Despite a renewed edge computing investment cycle that is seeing many companies invest into more powerful and flexible hardware, many companies at this point have passed the first hurdle of ensuring they have basic IoT data to work with. We expect the spending for IoT hardware/devices to be the lowest growth category at 14% until 2027.

Stage 2: Establishing connectivity

In the second stage, enterprise end users establish and simplify the connectivity to their IoT hardware. While some technologies used have been around for decades (e.g., certain field buses), companies in recent years have invested heavily into higher bandwidth connectivity (like ethernet), wireless connections (e.g., 4G/5G and LPWAN), and more modern and lightweight protocols (e.g., OPC-UA and MQTT). Spending on connectivity is expected to grow by 18% until 2027.

Stage 3: Creating the software backbone

Data normalization and analysis are key to the third stage of IoT maturity. Companies invest in the software backbone that allows them to access various IoT data sources and build valuable services, e.g., using cloud storage and platform services, centralized data lakes, containerization, and modern databases. Many companies are currently in a major investment phase in this part of the maturity curve. That is why we expected spending related to IoT Platforms and middleware to grow 30% and 34% for Infrastructure as a Service (IaaS) until 2027.

Stage 4: Building value adding IoT applications

In the fourth stage of IoT maturity, IoT end users build cloud native or edge-based applications that make use of IoT data at scale. The ability to connect to any asset (stage 1) in a standardized fashion (stage 2) and having those data easily accessible (stage 3) enables a number of IoT use cases. Some of the early innovators (e.g., several automotive OEMs) have reached this stage and are building all kinds of internal (e.g., for their factories) and external (e.g., for their cars) IoT applications. We expect more companies to reach this stage of maturity in the coming years, which is why we expect the spending on IoT applications to exhibit a CAGR of 29% until 2027.

Stage 5: AIoT = infusing AI into IoT

Enabling business with AI is the fifth stage of IoT maturity. This is where companies explore ways to augment existing applications and build new applications by embedding AI. Machine vision and predictive maintenance are two of the most common AI-enabled IoT use cases today. Recent breakthroughs in generative AI may add a new dimension and are a driver for companies to rapidly adopt AI further.

The shift toward AIoT: Nearly half of all IoT applications to be AI-infused by 2027

Although some companies are still struggling to enable their assets (stage 1) and establish connectivity (stage 2), the future of IoT is the convergence of AI and IoT, also often referred to as AIoT.

The future of IoT is the convergence of AI and IoT

In 2022, we conducted a survey of 500 senior IT and engineering staff at manufacturing companies. 15% of those companies indicated having fully implemented their AI strategy (results are part of the Industry 4.0 Adoption Report 2022). Two key use cases with an AI component that were cited were machine vision and predictive maintenance, both scoring a consistently high ROI for these companies.

Based on the data we have and the discussions we lead with various organizations, we estimate that approximately 6% of IIoT applications today are AI-based, meaning that AI algorithms play a core role in enabling the use case (i.e., when using machine learning for vision detection in quality control). Another 11% of applications are classified as AI-augmented, meaning that AI does play a role for the use case, but the use case is not dependent on that AI functionality (e.g., AI-augmented AGV/AMR routing instead of using rules decided by operators).

We see a strong push toward embedding AI into IoT applications (e.g., by moving from condition monitoring to predictive maintenance) and expect a strong increase in the next years.

By 2027, we forecast nearly half of all IIoT applications to have some AI element with the share of AI-augmented applications tripling in that time frame (from 11% to 34%). Many software vendors are currently undergoing large internal exercises on how they can augment their existing software offerings with the use of AI. In May 2023, for example, SAP announced 15 new business AI capabilities across the existing ERP product portfolio, including nine new generative AI scenarios.

Not everything is required to be AI-based, however. Many legacy non-AI IoT applications that are already deployed may not be touched. Many rule-based applications will remain sufficient for some clients and uses cases, and not every dashboard will need to be AI-augmented.

