As we start 2023, the IoT Analytics team has again evaluated the past year’s main IoT developments in the global “Internet of Things” arena. This article highlights some general observations and our top 10 IoT stories from 2022, a year characterized by a skyrocketing inflation rate, ongoing supply disruptions, and a looming recession. (For your reference, here is our 2021 IoT year-in-review article)

General IoT 2022 market

2022 was a year of uncertainties and a number of (mostly negative) macroeconomic surprises. The 4.4% global growth forecast for the year (from January 2022) was almost certainly not reached, and the outlook for 2023 has been lowered to a meager 2.7% (as of Oct 2022). The Nasdaq Composite, one of the key indices for technology companies, fell 33.1% in 2022.

Against this backdrop, IoT 2022 markets held up somewhat steadily, with the number of connected IoT devices growing to approximately 14.4 billion (exact update coming in a few weeks) with roughly $202 billion in IoT enterprise spending (IoT Analytics will publish the 2022 IoT spending actuals shortly).

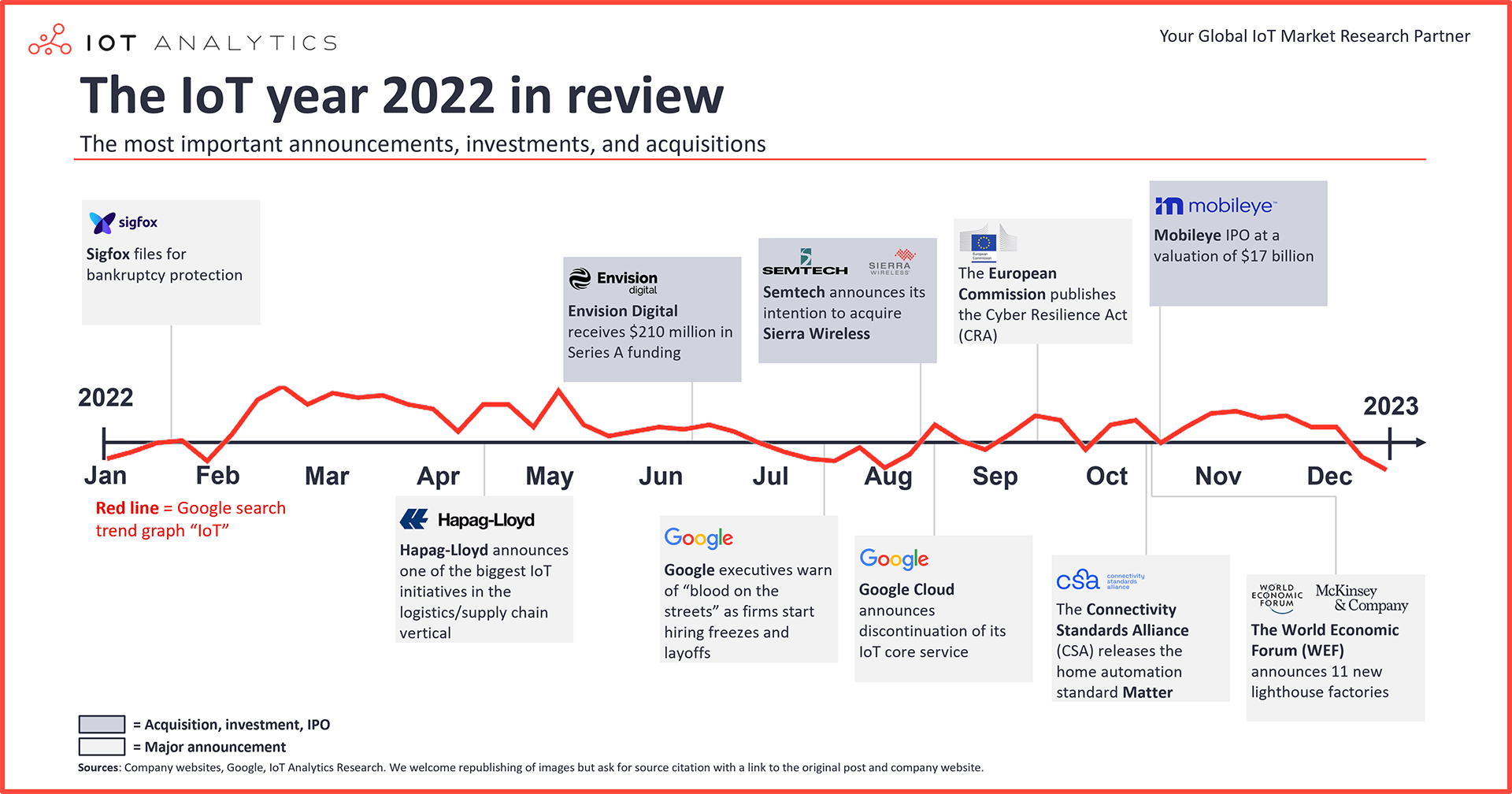

The public relevance of the term “IoT,” which had been on the decline since October 2018, climbed back up by more than 30% to reach its all-time high levels in Q1 2022. (See Google trend graph in the lead image of this article).

For us at IoT Analytics, the increased public search interest for IoT reaffirms some of the developments we have witnessed over the past 2–3 years:

- A maturing IoT stack both in the cloud and now more and more at the edge (see for example our report on 55 emerging IoT technologies or our IT/OT convergence report from SPS 2022)

- A number of Fortune 500 companies making large investments in IoT projects

- The vast majority of end-users reporting faster project roll-out and faster investment payback times for their IoT projects (We will publish more data on that in April 2023).

Top 10 IoT 2022 stories

Throughout 2022, we monitored significant developments regarding IoT technology. In our opinion, these are the top 10 stories of IoT 2022 (in chronological order):

1. Most accelerated IoT vertical: Supply chain

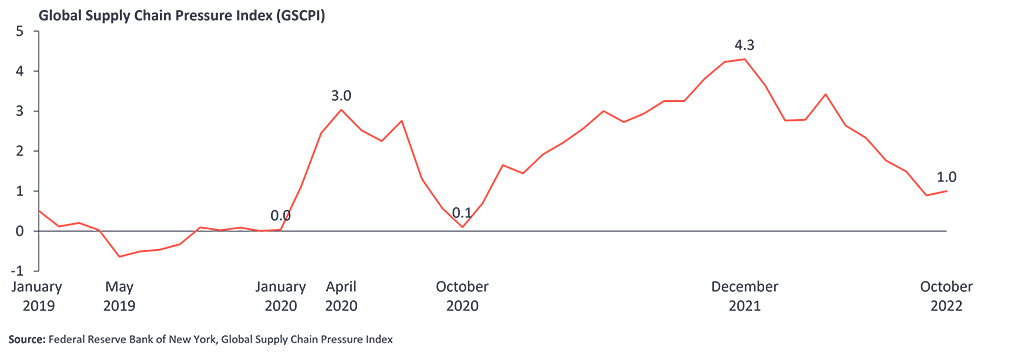

In the aftermath of the global pandemic and war in Ukraine, reports of congested ports, suppliers halting production, or critical cargo going missing became normal news in 2022. Supply chain disruptions dominated CEO discussions well into the second half of 2022 (for example, see our quarterly trend report: What CEOs talked about in Q3/2022).

The lack of supply chain visibility resulted in a sharp increase in interest in a number of supply chain technologies, such as visibility software, intralogistics robots, or IoT track-and-trace devices (see here for a list of five other trending supply chain technologies).

Although supply disruptions eased significantly throughout 2022 (The Global Supply Chain Pressure Index peaked in Dec 2021—see below), several large companies made major digital supply chain initiatives public.