The hype around ChatGPT and Generative AI is likely to impact the AI strategy of companies in the coming years. It is still early to tell if and how quickly the implementation of generative AI in IoT will lead to new large-scale use cases. Generative AI models predominantly focus on text and images, with only a few models centered around sensor data at this point.

“We see a strong push now to bring AI into the business landscape, with the expectation that AI will reengineer enterprises as completely as enterprise software did three decades ago.”

Ravi Kumar, CEO, Cognizant, 2 February 2023

Winning in IoT: How vendors are positioning themselves

With users more focused on building the software backbone, developing applications, and infusing AI, the combined IoT software opportunity is expected to amount to $193 billion by 2027. In 2022, no single vendor had more than 3% market share in the $201 billion global IoT market, and no single vendor had more than 9% market share in the IoT software market. (Note: IoT Analytics tracks 170+ vendors and their market share by IoT segment—see the most recent update of the IoT Enterprise Spending Dashboard.)

No single vendor has more than 3% market share in the IoT market

IaaS (top three vendors: 86% market share) and wireless connectivity (top three vendors: 44% market share) are the only IoT tech stack elements that are largely consolidated at this point—the other areas leave plenty of room for innovation and consolidation.

The insights from this article are based on market data from the Global IoT Enterprise Spending Dashboard, an interactive dashboard and nested tracker containing global IoT enterprise spending data from 2017 to 2027.

Request a demo to experience a walk-through of the dashboard via screen share, get your specific questions addressed, and explore how our research can add value to your organization.

Already a subscriber? Browse your dashboards here →

You are currently viewing a placeholder content from Default. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationHere are examples of some of the strategies that leading IoT vendors are pursuing as they gear up for the next five to ten years in the IoT market:

Strategy 1: Multiplying the opportunity by building a strong ecosystem of partners

The complexity of IoT has led some of the leading organizations to build an ecosystem of complimentary partner companies to help in their go-to-market and delivery. This strategy is most notable with the leading hyperscalers Microsoft, AWS, and Google.

For example, at Hannover Messe 2023 (the world’s leading industrial fair), we counted 32 partners co-exhibiting with AWS, 25 with Microsoft, and 24 with Google (see our Hannover Fair event report for more details). Although these companies are technically also customers of the hyperscalers, significant time and resources go into developing joint solutions, building architectures together, and marketing the joint offerings. AWS, for example, marketed joint solutions with Element Unify, HighByte, Deloitte, and TensorIoT at the fair.

Strategy 2: Focus on solutions that solve customer problems

A few years ago, many vendors focused on selling a platform that would allow IoT adopters to build applications themselves. However, many IoT adopters, especially SMEs, have found that they do not have the resources to make this happen. Some of the vendors that previously provided an IoT platform have adjusted accordingly and moved on to providing IoT solutions to individual problems and use cases, rather than a universal, hard-to-maintain platform. In some cases, these solutions bundle existing hardware or sensors with access to cloud-based software so that IoT adopters can receive everything they require from one vendor.

For example, in 2022, Swedish sealing and bearing company SKF launched SKF Axios, a wireless predictive maintenance solution geared toward monitoring equipment and improving equipment uptime. The solution leverages several AWS cloud services and provides necessary sensors, gateways, wireless connectivity, and a ready-to-use application so that customers have the entire solution ready to go.

Strategy 3: Embedding a bold AI vision into the strategy

As the IoT enterprise market is starting to look at the fifth stage of maturity (AIoT), some vendors appear to be bolder and more committed to leading the AI race than others.

For example, Japanese industrial automation vendor Yokogawa is building the vision of industrial “autonomous operations” into the company strategy, believing that the future of manufacturing is AI-based. In March 2023, Yokogawa announced the adoption of Yokogawa’s Autonomous Control AI at an ENEOS Materials Chemical Plant. The field test demonstrated that AI could control distillation operations more effectively than existing human-controlled approaches, resulting in stable product quality, high yield, and energy savings.