In April 2022, the German company Hapag-Lloyd, a market leader in ocean shipping, announced one of the biggest IoT adoption initiatives in the logistics/supply chain vertical. The company plans to equip its entire global fleet of dry containers (approximately 1.6 million containers) with track-and-trace devices (supplied by Swiss vendor Nexxiot and U.S.-based vendor Orbcomm). The company hopes to provide its customers with much-improved information about the whereabouts and the status of their goods and a more accurate estimated arrival time.

In June 2022, the world’s largest retailer, Walmart, announced a number of new state-of-the-art and highly automated fulfillment centers (supplied by intralogistics robot vendors Knapp, Symbotics, and Witron). The new fulfillment centers, which are all located in North America, are designed to set the pace of automation for Walmart’s 4,700 stores and 210 distribution centers globally.

In April 2022, the world’s largest e-commerce company, Amazon, announced the creation of a $1 billion venture investment program to fund companies that help automate and digitize Amazon’s fulfillment operations.

2. IoT Security breach of the year: None

We highlighted major IoT security breaches in many of our “IoT year in review” analyses of previous years. In IoT 2022 we did not witness a major IoT security incident so big that it can be singled out. We interpret this as a positive sign and a direct result of the investment that has gone into security research and solutions in the last years.

We would still want to highlight that this does not mean that vulnerabilities in IoT systems do not exist. In contrast, several critical vulnerabilities were discovered in 2022, and their corresponding advisories were issued.

The Nozomi August 2022 OT/IoT Security Report found that 303 Common Vulnerabilities and Exposures were released in the first half of 2022. Of these, 109 affected critical manufacturing systems directly. Interestingly, the SQL Injection technique tops the chart with the highest number of associated vulnerabilities for the Industrial Control System (ICS) in 2022. Other common critical weaknesses included misused authentications, improper access controls, and integer overflow vulnerabilities. Microsoft’s Cyber Signals December 2022 report identified unpatched, high-severity vulnerabilities in 75% of the most common industrial controllers. The same report also mentioned a “78% increase in disclosures of high-severity vulnerabilities from 2020 to 2022 in industrial control equipment produced by popular vendors.”

The INCONTROLLER vulnerability, discovered in April 2022, stood out to us at IoT Analytics due to its great potential harm. Below is a list of five vulnerabilities that caught our attention in 2022:

- INCONTROLLER vulnerability. In April 2022, Mandiant and Schneider Electric jointly revealed an ICS attack tool/framework named INCONTROLLER (also called PIPEDREAM), which has the ability to gain complete access to SCADA systems and various Schneider Electric and Omron PLCs. INCONTROLLER was rated rare and dangerous, comparable to the likes of TRITON (2017), INDUSTROYER (2016), and STUXNET (2010). Luckily, INCONTROLLER was discovered before any incidents.

- Industroyer2. In April 2022, we also saw the emergence of Industroyer2. It is a variant of the Industroyer malware that was used to attack Ukraine’s power grid in 2016 and cut power to 20% of Kyiv for approximately an hour. The malware targets IEDs in electric substations that communicate over IEC-104 (IEC 60870-5-104) protocol.

- Mitsubishi PLC vulnerabilities. In August 2022, Nozomi researchers identified three security holes (CVE-2022-29831, CVE-2022-29832, and CVE-2022-29833) that could allow an attacker to obtain information from Mitsubishi GX Works3 (configuration and programming software for certain Mitsubishi PLCs)project files to compromise connected safety CPU modules.

- Lanner controller vulnerabilities. Approximately a dozen new Baseboard Management Controller firmware flaws in Lanner controllers were discovered in November 2022, potentially exposing OT/IoT networks to remote attacks.

- PTC Axeda remote access vulnerabilities. In March 2022, Researchers from CyberMDX, a healthcare security firm, found seven easily exploited vulnerabilities (called Access:7) in the PTC Axeda remote access tool. Such vulnerabilities could potentially allow the extraction of data from medical equipment, the tampering of lab results, or the making of critical devices unavailable. The researchers estimated that the Access:7 vulnerabilities could compromise thousands of devices out in the field.

3. Biggest 2022 funding round: Envision Digital

2022 was a tough year for start-up funding. An analysis by Pitchbook shows that the number of funding rounds and the average deal size declined across almost all start-up sectors. Edtech start-ups suffered the most, with total deal value dropping by 60% compared to 2021. The biggest IoT 2022 funding round was a $210 million Series A funding round of Envision Digital in June 2022. The company operates in the “climate technologies” sector, which stood out from the other sectors with a 41% median valuation increase in 2022.

Envision Digital sells an AIoT platform called EnOS™, which helps organizations manage the production of renewable energy and orchestrate efficient consumption to achieve net zero carbon emissions. The company markets pre-built decarbonization and digitalization applications for energy, manufacturing, transportation, and utility industries. The Shanghai-based company, founded in 2017, claims to manage more than 220 million smart devices and 568 gigawatts of energy assets globally.

Other notable funding rounds for IoT and sustainability-related companies in 2022 included Morse Micro. This fabless semiconductor company is reinventing Wi-Fi for IoT by building chips and modules based on the new Wi-Fi HaLow standard, which consumes less energy. The company raised approximately $94 million in funding via two funding rounds. Span.IO, a renewable energy start-up, received $90 million in funding. It offers a smart electrical panel that allows homeowners to use an app to monitor and optimize power consumption, thus giving them more control over how their cars and homes are powered. Canada-based Validere, which offers an all-in-one commodity management platform for the energy industry, raised $43 million. The platform enables companies to improve their operations and make better emissions decisions.

The second-highest IoT funding round in 2022 was a Series D of U.S.-based Verkada. We covered the company in our 2021 year in review due to a major security breach in which hackers had compromised the security feeds of thousands of IoT security cameras.

Germany-based Kinexon is another notable start-up, occupying fourth place. The company, which offers real-time location data and an analytics platform in both the manufacturing and sports verticals, not only made headlines in 2022 for its $130M Series A but also for the use of its Connected Ball Technology in the recently concluded 2022 FIFA World Cup. This very technology denied Cristiano Ronaldo a goal by confirming that he had not made contact with the ball in the Portugal vs. Uruguay game.

| Company | Funding stage | Amount | Country | Category | Lead investor |

|---|---|---|---|---|---|

| Envision Digital | Series A | $ 210 M | China | AIOT Platform/Sustainability | Sequoia Capital China |

| Verkada | Series D | $ 205 M | USA | IoT Security | Linse Capital |

| Helium | Series D | $ 200 M | USA | IoT Connectivity | Andreessen Horowitz, Tiger Global Management |

| Kinexon | Series A | $ 130 M | Germany | Track & Trace | Thomas H. Lee Partners |

| TXOne Networks | Series B | $ 80 M | Taiwan | IoT Security | TGVest Capital |

4. Most talked about merger/acquisition: Semtech and Sierra Wireless

In August 2022, semiconductor company Semtech announced its intention to acquire IoT module and wireless communications equipment manufacturer Sierra Wireless in an all-cash deal valued at $1.2 billion. The deal is set to integrate Semtech’s LoRa wireless modulation technology into Sierra Wireless’ cellular modules, which use technologies such as NB-IoT and LTE-M and combine the two companies’ cloud services platforms. The deal is expected to close soon, pending approval by regulatory bodies. In October, each company received a request for additional information and documentary material (commonly known as a “second request”) from the U.S. Department of Justice.

In another significant IoT 2022 deal, Siemens Infrastructure acquired Brightly Software for $1.6 billion in June. U.S.-based Brightly Software provides asset and maintenance management SaaS solutions to schools, governments, hospitals, and manufacturers globally. The deal is expected to boost Siemens’ smart cities and sustainable business significantly while increasing its visibility in the US. Siemens president Roland Busch called the deal “another important step in the company’s stated strategy to become a focused technology company.” The acquisition solidifies Siemens as a leader in the software market for buildings and built infrastructure.