Strategy 4: Acquiring missing puzzle pieces

Rather than partnering, some companies opt to acquire certain IoT technologies or applications that they consider high value.

In May 2022, for example, Emerson Electric acquired Aspen Technology to create a leading industrial software company. The acquisition, among other things, gives Emerson Electric access to a strong Industrial AI portfolio, including numerous asset intelligence solutions.

In June 2022, Siemens acquired Senseye, a provider of AI-powered solutions for industrial machine performance and reliability.

As part of our recent State of IoT—Spring 2023 report, we looked at the 100 most recent acquisitions in the IoT space. We found that the largest group (26%) of acquired companies was in the applications space—many with a strong AI footprint.

Strategy 5: Betting on open standards

Open standards promise to solve one of the biggest inhibitor to large scale IoT adoption: Missing interoperability and compatibility among various IoT devices and systems.

By aligning their solutions with open standards, vendors hope to significantly improve the customer experience, fostering innovation, flexibility, and scalability in their IoT deployments.

Schneider Electric, for example, is actively promoting the use of IEC 61499, a shared source runtime execution engine, developed by Universal Automation. The standard aims to create hardware-independent applications to bridge the existing gap between IT and OT.

In our Hannover Messe 2023 event report, we highlighted that we noticed several big brands aligning behind the Asset Administration Shell (AAS) framework to develop interoperable digital twins. Among many companies, Microsoft, Siemens, and SAP seem to be three of the most notable supporters.

Conclusion

IoT continues to offer tremendous opportunities, even if the market is not advancing as fast as some had predicted in the past. IoT enterprise spending is expected to increase to $483 billion by 2027. In a maturing IoT market, the biggest growth opportunity lies in the software, especially with (AI) applications.

The biggest IoT growth opportunity lies in software

Nearly half of all applications in 2027 will be AI driven. Leading IoT vendors, such as hyperscalers, industrial automation vendors, and connectivity providers, and also many start-ups position themselves to stay relevant in an AI-first IoT market. With a clear IoT strategy, companies have an opportunity to position themselves in what remains one of the biggest market opportunities of our generation.

More information and further reading

Are you interested in learning more about the IoT market?

IoT Enterprise Spending (Update Q1/2023)

An interactive dashboard and nested tracker containing global IoT enterprise spending data from 2017 to 2027.

- 100+ countries from seven world regions

- 10 types of technology stack elements

- 11 IoT segments

- 75+ industries

- 40+ use cases

- Export data option

You are currently viewing a placeholder content from Default. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationRelated dashboard and trackers

You may also be interested in the following dashboards and trackers:

- Global Cellular IoT Module and Chipset Market Tracker & Forecast

- Global Cellular IoT Connectivity Tracker & Forecast

Related publications

You may also be interested in the following reports:

- State of the IoT – Spring 2023

- Hannover Messe 2023—the latest Industrial IoT/Industry 4.0 trends

- Quarterly Trend Report: What CEOs talked about in Q1/2023

- IoT Software Adoption Report 2023

- Machine Vision Market Report 2022-2027

- Industrial AI and AIoT Market Report 2021–2026

- Industry 4.0 Adoption Report 2022

Related articles

You may also be interested in the following articles:

- State of IoT 2023: Number of connected IoT devices growing 16% to 16.7 billion globally

- The top 10 industrial technology trends—as showcased at Hannover Messe 2023

- CEO priorities from 2019 until now: What has changed?

- 10 notable telco IoT trends—based on insights gathered in Q1 2023

- The leading IoT software companies 2023

- Global IoT market size to grow 19% in 2023—IoT shows resilience despite economic downturn

- The rise of industrial AI and AIoT: 4 trends driving technology adoption

Subscribe to our newsletter and follow us on LinkedIn and Twitter to stay up-to-date on the latest trends shaping the IoT markets. For complete enterprise IoT coverage with access to all of IoT Analytics’ paid content & reports including dedicated analyst time check out Enterprise subscription.