Another interesting IoT acquisition is Pelion by Izuma Networks, an edge computing services provider founded in April 2022. In October 2022, the company announced that it had received a strategic investment from Softbank to acquire Softbank’s Pelion edge software business once again. In 2020, ARM spun off Pelion as an independent SoftBank business unit, and it was originally the device management business of ARM. Izuma is planning to use the investment from Softbank to hire new talent, improve IoT services, and integrate edge and IoT services under one umbrella. Izuma Edge is an open-source software stack that securely deploys and manages applications at the edge using Docker and Kubernetes orchestration technologies.

In another high-stakes acquisition, SigFox was acquired by UnaBiz in April 2022 from a group of nine bidders. Until recently, Sigfox was a celebrated player in the IoT connectivity space with its proprietary narrowband (LPWA) technology positioned as an alternative to 2G/3G. However, it went into insolvency in January 2022. While UnaBiz will save Sigfox from insolvency, the question regarding the acceptance of the technology in the market remains.

Schneider Electric, which already owned nearly 60% of Aveva, took over Aveva for an increased valuation of $11.6 billion. The deal of the Cambridge-listed Aveva was cleared by the U.K. government on December 7, 2022. This is the third time lucky for Schneider Electric after two initial unsuccessful attempts to acquire Aveva. The deal enables Schneider Electric to provide powerful digital transformation solutions on top of its EcoStruxure™ platform. In 2021 Aveva acquired OSIsoft, the maker of the popular PI System, the leading data management platform for industrial operations.

| Acquirer | Acquired company | Deal size | Category |

|---|---|---|---|

| Schneider Electric | Aveva | $ 11.6 B (60% ownership prior to complete acquisition) | Industrial IoT |

| Siemens | Brightly Software | $ 1.6 B | Industrial Software |

| Semtech | Sierra Wireless | $ 1.2 B | IoT Connectivity |

| Yageo | Telemecanique Sensors | $ 714 M | IoT Sensors |

| Qualcomm | Cellwize | $ 300 M | Edge |

| Izuma Networks | Pelion – Device Management Business | n/a | Edge |

| Johnson Controls | FogHorn | n/a | Edge |

| Renesas Electronics Corporation | Reality AI | n/a | Edge |

| Infineon Technologies | Industrial Analytics IA | n/a | Data/Analytics |

| Telit | Telit Cinterion | n/a | IoT Connectivity |

| Schneider Electric | Autogrid | n/a | Data/Analytics |

| UnaBiz | Sigfox | n/a | IoT Connectivity |

| Aeris | Ericsson – IoT Accelerator | n/a | IoT Platform |

5. Biggest impact on the IoT job market: Tech layoffs

Layoffs and hiring freezes marked headlines throughout the second half of 2022. Fears of an economic slowdown saw a host of leading tech companies, such as Meta, Twitter, Salesforce, Microsoft, HP, Tesla, Cisco, and others, shed some portion of their workforce. In July/August 2022, Google executives conveyed a stark message to their sales teams: “There will be blood on the streets!” Although Google has since not announced any layoffs, others have. The first reports of looming layoffs at Intel started circulating in October, and Meta announced the layoff of 11,000 employees in November 2022. The same month, Cisco announced its plan to cut 5% of its workforce, approximately 4,100 employees, as part of a company-wide $600 million restructuring plan.

What is noticeable is that many vendors offering IoT solutions seem only somewhat affected. In July 2022, Microsoft removed open job listings for its Azure Cloud and security groups. In late October 2022, Amazon froze hiring in AWS. Based on publicly available information, none of the major industrial automation giants, including Siemens, Schneider Electric, Emerson, Rockwell, and others, announced any layoffs.

The layoffs, though always painful, could be a blessing in disguise for the talent-hungry IoT companies that seemingly keep hiring and have been dipping into the same talent pool with the likes of Meta, Twitter, and others (and often on the poor side of the bargain).

6. Most surprising IoT divestiture: Google

In August 2022, Google made the surprising announcement that it would discontinue its IoT core service on August 16, 2023 (one year from the announcement date), when access to its IoT Core Device Manager APIs will no longer be available. The news rocked the IoT world, as some large corporations decided to base their IoT initiatives on Google Cloud. Those corporations suddenly found themselves having to re-architect their solutions, a process that can take weeks or even months.

We at IoT Analytics predicted an unfolding market consolidation in November 2021. Although we did point out that Google was falling way behind AWS and Microsoft Azure for IoT services in an analysis in February 2022, we did not see this move coming.

In November 2022, three months after Google, in a nearly equally important announcement, IBM announced that it would also be retiring its Watson IoT Platform, effective December 1st, 2023. This means new IoT devices will not be able to connect to the MQTT and HTTP endpoints of Watson, and existing connections will be shut down. The announcement followed news from earlier in the year that IBM had sold off Watson Health and was deprecating its IBM Cloud Foundry (an open-source PaaS on IBM Cloud that enables customers to deploy and scale applications).

In July 2022, another IT giant, SAP, started to retire its IoT services (and all its predecessor services). A host of other SAP IoT services, such as SAP IoT Edge, have also been put on the deprecation list.

In December 2022, Ericsson announced that it was selling its IoT Accelerator and Connected Vehicle Cloud businesses to Aeris Communications. The IoT Accelerator from Ericsson is a platform that enables enterprises to deploy, manage, scale, and control IoT devices throughout their lifecycle.

In our view, all of the above IoT divestitures are from companies whose IoT divisions failed to meet the targets set by management. In the case of Google, IBM, and SAP, the companies failed to gain significant traction and started to fall behind their competitors (e.g., AWS and Microsoft). The case of Google is especially curious, as IoT continues to be a growing market that is still far from being very mature. With Google having a strategic focus on “industry value propositions,” it is unclear why the company relies on third parties to connect IoT devices.

7. Most important government initiative: E.U. Cyber Resilience Act

In September 2022, the European Commission published the Cyber Resilience Act (CRA), aiming to set cybersecurity standards for secure hardware and software products placed on the market across the E.U. The act aims to plug the holes in the existing E.U. legislation related to cybersecurity that does not directly cover mandatory requirements for the security of products with digital elements.

The CRA defines “products with digital elements” as any software or hardware product and its remote data processing solutions, including software or hardware components that are sold in the market separately.

The act establishes guidelines for developing products such that fewer vulnerabilities exist in released products and throughout their life cycles. It also aims to create conditions whereby users can take cybersecurity into account when selecting and using products with digital elements. Product manufacturers will need to perform risk assessments and produce technical documentation to demonstrate that their products meet the essential requirements.The CRA also distinguishes based on product criticality to account for the different levels of cybersecurity risk associated with the product types.

Four specific objectives were set out as part of the CRA:

- Ensure that manufacturers improve the security of products with digital elements from the design and development phase and throughout the whole life cycle.

- Ensure a coherent cybersecurity framework, facilitating compliance for hardware and software producers.

- Enhance the transparency of security properties of products with digital elements.

- Enable businesses and consumers to use products with digital elements securely.

8. Upcoming IoT connectivity standard: Matter

After its initiation in December 2019 as Project Connected Home over IP (CHIP) and then several missed deadlines, the much-anticipated home automation standard Matter was officially released on October 4, 2022, by the Connectivity Standards Alliance (CSA, formerly the Zigbee Alliance). Matter is a royalty-free connectivity standard that enables communications among a wide range of smart home devices.

Matter uses IP technologies such as Ethernet, Wi-Fi, Thread (low-power mesh networking protocol), and Bluetooth Low Energy (BLE) for configuration. It seems that Matter has an affinity towards Thread as the IP protocol of choice to form the backbone of a connected home in the long term.

The first version of Matter supports devices, including door locks, HVAC controls, lighting and electrical, media devices, safety and security sensors, and window coverings and shades. In subsequent versions, additional device types such as cameras, home appliances, robot vacuums, EV charging, and energy managers will likely be supported. Matter devices can also connect with devices supporting other protocols, like Zigbee, using bridges. To simplify device setup during commissioning, Matter uses QR codes and BLE. A Matter device can also be updated over the air (OTA).

CSA has taken care of various security best practices when developing Matter. For example, each Matter device includes a unique identity to ensure that only authentic and certified devices can join the network. Data is encrypted, and fine-grained access control policies have been implemented. Matter also supports Distributed Compliance Ledger (DCL), a cryptographically secure, distributed storage network based on blockchain. It allows IoT device manufacturers and vendors, official test houses, and Certification Centers to publish public information about a device or class of devices, hence providing a reliable source of information about the device.

Will Matter matter? We do not know that yet. However, it is likely that Matter will matter as the list of CSA member companies that support the standard includes almost all the major smart home device vendors, including Apple, Google, Amazon, IKEA, Huawei, Samsung, Schneider Electric, Bosch, Verizon, and hundreds more. Many have announced the release of Matter-supported devices in 2023 (see list of announcements).

9. Biggest IPO: Mobileye

2022 was generally a bad year for tech IPOs. According to an Ernst&Young report, global IPO proceeds were down 61% compared to 2021.

From an IoT point of view, the Israeli company Mobileye stood out with its IPO (for the second time) on October 26, 2022, at a valuation of $17 billion. The valuation was considerably below the once-expected valuation of $50 billion by its parent Intel, a sign of readjusted valuations of tech companies because of the higher interest rates rise and a jittery economy.

Founded in 1992, Mobileye is a market leader in Advanced Driver Assistance Systems in the autonomous vehicle space. Intel first acquired the company for $15.3 billion in 2017. After the 2022 spinoff, Intel will continue to retain a majority stake in the company. Mobileye’s chip-based camera systems are known for powering semi-automated driving features with its tools installed in over 100 million cars. Intel intends to use some of the funds from the IPO to build more chip factories.

One of the earliest tech IPOs of 2022, and which surprisingly remains one of the only seven IPOs of companies from the bay area in 2022, is that of Credo Technology. Credo Technology is a fabless company founded by ex-Marvell executives in 2008. Its IPO is particularly interesting given that semiconductor company IPOs are rare. The valuation of Credo on IPO day was $1.4 billion. Credo makes chips and components for hyperscalers and 5G wireless network operators to transport huge volumes of data at high speed while consuming less power. Credo’s IP that differentiates it from its competitors is its patented Serialize/Deserialize (“SerDes”) chiplet, which allows cheaper manufacturing, smaller chip size, and better power efficiency.

Another company that almost went public in 2022 but did not is Databricks. The Databricks IPO, which is expected in 2023, likely got postponed due to poor market conditions. Databricks, currently valued at $38 billion (as of August 31, 2022), was founded by the creators of Apache Spark™, Delta Lake, and MLflow. It focuses on AI-based data analytics, engineering, data warehousing, and business analytics. Co-founders Ion Stoica and Matei Zaharia stand to become among the richest people in their home country of Romania when the IPO goes through next year (Ali Ghodsi and Reynold Xin are the other co-founders).

Yet another IPO that was rumored for 2022 was that of ARM, the chip designer powering almost all the smartphones and tablets in the world. The IPO route for ARM had opened after its acquisition by NVIDIA failed in February 2022 due to stiff resistance from regulators in the U.S., Europe, and China. ARM, which was set to be acquired by NVIDIA for $40 billion, has now been put on the IPO wait list for 2023 by its parent SoftBank.

It is also worth looking at the stock performance of IoT companies that went public in the past few years. Many of them underperformed in the broader tech market in 2022. Here are some of them:

- Sonos (IPO 2018): −43.7% in 2022

- Samsara (IPO 2021): −53.2% in 2022

- C3.ai (IPO 2020): −65.7% in 2022

- Tuya (IPO 2021): −68.7% in 2022

10. Most notable new IoT projects: 11 lighthouse smart factories

Ever since the World Economic Forum (in collaboration with McKinsey&Co) announced the first set of 16 global lighthouse manufacturing sites in 2019, the world has taken a closer look at the factories that made the list. In October 2022, the WEF announced the inclusion of 11 new lighthouses to take the existing count to 114 lighthouses globally, spanning various industries, including healthcare, electronics, pharmaceuticals, and automotive. Interestingly, 11 of the new lighthouses are based in Asia, acknowledging that Asian sites are quickly catching up with European and North American sites, which are generally regarded as being more digitally mature. For example, Agilent Technologies in Singapore deployed IIoT-powered digital twins, AI, and Robotic Automation solutions to increase output by 80%, improve productivity by 60%, improve cycle time by 30%, and quality cost by 20%, according to the report.

The 11 new lighthouses are:

- Agilent Technologies, Singapore

- CATL, Yibin/China

- Cipla, Indore/India

- Danone, Opole/Poland

- Dr. Reddy’s Laboratories, Hyderabad/India

- Flex, Sorocaba/Brazil

- Haier, Qingdao/ China

- Midea, Shunde/China

- Mondelēz, Sri City/India

- Sany Heavy Industry, Changsha/China

- Western Digital, Shanghai/China

Four sites were also designated as Sustainability Lighthouses in 2022. A Sustainability Lighthouse is a site that is committed to environmental stewardship by reducing consumption, resource waste, and emissions

The four Sustainability Lighthouses are:

- Arçelik, Ulmi/Romania

- Micron, Singapore

- Unilever, Dapada/India

- Western Digital, Shanghai/China

For example, Arçelik, powered by 100% green electricity, deployed sustainability use cases, such as digital twins for energy management and closed-loop water management systems integrated into advanced water treatment plants. It reduced water consumption by 25%, energy consumption by 17%, and GHG emission by 22% per unit manufactured.

Advanced factories are of particular interest from an IoT point of view. According to our own data, manufacturing is the largest IoT vertical, and factories are the biggest segment within that vertical for IoT. Factories have huge bases with millions of sensors, field instruments, controllers, and other hardware/software systems,

For those interested in more data on IoT and manufacturing, IoT Analytics, together with Microsoft and Intel, published the 59-page IoT Signals – Manufacturing Spotlight in August 2022 (download for free), in which we surveyed 500 decision-makers in discrete, hybrid, and process industries to understand the status quo and future outlook for IoT in manufacturing. A sneak peek of the data for the most important smart manufacturing KPIs can also be found here in our own blog.

Further information

IoT Analytics constantly monitors current trends in IoT markets and makes them available to enterprise subscription clients.

Our IoT coverage in 2022

Would you like to take a deeper look at current IoT markets? You may be interested in one of the market reports and trackers we published in 2022. You can find the complete overview here.

General IoT reports

- MWC Barcelona 2022 Event Report

- Emerging IoT Technologies Report 2022

- State of IoT—Spring 2022

- Hannover Messe 2022 — the latest Industrial IoT / Industry 4.0 trends

- Quarterly Trend Report: What CEOs talked about in Q3/2022

Industrial IoT reports

- Industrial Software Landscape 2022–2027

- Industrial IoT and Industry 4.0 Case Study Report 2022

- Industry 4.0 Adoption Report 2022

- SPS Fair 2022—the latest industrial automation trends

- Machine Vision Market Report 2022-2027

Connectivity and Hardware reports/tracker

IoT Software and Platforms reports

Non-industrial IoT reports

Our IoT coverage in 2023

For continued coverage and updates (such as this one), you may subscribe to our newsletter. In 2023, we will keep our focus on important IoT topics such as Digital Twin, IoT Gateways, Predictive Maintenance, Industrial Edge Computing, IoT Use Cases and more. Plenty of new reports will be published in the coming months.

For a complete enterprise IoT coverage with access to all of IoT Analytics paid content & reports as well as dedicated analyst time, your company may subscribe to the Corporate Research Subscription.

Much success for 2023 from our IoT Analytics team to yours!

{kind=link}